Non-GAAP earnings are back in the crosshairs. 15 years after the Enron scandal first prompted the SEC to create rules for non-GAAP metrics, the proliferation of these pro forma results—especially extreme cases such as Valeant (VRX)—have led to renewed scrutiny. Most notably, the SEC has created a task force to review companies’ use of non-GAAP metrics.

Whenever non-GAAP metrics get attacked, a slew of contrarians leap to defend them by pointing out that GAAP standards have many flaws. Traditional GAAP accounting, these critics argue, do a poor job of reflecting economic realities and already contain enough loopholes for executives to “manage” earnings.

These critics are right that GAAP is flawed. It’s just that non-GAAP is even worse.

GAAP Earnings Require Fixing

GAAP standards contain numerous loopholes that executives can use to manipulate earnings, which studies show they do with frequency and magnitude.

Given these flaws, it’s understandable that people would think non-GAAP metrics could better serve the interests of investors who want to understand the true cash profitability of businesses.

Companies Make Non-GAAP Earnings Worse Than GAAP

Non-GAAP earnings tend to be much worse than GAAP earnings when it comes to accurately reporting profits. GAAP standards at least hold companies to a common set of rules. Companies that report non-GAAP earnings can make up whatever rules they want, and they almost always use those rules to inflate their reported growth and profitability.

It is naïve to assume that accurate communication of the true profitability of the business is a top priority for management teams. Experience has taught us that executives are primarily concerned with maximizing their compensation, which leads them to report the results that drive the metrics to which their compensation plans are linked, not the results that are the most accurate.

Case Study on How Non-GAAP Hurts Investors

Like 90% of companies in the S&P 500, Newell Brands (NWL) reports non-GAAP earnings along with GAAP net income. However, this consumer staples company stands out for the way it uses these made up numbers to give the illusion of growing profitability.

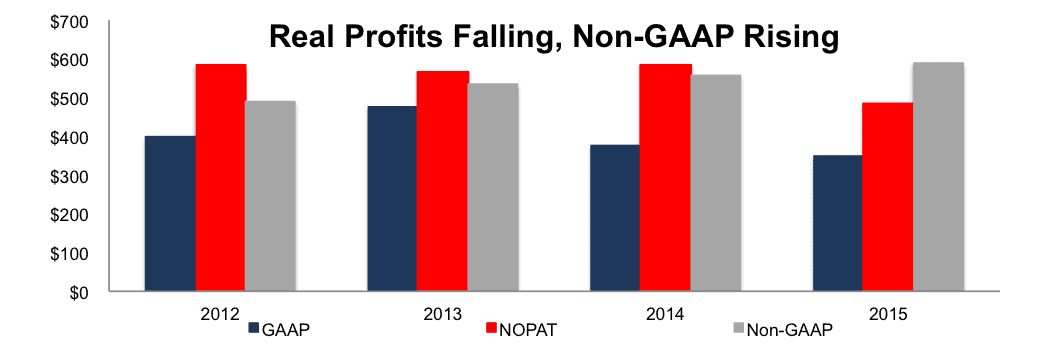

Figure 1: GAAP Vs. Non-GAAP For Newell Brands (NWL)

Sources: New Constructs, LLC and company filings.

Should We Be Surprised That Non-GAAP Numbers Are Misleading?

No, not if you do a little digging. As we explain in 4 Reasons Executives Manipulate Earnings, ever since “performance-based” bonuses were made tax-deductible in 1993, an increasingly large portion of executive compensation has been tied to hitting certain performance targets. In many cases, these are “adjusted” non-GAAP metrics that are designed so that executives always hit the incentive targets.

Figure 1 shows how Newell Brand’s (NWL) non-GAAP earnings have risen in each of the past three years, contrasting with the decline in both its GAAP net income and its net operating profit after tax (NOPAT), a measure of operating profit that reverses GAAP’s accounting distortions on a consistent basis across companies.

Newell achieves this false growth through a variety of tactics. For one, it excludes “non-recurring” charges such as restructuring, which the company has incurred for almost 20 consecutive years. After two decades, it’s hard to argue these are one-time expenses.

Here are details on the types of adjustments companies make to create misleading non-GAAP metrics.

The Real Problem: Owner-Agent Conflict and the Integrity of the Capital Markets

When non-GAAP earnings push the focus further away from actual economic profits, they exacerbate the disconnect between executive incentives and the best interests of shareholders.

This Owner-Agent problem exists because executives (the Agent) are supposed to work in the best interests of the shareholders (the Owner) – in theory. In practice, they often serve their own interests first.

Take Valeant Pharmaceuticals (VRX) as an example. The company’s compensation structure incentivized CEO Mike Pearson to take big risks, inflate earnings, and chase short-term gains in the stock price. After the stock collapsed, average investors are left with big losses while Pearson walks away with a $9 million severance package.

Frauds such as Enron, Tyco and WorldCom, show that executives blatantly lie to investors to enrich themselves.

By obscuring true profitability and widening the gap between executive incentives and shareholder interests, non-GAAP metrics reduce the efficiency and integrity of capital markets.

Investors should do their diligence and not rely on information from conflicted sources.

This report originally published here on September 23, 2016.

Disclosure: David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, style, or theme.

Scottrade clients get a Free Gold Membership ($588/yr value). Login or open your Scottrade account & find us under Quotes & Research/Investor Tools.

Click here to download a PDF of this report.

Photo Credit: Benjamin Reay (Flickr)

4 replies to "What’s The Problem With Non-GAAP Earnings?"

Hi David,

My firm represents Newell Brands’ PR.

Wanted to point out that the sentence below, which I’ve starred, is incorrect. In fact, this item WAS excluded from non-GAAP earnings. Can you please make this change to your story?

Even when the company does exclude legitimately non-recurring expenses, such as a $10.2 million product recall charge, it still misleads investors by including non-recurring income. In 2015, the company earned $95.6 million in after-tax income from the sale of its Endicia shipping business. ****Even though this item is clearly a one-time, non-operating gain, it was not excluded from non-GAAP earnings.****

That paragraph has been deleted from the story

Hi, just picked up this interesting article whilst carrying out diligence on the quality of financial statements produced by Newell Brands. The company’s stock appeared possibly undervalued at $27 per share however my thesis may need to be evaluated further if the numbers cannot be trusted. It would be great to hear your thoughts on red flags to watch out for in the accounting.

Many thanks

Dr Parag Nandha

Value Investor

Milton Keynes, UK

NWL’s 2017 GAAP earnings are significantly inflated due to a $1.5 billion one-time benefit from tax reform. Its non-GAAP numbers adjust for that benefit, but they still overstate the company’s profitability. Non-GAAP net income increased by 10% in 2017, but after-tax operating profit (NOPAT) only increased by 2%.