Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life and Marketwatch.com

A beaten down company will always find its suitors, those wanting to “pick up the pieces” or buy the bottom. This week’s Danger Zone pick is down 32% year to date, but it is not a good value and carries high downside risk. Unsustainable revenue growth, destructive acquisitions, and declining profits land Mattress Firm (MFRM: $31/share) in the Danger Zone.

Revenue Growth Masks Soaring Losses

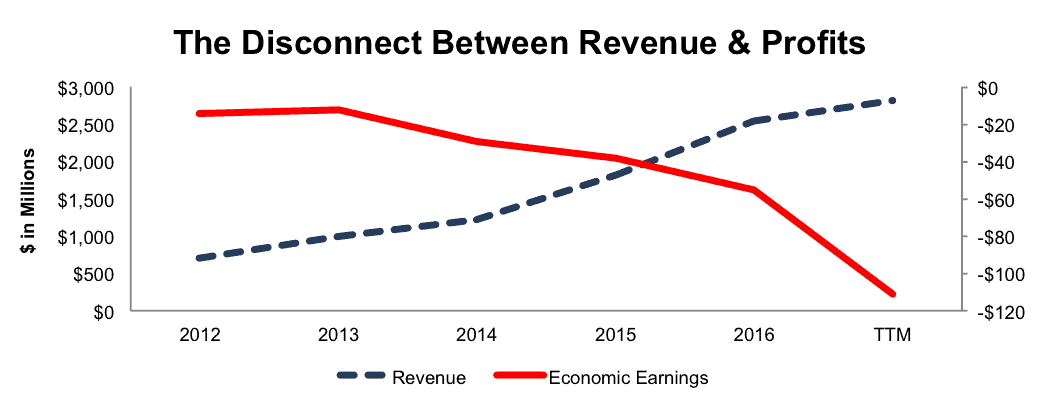

Mattress Firm’s economic earnings, the true cash flows of the business, have declined from -$14 million in fiscal 2012 to -$111 million over the trailing twelve months. These losses come despite revenue growing from $704 million in fiscal 2012 to $2.5 billion in fiscal 2015, or 38% compounded annually. Revenues have continued to grow to $2.8 billion over the last twelve months. Figure 1 highlights the disconnect between revenue and cash flow. See the reconciliation of Mattress Firm’s GAAP net income to economic earnings here.

Figure 1: MFRM’s Losses Grow Despite Revenue Growth

Sources: New Constructs, LLC and company filings

In its quest be the leading mattress retailer, since 2013, MFRM has made over 15 separate acquisitions for upwards of $1.4 billion. Most recently, the firm paid $795 million for the acquisition of HMK Mattress Holdings in February 2016. While these acquisitions are superficially “accretive” to EPS, they are highly dilutive to cash flows and MFRM’s balance sheet. From 2013-2016, Mattress Firm’s debt grew 42% compounded annually to $2.1 billion. Over the last twelve months, debt has ballooned to nearly $2.9 billion, more than double the current market cap.

The telltale sign that these acquisitions have been a raw deal for investors is the steady deterioration of MFRM’s return on invested capital (ROIC). Since earning a 10% ROIC in 2012, Mattress Firm’s ROIC has more than halved to a bottom-quintile 4% over the last twelve months. Similarly, MFRM has burned $1.6 billion in free cash flow from 2013-2016, and over the last twelve months, FCF sits at -$603 million.

Executive Compensation Rewards Destroying Shareholder Value

Apart from base salaries, executives at Mattress Firm receive annual cash bonuses and long-term stock-based awards. The cash bonuses are granted solely for meeting adjusted EBITDA targets. As seen in Figure 2 below, adjusted EBITDA presents MFRM in a much more positive light than the true profits of the business, which misalign executives incentives with those of investors. By removing costs such as compensation expense or acquisition costs, executives can grow the top line and adjusted metrics with little or no attention paid to the economics of their actions. Additionally, we’ve seen the damaging effects that incentivizing executives with stock price targets can have, particularly at Valeant Pharmaceuticals. The best way to create shareholder value, and align executives with the best interest of shareholders, is to tie performance bonuses to ROIC because there is a clear correlation between ROIC and shareholder value.

