When Microsoft (MSFT) agreed to pay $26.2 billion to acquire LinkedIn (LNKD) last month, we—along with many others—were left scratching our heads. Why would Microsoft pay such a high premium for a money-losing company with slowing growth and the worst user engagement of any major social media platform?

Microsoft claims the deal has massive synergies that will justify the purchase price. It seems much more likely, however, that the software giant will end up taking a major write-down on LinkedIn, just as it did last year with Nokia ($7.5 billion) and in 2012 with aQuantive ($6.2 billion). The company has an established track record of destroying value by overpaying for acquisitions.

Of course, Microsoft is far from the only company to destroy shareholder value by overpaying to acquire other companies. Most studies find that acquisitions fail to create value for shareholders between 70-90% of the time. We’ve emphasized time and time again that big acquisitions can be accretive to GAAP earnings but actually destroy shareholder value.

Overpriced acquisitions are far from a new phenomenon, but they’ve been especially prevalent in recent months. As a result, we’ve gathered some ideas about the various reasons companies ignore the evidence and continue to overpay for acquisitions.

Big (Misaligned) Compensation Windfalls

Even though acquisition deals theoretically need the approval of shareholders and the board of directors, in practice, executives have an outsized influence on the process. Many boards lack true independence from management, and the large mutual funds and ETFs that own a substantial portion of most public companies rarely vote against board proposals.

In theory activist investors should fill this void by waging campaigns to encourage more responsible corporate governance. In practice, most activists are more focused on short-term gains.

This lack of accountability creates a big problem when executive incentives are misaligned with shareholder value. Too often, executives earn bonuses and stock grants based on metrics that have no real connection to value. See 4 Reasons Executives Manipulate Earnings for more details.

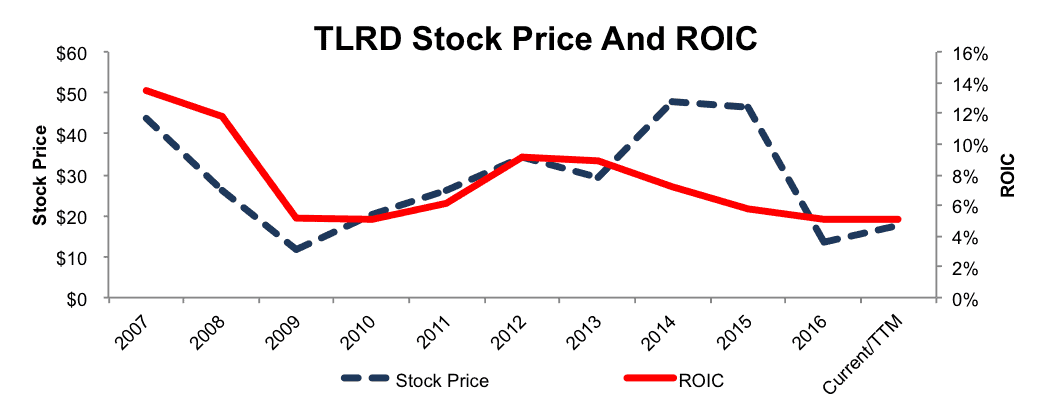

Figure 1: Jos. A. Bank Acquisition Destroys Value For Shareholders

Sources: New Constructs, LLC and company filings.

For a case study on just how much value these overpriced acquisitions can destroy, look no further than the $1.8 billion acquisition of Jos. A. Bank by Men’s Wearhouse (TLRD) in 2014. As Figure 1 shows, the acquisition decreased ROIC and sent the stock price tumbling by more than 50%.

At the same time, CEO Doug Ewert earned a massive bonus for completing the acquisition and for the accompanying revenue growth, which caused his compensation to spike 167%.

For a more recent example, take the recent $2.9 billion acquisition of Demandware (DWRE) by Salesforce.com (CRM). We found that even the most optimistic forecasts for margins and revenue growth could not produce a return on invested capital (ROIC) for the deal that would equal CRM’s cost of capital (WACC).

Earning an ROIC above WACC is the only way to create long-term value for shareholders. However, CRM’s executives are not paid based on ROIC. Instead, their annual cash bonuses come from increasing revenue, operating cash flow, and non-GAAP income. Acquiring Demandware allows CRM to boost all three.

The Overvaluation Trap

Greed is not the only motivator that pushes companies to overpay. Fear can be just as powerful. In particular, many companies fall prey to the Overvaluation Trap. When the market overvalues a company, its executives have to try to find a way to justify that stock price, or they will get blamed for the subsequent drop in value.

