Under even the most optimistic integration scenarios, we believe that Salesforce.com’s (CRM) proposed acquisition of Demandware (DWRE) for $75/share or $2.85 billion represents an unacceptable transfer of wealth from CRM to DWRE shareholders. As noted in prior reports, Demandware is far from profitable. Salesforce is not much better. Our models show that more than $2 billion of the $2.8 billion purchase is an overpayment and a direct destruction of value for CRM shareholders.

Salesforce Is Spending On A Profitless Business

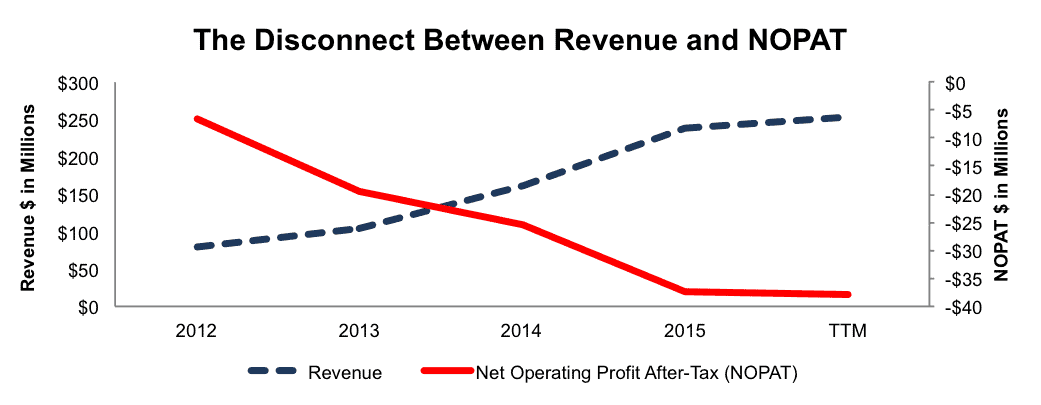

Since going public, Demandware’s operations have focused on revenue growth with no regard to the bottom line. The company’s after-tax profit (NOPAT) has declined from -$7 million in 2012 to -$38 million in fiscal year 2015. Conversely, Demandware’s revenue has grown from $79 million in 2012 to $254 million over the last twelve months (TTM), per Figure 1.

Figure 1: Demandware’s Growing Losses

Sources: New Constructs, LLC and company filings

Acquisition Is A Misallocation Of Capital

In a nutshell, Salesforce is paying $2.8 billion to acquire an unprofitable company (Demandware lost -$38 million in NOPAT in the last twelve months). The deal generates an ROIC of -1%, which is lower than Salesforce’s 2% ROIC and well below the company’s 9% weighted average cost of capital (WACC). To justify paying $75/share, Salesforce would need, at a minimum, Demandware’s NOPAT (assuming no capex) to be $257 million or 9% of the $2.8 billion purchase price. At that level, the deal would earn Salesforce an ROIC equal to its WACC, which is still a low hurdle, but at least the deal would not destroy value.

How Much Is Salesforce Overpaying?

To get a sense of how much shareholder value Salesforce is destroying, let’s look at some reasonable scenarios for how much the company can improve Demandware’s business so that it generates some cash flow. First, we account for liabilities that investors may not be aware of that make DWRE more expensive than the accounting numbers would suggest.

- $68 million in outstanding employee stock options (4% of market cap prior to acquisition announcement)

- $31 million in off-balance-sheet operating leases (2% of market cap prior to acquisition announcement)

Next, Figures 2 and 3 show the implied stock prices that Salesforce should pay for DWRE to achieve a ROIC equal to its WACC, assuming different scenarios for revenue growth and NOPAT margins. In each of these scenarios, we conservatively assume that Salesforce can grow Demandware’s revenue and NOPAT without spending on working capital or fixed assets. In Figure 2, the revenue growth scenarios assume that upon acquisition, DWRE immediately achieves Salesforce’s NOPAT margin of 2.1%. The current margin is -14.9%.

Figure 2: Implied Acquisition Prices For CRM To Achieve 9% ROIC with 2.1% NOPAT margin

Sources: New Constructs, LLC and company filings. $ values in millions except per share amounts.

The big takeaway from Figure 2 is that even if Demandware grows revenue by 50% compounded annually for the next five years, the most Salesforce should pay to ensure an ROIC equal to WACC is $11/share, or $2.4 billion (85%) less than the proposed purchase price. For reference, Demandware grew revenue by 48% in 2015, and consensus estimates peg revenue growth at 28% in 2016.

Figure 3: Implied Acquisition Prices For CRM To Achieve 9% ROIC with 4.2% NOPAT margin

Sources: New Constructs, LLC and company filings. $ values in millions except per share amounts.

In Figure 3, the revenue growth scenarios assume that upon acquisition, DWRE immediately achieves a 4.2% NOPAT margin, which is double CRM’s TTM NOPAT margin. Even in this scenario, the most Salesforce should pay for DWRE is $22/share, or 71% below the actual acquisition price.

In addition to significantly higher revenue growth expectations, both scenarios are made more optimistic by the high NOPAT margin estimates (DWRE’s TTM NOPAT margin was -14.9%).

The bottom line is that Salesforce’s management should have some explaining to do to justify this acquisition at $75/share.

Implied Synergies Are Unreasonable

The only reason for a firm to pay a premium over the market value for another firm is if the acquiring firm believes there are significant synergies attainable through acquisition. As the deal is constructed, Salesforce is paying a premium of $27.01/share (from 5/31/16 close price), or slightly over $1 billion above market price. Salesforce has yet to make any mention of the dollar value of synergies between the two companies.

Conclusion

Until investors hold management accountable for intelligent capital allocation, they can expect companies to continue to destroy shareholder value without feeling any accountability to their investors. Given our analysis above, we think it fair to ask both management teams how this deal is fair to their investors. The answer for DWRE investors appears easy. The answer for CRM investors is not so easy.

This article originally published here on June 2, 2016.

Disclosure: David Trainer and Kyle Guske II receive no compensation to write about any specific stock, style, or theme.

Click here to download a PDF of this report.

Photo Credit: Justin Levy (Flickr)

1 Response to "Salesforce.com Investors Lose Big In Demandware Acquisition"

Please do a feature highlighting the overwhelming accounting fraud CRM Salesforce is using and has been using more aggressively over the last 6 months, as its market cap has grown over $100 Billion. Non-GAAP numbers are the ONLY numbers being reported about this company, and the long non-vested employees are especially fearful of the price dropping before their shares vest. As a result, the continuing valuation toward pie-in-the-sky is especially dangerous.

Any time anybody tries to bring up GAAP facts, Salesforce employees downvote, censor, or otherwise block the details.

There is something really awful and sinister happening at this company, and all over corporate America. Please help bring your awesome analysis and charts that people can share to spread the news of this fraudulent company.