Adjusted EBITDA Rises While Profits Decline

Investors analyzing non-GAAP metrics would believe Mattress Firm’s business is achieving great success. Mattress Firm is a prime example of how companies remove normal operating costs to create a more positive picture of the business. Here are expenses MFRM has removed when calculating its non-GAAP metrics, including adjusted EBITDA, adjusted EPS, and adjusted cash EPS:

- Loss on store closing & impairment of store assets

- Loss from debt extinguishment

- Stock based compensation

- Secondary offering costs

- Acquisition related costs

- ERP system implementation costs

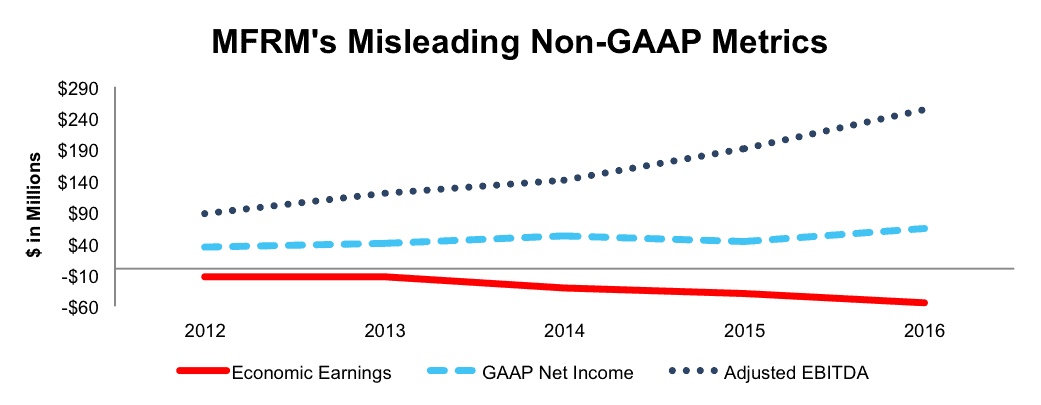

These costs have a material impact on results, particularly acquisition related costs. In 2016, MFRM removed $23 million (35% of GAAP net income) in acquisition related costs to calculate its adjusted EBITDA. After removing these costs, MFRM is able to report non-GAAP results that are not only much improved from economic earnings, but rapidly rising when cash flows are declining. Adjusted EBITDA grew from $87 million in 2012 to $255 million in 2016, or 31% compounded annually. Over this same time, GAAP net income grew 17% compounded annually while economic earnings declined from -$14 million to -$55 million, or -41% compounded annually, per Figure 2.

Figure 2: Misleading Non-GAAP Metrics

Sources: New Constructs, LLC and company filings

Low Profitability In A High Margin Industry

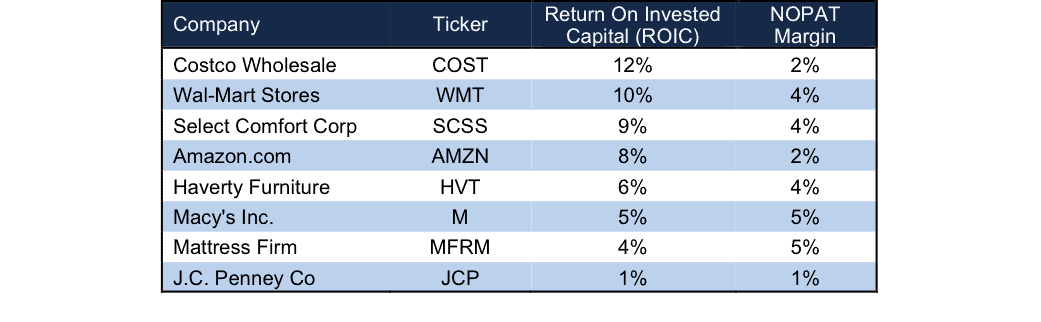

The retail mattress market is well known to have exorbitantly high markup on its products. Such markup provides excellent opportunity for profits, which ultimately breeds competition. The mattress market is highly fragmented, and MFRM faces competition from regional and local stores such as America’s Mattress, retail furniture stores like Ashley Furniture, Haverty’s (HVT), and Rooms-to-Go, department stores like Macy’s (M) and J.C. Penney (JCP), and large retailers like Wal-Mart (WMT), Costco (COST), and Amazon (AMZN). This list doesn’t even mention the new start-up online mattress retailers such as Casper, Tuft & Needle, Saatva, and Leesa. Unfortunately for investors, MFRM has not been able to translate these high markup prices to high margins or a high ROIC. As seen in Figure 3, MFRM’s ROIC ranks well below most competitors and its margins hardly surpass big box retailers better known for selling products with razor-thin margins.

