Lithium producer Livent (LTHM: $19/share midpoint of IPO price range) will IPO on Thursday, October 11. At a price range of $18-$20/share, the company plans to sell up to $460 million in stock to the public that will result in a market cap of ~$2.7 billion. At the midpoint of the IPO range, LTHM currently earns our Neutral rating.

LTHM is profitable – unlike a record 83% of IPOs so far this year – but the company still faces significant challenges. The lithium producer, which is being spun-off of parent company FMC Corporation (FMC), faces significant pricing pressure and is overvalued when compared to other mining companies.

This report aims to help investors sort through Livent’s financial filings to understand the fundamentals and valuation of this IPO.

A (Sort of) Bet on Electric Vehicles

LTHM is a spinoff of diversified chemical company FMC, which will receive all the proceeds of the IPO and retain control of ~85% of LTHM’s shares.

LTHM describes itself as a “pure-play, fully integrated lithium company.” The company extracts lithium brine from the Salar del Hombre Muerto mine in Argentina, and it refines that lithium into a variety of compounds at manufacturing facilities around the world.

Most of the press surrounding LTHM focuses on its ties to the electric vehicle (EV) market, but that remains a minority of its business for now. In 2017, sales of lithium hydroxide for EV batteries accounted for just 24% of revenue. The other 76% of revenue came from sales of other lithium compounds used in industrial processes and pharmaceuticals.

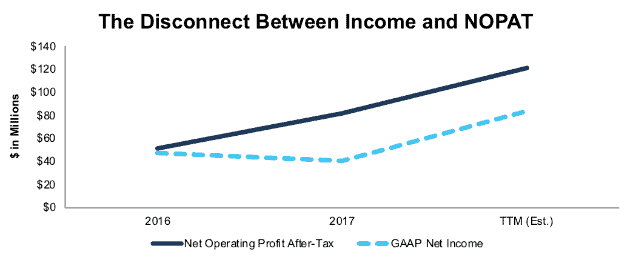

Still, the EV market represents the primary growth driver for LTHM. Tesla (TSLA) gets most of the attention in this sector, but many other automakers are ramping up their EV production as well. Demand for lithium hydroxide is projected to grow by 44% compounded annually over the next decade, according to research firm Roskill. Figure 1 shows that LTHM’s after-tax operating profit (NOPAT) grew from $51 million in 2016 to $82 million in 2017, a 61% increase. It also shows that NOPAT has continued to grow to an estimated $121 million over the trailing twelve months.[1]

Figure 1: LTHM GAAP Net Income and NOPAT Since 2016

Sources: New Constructs, LLC and company filings

Figure 1 also shows that reported earnings significantly understate LTHM’s profitability. Two unusual items – a $31 million pension settlement expense and a net $11 million charge from tax reform, which combined account for 10% of revenue – artificially reduce LTHM’s reported 2017 and TTM earnings.

Oversupply Could Hurt Margins

LTHM plans to capitalize on the increased demand for lithium hydroxide by dramatically increasing its production. The company stated in its S-1 that it plans to increase production capacity from 18.5 thousand metric tons in 2017 to 55 thousand metric tons in 2025, a threefold increase.

Unfortunately for LTHM, it’s not alone in increasing its lithium production. The rise in demand has led to a boom in new lithium mining production. New mines are coming online around the world, and key competitor Sociedad Qimica y Minera de Chile (SQM) could increase its production by 4-6 times over the coming years.

All this new supply has led to a crash in lithium prices. In China, which accounted for 32% of LTHM’s revenue through the first six months of 2018, lithium prices fell from ~$25 thousand per ton in March to $13 thousand per ton in August, a 47% drop.

Falling lithium prices could hurt LTHM’s margins and put a damper on its planned increase in production. Potential investors should be concerned about this fact because, as we’ll show below, there’s significant growth already baked into the proposed IPO valuation.

LTHM Holds Potential Competitive Advantages

Despite its status as a commodity producer, LTHM has certain competitive advantages that could allow it to continue to earn high margins and profits even as lithium supply increases dramatically.

Most notably, LTHM should have a significant cost advantage compared to most of the new lithium producers entering the industry. According to the same Roskill report referenced above, LTHM is the lowest cost lithium hydroxide producer in the world, primarily due to the attractive location of its Argentinian mine, which is located on a salt flat. Extracting lithium brine from salt flats is significantly cheaper than mining hard rock lithium, which constitutes a large share of the new lithium production coming online.