More often than not, companies respond to the Overvaluation Trap by making flashy acquisitions. This allows them to claim synergies and “platform value” that can theoretically justify their valuation. As long as the company keeps making acquisitions, it can distract the market from previous failures for a time, until the whole edifice comes crashing down, a scenario that might sound familiar to any who has paid attention to Valeant (VRX).

With the stock market at an all time high even in the midst of an earnings recession, many companies are stuck in the Overvaluation Trap.

Abundance Of Capital

Companies that see their stock as expensive might want to do as many all-stock deals as possible to take advantage of their strong currency.

Not that companies need to use their stock to get deals done. S&P 500 non-financial companies currently hold a record $1.5 trillion in cash and short-term investments on their balance sheets. The $26.2 billion Microsoft agreed to pay for LinkedIn represents less than a quarter of its excess cash.

Public companies aren’t the only ones with money burning a hole in their pockets either. Private equity funds are sitting on over $880 billion in dry power. With lots of cash and expensive stock chasing relatively scarce investment opportunities, there are lots of opportunities for overpriced acquisitions.

Ego

Most individuals that reach the top levels of major public corporations tend to be competitive and have a drive to beat their competitors, and that can manifest in large acquisitions. Oracle (ORCL) founder Larry Ellison admitted as much in a 2005 interview when he said:

“That’s one of the unknowables. Am I doing it for purposes of vanity or because of my obligation to the shareholders?”

Current Oracle CEO Safra Katz struck a similar tone in a press conference last year when she spoke about her frustration at being smaller than SAP in the business applications market, saying:

“This is how we feel: silver medal is the first loser.”

It’s not hard to imagine that ego can drive executives to overpay for acquisitions so they can get bigger and bigger, or so that they can stop a competitor from getting bigger than them.

Certainly one has to imagine ego played a role in Elon Musk’s decision to have his highflying company Tesla (TSLA) bailout his struggling company SolarCity (SCTY). The announcement sent Tesla shares plummeting, but at least he doesn’t have to see a company he founded go under.

The Pollyanna Principle

Finally, overpriced acquisitions can happen because everybody—executives, directors, shareholders, etc.—fall prey to basic psychological biases. Most importantly, people are susceptible to what’s known as the Pollyanna Principle, the tendency to overrate positive memories and discount negative ones. It’s the reason everyone thinks music was better when they were young, and it’s the reason companies can talk themselves into deals at absurd valuations.

After all, sometimes seemingly overpriced deals do work out. People scoffed at EBay (EBAY) buying PayPal (PYPL) for $1.5 billion in 2002, or Google (GOOGL) paying $1.6 billion for YouTube in 2006, and those deals turned out to be massive winners.

The Pollyanna Principle causes people at all levels of the deal making process to overrate these success stories and ignore counterexamples such as the disastrous AOL/Time Warner merger that led to a $45 billion write-down.

What This Means For Investors

The recent overpriced acquisitions haven’t shaken our conviction in our models. The evidence still shows that ROIC and cash flows are the ultimate drivers of value. Still, it’s always important to remember the words of legendary investor Benjamin Graham:

“In the short run, the market is a voting machine, but in the long run, it is a weighing machine.”

Fundamentals may drive long-term valuations, but in the short-term it’s greed, fear, ego, and bias that swing prices. We tend to think of corporations as rational economic actors, but they’re run by humans that have biases. With so much capital available for acquisitions, those emotions and biases are causing prices to diverge significantly from fundamentals.

So how are we responding?

- We’re putting a greater weight on the risk of an acquisition, or “Stupid Money” risk, when considering which stocks to put into the Danger Zone.

- For investors that decide to short stocks we put in the Danger Zone, we’re going to be more aggressive about closing out those calls after a significant drop. Even if the stock might have further to fall, we’re going to err on the side of caution so that an acquisition offer doesn’t erase those gains.

- We’ve begun a model portfolio of highly rated stocks that link executive compensation to ROIC. Investors can feel secure that these companies are incentivizing executives to be responsible stewards of capital and shouldn’t destroy shareholder value through overpriced acquisitions.

Buying stock in companies with high and rising economic earnings combined with low market expectations for future growth continues to be the best way to succeed in the market long-term. Still, these short-term risks are worth taking into account.

This article originally published here on July 19,2016.

Disclosure: David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, style, or theme.