Figure 3: MFRM’s “Retail-Like” Profitability

Sources: New Constructs, LLC and company filings

Bull Hopes Rest On Happy Ending to Roll-Up

First, we’ve seen this movie before. In my experience on Wall Street (going on 20 years), there have been precious few roll-ups that have a happy ending. Most of them end with investors realizing the emperor has no clothes, or the consolidator has no cash flows.

Roll-ups make the insiders (corporate executives and Wall street bankers) lots of money, and investors should not be surprised to see these folks touting the roll-up plan. Remember that these insiders’ interests are not aligned with yours. As we detail below, Mattress Firm’s roll-up pitch fits the description of a roll-up scheme very well.

Prior to the HMK Mattress Holdings acquisition, the mattress market was highly fragmented. Post acquisition, MFRM stated the combined firm would have a 21% share of the mattress market. As market share climbs, roll-up strategies become harder to execute, because the impact of acquisitions becomes ever smaller. As such, those betting on the future growth of Mattress Firm are betting on the inevitable end of the roll-up and successful, more importantly profitable, integration of all the acquired firms.

However, without the constant acquisitions to grow the top line and poor organic growth, the bull case appears rather weak. Since 2012, total sales have grown on average 38% each year. Excluding new stores, comparable-store sales have grown only 4% on average each year since 2012. Even the revenue growth numbers are misleading. Once the roll-up strategy comes to an end, revenue growth will follow the negative trend that profits have been setting for years.

Investors have taken note of the lack of organic growth at MFRM, but as we’ll show below, even after falling 32% YTD, MFRM is still priced for significant profit growth. Such profit growth is unlikely to be achieved with such low comparable-store sales. The current expectations baked into the stock price require the acquisitions to continue, but also become immediately profitable, which has not occurred as of yet.

Even if you think the roll-up strategy will work, you have to be mindful of new entrants providing mattresses at much cheaper price points. Online mattress firms, such as Casper and Tuft & Needle, cut out middlemen like Mattress Firm. They are more profitable because they don’t require the costly overhead of showrooms or commissioned sales staff as they ship mattresses directly to buyers. While this shift in business model is certainly too new to judge its overall effect, there is no debating that cutting out middlemen and providing consumers cheaper products is a threat to the viability of Mattress Firm’s business model.

The largest risk to the bear case is what we call ‘stupid money risk.’ With a stock price that is down YTD, another firm could step in and acquire MFRM at a value that is much higher than the current market price. As we’ll show below, only in the event a firm is willing to destroy shareholder value is MFRM worth more than its current share price.

Unraveling Roll-Up Worth Acquiring?

The biggest risk to our thesis, apart from MFRM continuing to acquire smaller competitors to maintain non-GAAP growth, would be if an outside firm was to acquire MFRM at a value at or above today’s price. Despite being the industry leader, we’ll show below that Mattress Firm is not an attractive acquisition target because unless a buyer is willing to destroy shareholder value, an acquisition at current prices would be unwise.

To begin, MFRM has liabilities that investors may not be aware of that make it more expensive than the accounting numbers suggest.

- $1.4 billion in off-balance-sheet operating leases (122% of market cap)

- $52 million in net deferred tax liabilities (5% of market cap)

- $19 million in minority interests (2% of market cap)

- $8 million in outstanding employee stock options (<1% of market cap)

After adjusting for these liabilities (which total 129% of market cap) we can model multiple purchase price scenarios. Even in the most optimistic of scenarios MFRM is worth less than the current share price.