In addition, LTHM is an integrated lithium producer, meaning it manufactures lithium compounds in addition to extracting the raw materials. The company has over 60 years of expertise in lithium compound production, which should give it a competitive advantage over newer producers.

It remains to be seen how significant or durable these advantages are, but they should at least allow LTHM to maintain superior profitability compared to other lithium producers for the foreseeable future.

LTHM is Overvalued Compared to Peers

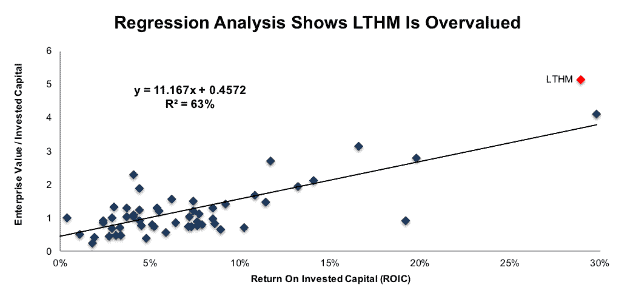

Numerous case studies show that getting return on invested capital (ROIC) right is an important part of making smart investments. Ernst & Young recently published a white paper that proves the material superiority of our forensic accounting research and measure of ROIC. The technology that enables this research is featured by Harvard Business School.

Per Figure 2, ROIC explains 63% of the difference in valuation for the 61 Metals and Mining companies under coverage. LTHM trades at a significant premium to its peers based on its position above the trendline.[2]

Figure 2: ROIC Explains 63% of Valuation for Metals and Mining Companies

Sources: New Constructs, LLC and company filings

Based on its current enterprise value per invested capital (a cleaner version of price to book) of 5.1, the market expects LTHM’s ROIC to increase to 42%. Notably, no other company in the industry has earned an ROIC above 38% in any single year over the past five years.

Our Discounted Cash Flow Model Shows Potential Downside for LTHM

Our dynamic DCF model shows that the future cash flow expectations baked into LTHM’s are optimistic, but not impossible.

To justify the midpoint of its IPO range at $19/share, LTHM must maintain 2017 NOPAT margins of 24% and grow revenue by 15% compounded annually for the next seven years, in line with its projected production increase. See the math behind this dynamic DCF scenario.

If falling lithium prices put pressure on LTHM’s growth and margins, the stock could have significant downside. If NOPAT margins fall to 2016 levels of 19% and revenue grows by just 10% compounded annually for the next 10 years, the stock is worth just $13.50/share today, a 30% downside from the midpoint of the IPO. See the math behind this dynamic DCF scenario.

Investors view LTHM as a bet on electric vehicles, but really, it’s a bet on lithium prices. Higher lithium prices will be bad for EV producers but great for LTHM.

Critical Details Found in Financial Filings by Our Robo-Analyst Technology

As investors focus more on fundamental research, research automation technology is needed to analyze all the critical financial details in financial filings. Below are specifics on the adjustments[3] we make based on Robo-Analyst[4] findings in Livent’s S-1:

Income Statement: we made $47 million of adjustments, with a net effect of removing $41 million in non-operating expense (12% of revenue). You can see all the adjustments made to LTHM’s income statement here.

Balance Sheet: we made $83 million of adjustments to calculate invested capital with a net increase of $53 million. The most notable adjustment was $46 million in accumulated other comprehensive loss. This adjustment represented 11% of reported net assets. You can see all the adjustments made to LTHM’s balance sheet here.

Valuation: we made $12 million of adjustments with a net effect of decreasing shareholder value by $12 million. The largest adjustment to shareholder value was $6 million in off-balance sheet debt. This hidden liability represents less than 1% of LTHM’s proposed market cap.

This article originally published on October 10, 2018.

Disclosure: David Trainer, Kyle Guske II, and Sam McBride receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] LTHM’s S-1 does not give us enough information to definitively calculate its NOPAT over the TTM period.

[2] Same as Figure 1, LTHM’s TTM ROIC and Invested Capital are estimated due to lack of information in the company’s S-1

[3] Ernst & Young’s recent white paper “Getting ROIC Right” demonstrates the link between an accurate calculation of ROIC and shareholder value.

[4] Harvard Business School Features the powerful impact of research automation in the case study New Constructs: Disrupting Fundamental Analysis with Robo-Analysts.