Figure 4 shows what we think Wal-Mart (WMT) should pay for MFRM, given different growth scenarios that account for the capital outlay required to achieve such a scenario. Because MFRM is the largest mattress retailer, any acquiring firm would likely be another furniture store or big box retailer. WMT acquiring MFRM could lead to more efficient supply chain management, cost reductions due to WMT’s massive distribution footprint, or even increased sales through marketing efforts or integration of MFRM’s products into WMT stores. However, there are limits on how much WMT would pay for MFRM given the cash flows being acquired

Each implied price is based on a DCF scenario (linked below) assuming different levels of future revenue growth:

- Scenario 1: 51% in (estimated) year one, 6% in (estimated) year two, and 4% in (estimated) year 3 and beyond.

- Scenario 2: 51% in (estimated) year one, 6% in (estimated) year two, and 6% in (estimated) year 3 and beyond.

- Scenario 3: 51% in (estimated) year one, 6% in (estimated) year two, and 8% in (estimated) year 3 and beyond

In each scenario, the estimated revenue growth rates in year one and two equal the consensus estimates for 2016 (51%) and 2017 (6%). For the subsequent years, we use 4% in scenario one because it represents the average same-store sales growth since 2012. We use 6% in scenario two because it represents a continuation of 2017 expectations. We use 8% in scenario three because it represents the average 2017 expected revenue growth rate of all 47 Household Durables firms under coverage.

Additionally, we assume MFRM’s invested capital increases $968 million in estimated year 1, which is equivalent to the change in net working capital and fixed assets after the acquisition of HMK Mattress Holdings. This acquisition grew MFRM’s store count by over 40% and accounts for much of the revenue growth expected in estimated year 1. We, then, conservatively assume that WMT can grow MFRM’s revenue and NOPAT/free cash flow without any incremental capital outlays after year 1, an unlikely and very optimistic scenario. We also assume MFRM achieves a 7% NOPAT/free cash flow margin, which is the highest margin achieved since 2013 when acquisition activity began ramping up. For reference, MFRM’s current NOPAT margin is 4.6%. This assumption, while optimistic, creates a scenario where acquisitions stop post takeover, and the new parent firm focuses on profitability not topline growth. As shown below, even in this best-case scenario, MFRM is not worth acquiring at current prices.

The resulting implied values for MFRM in each scenario represent the maximum amount WMT should pay for MFRM, given the expected cash flows and the costs to achieve those cash flows.

Figure 4: The Best-Case Scenario Value for MFRM If Acquired

Sources: New Constructs, LLC and company filings.

$ values in millions except per share amounts.

$ value destroyed equals the difference between implied price and acquisition at current market price plus net assets/liabilities.

Figure 4 shows that even if Mattress Firm can grow revenue 15% compounded annually, achieve 7% NOPAT margins, and require no excess capital spending (beyond year 1) for the next five years, the most WMT should pay for the firm is $24/share – a 23% downside from current price. Note in even the most optimistic scenario that the average ROIC over five years only equals 8%, which is slightly below WMT’s 10% ROIC. In order to achieve an ROIC equal to its current ROIC, WMT would either need to pay below $24/share, or grow MFRM’s revenue greater than 15% compounded annually while spending $0 in incremental invested capital.

Without Acquisition, Shares Remain Overvalued

On its own, MFRM still has unrealistically high expectations already baked into the current stock price. Specifically, to justify the current price of $31/share, MFRM must maintain 2016 NOPAT margins (6%) and grow NOPAT by 10% compounded annually for the next 11 years. In this scenario, MFRM would be generating over $7.4 billion in revenue 11 years from now. For reference, MFRM notes in its 2016 10-K that the entire U.S. retail market totaled $14 billion in 2014, of which specialty mattress retailers accounted for 47% of sales.

Put another way, current expectations imply MFRM reaching a sales volume that is greater than the market share of all retail mattress firms in 2014. MFRM must take significant market share from any and all competition over the next decade, which seems unlikely given disruptive new competition and common antitrust laws made to stop exactly such an event.

Even if we assume MFRM can maintain 2016 NOPAT margins and grow NOPAT by 9% compounded annually for the next decade, the stock is only worth $16/share today – a 48% downside.

Each of these scenarios also assumes the company is able to grow revenue and NOPAT without spending on working capital or fixed assets after (estimated) year 1, an assumption that is unlikely, even if the firm ceased destructive acquisitions. We make assumption to show investors just how optimistic they must be about the future cash flows of this company to warrant owning the stock. For reference, MFRM’s invested capital has grown on average $501 million (20% of 2016 revenue) each year since 2013.

Catalyst: MFRM Runs Out Of Options

Mattress Firm finds itself in a tough position. It has acquired its way to the top of the market, but has none of the profits to show for it. Moving forward, MFRM has a few options each of which do not meet the expectations baked into the stock price.

- Continue the roll-up strategy: MFRM could continue acquiring smaller competitors in an effort to grow the top line and boost non-GAAP metrics. However, this option may be difficult, as the firm’s total debt is now more than double its market cap, which could make funding future acquisitions difficult. At the same time, the firm’s non-GAAP earnings cannot cover its cash costs, and with MFRM’s climbing debt, it could only be a matter of time before the costs of the debt outweigh the benefits of acquiring additional revenue.

- Focus on organic growth: MFRM could cease its roll-up strategy and focus on growing its organic business. However, as noted above, without rapid sales growth, and cost cutting, it’s hard to see the organic growth at MFRM reaching levels that meet the expectations already baked into the stock price.

At the end of the day, neither of these options meets the current expectations embedded in the market price. If MFRM ends the roll-up, its growth story comes to a fast end, and the firm’s valuation would adjust accordingly. At the same time, if it abandons the roll-up, investors will quickly realize the emperor has no clothes.

Insider Action Is Strong While Short Interest Is High

Over the past 12 months 2.7 million insider shares have been purchased and 204,000 have been sold for a net effect of 2.5 million insider shares purchases. These purchases represent 7% of shares outstanding, which is a strong number for insider purchases. Additionally, there are 7.2 million shares sold short, or just over 19% of shares outstanding.

Impact of Footnotes Adjustments and Forensic Accounting

In order to derive the true recurring cash flows, an accurate invested capital, and a real shareholder value, we made the following adjustments to Mattress Firm’s 2016 10-K:

Income Statement: we made $199 million of adjustments with a net effect of removing $88 million in non-operating expenses (3% of revenue). We removed $143 million related to non-operating expenses and $56 million related to non-operating income. See all adjustments made to MFRM’s income statement here.

Balance Sheet: we made $1.6 billion of adjustments to calculate invested capital with a net increase of $1.2 million. The most notable adjustment was $1.4 billion (100% of net assets) related to operating leases. See all adjustments to MFRM’s balance sheet here.

Valuation: we made $2.9 billion of adjustments with a net effect of decreasing shareholder value by $2.9 billion. There were no adjustments that increased shareholder value. The largest adjustment was the removal of $2.9 billion (254% of market cap) due to total debt, which includes $1.4 billion in off-balance sheet debt.

Dangerous Funds That Hold MFRM

The following funds receive our Dangerous-or-worse rating and allocate significantly to Mattress Firm.

- Monteagle Funds: Texas Fund (TEXCX) – 1.9% allocation and Dangerous rating.

- Wasatch Core Growth Fund (WGROX) – 1.3% allocation and Dangerous rating.

This article originally published here on July 25, 2016

Disclosure: David Trainer and Kyle Guske II receive no compensation to write about any specific stock, style, or theme.

Click here to download a PDF of this report.

Photo Credit: Social Woodlands (Flickr)

2 replies to "Danger Zone: Mattress Firm (MFRM)"

Gents

Is it time to reexamine your analysis of the risks of acquisitions for the Danger Zone–Sell/Sell Short companies? MFRM gets acquired at $60 per share, almost double the price when this sell recommendation was made. This year, we have seen Danger Zone companies like WhiteWave, Qlik Technologies, Marketo and LinkedIn all acquired for substantial premiums over Danger Zone prices. All were acquired by sophisticated investors. Maybe every single one of them was wrong. Or maybe there was value in the companies that did not appear explicitly on the financial statements. Overall, Danger Zone companies were more likely to be acquired for a premium than Long Ideas.

Your financial analysis is outstanding, but there is mounting evidence that something is missing. Thanks for any thoughts.

This is an issue we’ve spent a lot of time thinking about, and we wrote an article about it a few months ago:

https://www.newconstructs.com/companies-overpay-acquisitions/

The essential problem is that too often management is not aligned with shareholder interests. We’ve been putting a larger emphasis on corporate governance recently, and analyzing acquisition risk has become a much more significant part of the process with our Danger Zone picks.