We closed the JCP position on November 16, 2020. A copy of the associated Position Update report is here.

Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life.

A new accounting rule added nearly $3 trillion to corporate balance sheets in Q1. Operating lease obligations, formerly buried in the footnotes, must now be reported as a liability – and corresponding right of use asset – on the balance sheet.

We applaud the FASB for removing the loophole that allowed companies to hide trillions of dollars in capital off the balance sheet. However, the new rule is not perfect. Corporate management have significant discretion in how they disclose operating lease obligations on the balance sheet. Specifically, management can choose the discount rate used to calculate the value of these operating lease obligations.

We’ve identified two companies that use unusually high discount rates to reduce and, perhaps, understate their reported operating lease burden. JC Penney (JCP: $1/share) and Diversicare Healthcare Services (DVCR: $3/share) are in the Danger Zone.

How Discount Rates Impact the Balance Sheet

A company can lease assets in one of two ways: capital leases or operating leases.

Capital leases effectively act as debt to own the underlying asset leased. A simple analogy is taking out a loan to purchase a car or home; payments are made periodically and, at the end of the term, the asset is owned outright with the loan repaid.

Operating leases do not transfer ownership of the underlying asset, and payments are made for usage of the asset. A simple analogy here is leasing a car from a dealer; the lessee makes payments for the right to use the car, but does not gain equity in the car itself and will not own the car at the end of the lease.

However, just as a car is a crucial long-term asset to a household, companies often rely on leases to finance key assets for their business. Retailers often lease the real estate for their stores, and airlines almost exclusively obtain their planes through leases. These leases often cover long time periods (sometimes as long as 99 years), so in effect they function, economically, as a form of debt.

Since operating leases are a form of debt, the lease payments running through income statements represent, in effect, a combination of depreciation and the implied interest payment for the debt. We use the term “implied” to describe the interest payment because there is no official interest payment. There is no official interest rate for the unofficial debt either.

However, under the new FASB rule, companies are required to estimate an implied interest rate. This interest rate is used to discount future lease obligations to their present value, i.e. the operating lease liability they report on the balance sheet. This methodology creates two significant issues:

- A company that is already at a high risk of bankruptcy will have a high implied interest rate. This high interest rate means the company will heavily discount future lease obligations, reducing its reported lease liability on the balance sheet. As a result, a high-risk company will appear to have lower liabilities than an equivalent company with less credit risk.

- Under the new FASB rule, companies have significant discretion in how they determine the discount rate. As long as it can plausibly justify the value to regulators, a company can use an artificially high discount rate to reduce its reported lease liability.

In order to prevent these issues from distorting our cash flow and valuation models, we use a standardized implied discount rate, 5.1%, across all companies. The 5.1% discount rate equals the mean-reverting weighted average cost of debt for the ~2,800 companies we cover. By using the same discount rate across all companies, we ensure that the operating lease assets and liabilities are more comparable between companies.

Figure 1 shows that JC Penney and Diversicare significantly understate their lease liabilities compared to our calculation by using abnormally high discount rates.[1]

Figure 1: Companies with Outlier Discount Rates

Sources: New Constructs, LLC and company filings

Why Discount Rates Matter

As Figure 1 shows, the difference between the reported lease liability and the lease liability we show for JCP is $457 million, or 120% of the market cap of the company. Investors who do not adjust JCP’s reported debt will have a distorted view of the company’s liabilities.

For JCP and ~2,700 other companies we cover that have operating lease liabilities, analyzing the operating lease disclosure in the footnotes is critical to a gaining a true understanding of their profitability and valuation. Accordingly, we will continue to analyze footnotes and adjust all reported operating lease assets and liabilities rather than just using the value on the balance sheet.

Below, we dig deeper into the lease footnotes and obligations for JCP and DVCR to better understand their impact on the risk and valuation for these companies.

JC Penney (JCP)

It’s no secret that JCP has been circling the drain for years. The company’s revenue has declined in 7 out of the past 10 years, and its return on invested capital (ROIC) fell to 0% in the trailing twelve months (TTM) period. The company barely breaks even on an operating profit basis, and its core business continues to decline. Unsurprisingly, analysts are publicly speculating that the company may face bankruptcy in the near future.

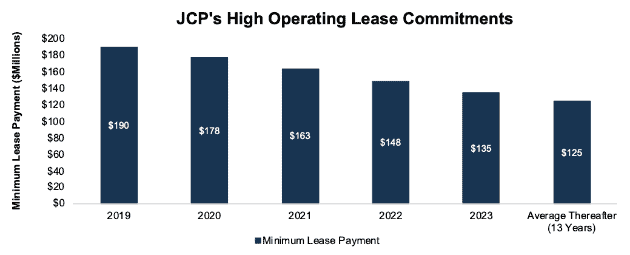

Lease Commitments Increase Bankruptcy Risk: Most of the short-term bankruptcy concerns have focused on the $123 million in principal and interest payments that JCP owes on its debt in 2019, but Figure 2 shows that leases represent an even more significant concern. JCP has minimum payments of $190 million for non-cancelable operating leases in 2019, and while those payments decline going forward, they will remain a substantial burden for many years to come.

Figure 2: JCP’s Operating Lease Commitments by Year

Sources: New Constructs, LLC and company filings

Some investors argue that operating leases should not be thought of as debt and should instead be treated as regular operating costs, like staff salaries or advertising. However, leases differ from these operating costs because they are non-cancelable. If JCP is struggling for cash, it can lay off staff or cut back its operating budget, but it can’t get out of these contracted lease payments.

Valuation Implies Unrealistic Growth: Due to its high levels of debt and minimal profits, JCP has an economic book value – or zero-growth value – of -$4.3 billion. The company needs to improve its cash flows by a significant amount in order to have any value to equity shareholders, much less justify its $380 million market cap.

Our dynamic DCF model quantifies the growth expectations implied by JCP’s stock price. In order to justify its ~$1/share valuation, the company must achieve 3% after tax operating profit (NOPAT) margins (which it hasn’t done since 2011) and grow revenue by 2% compounded annually for the next 5 years. See the math behind this dynamic DCF scenario.

While these expectations may seem low, they’re still highly optimistic for a company that has made no progress in its turnaround goals. In 2016, JCP outlined a strategic vision based on growing private label brands and executing on an omnichannel retail strategy. Since that time, private label brands have remained at ~53% of revenue, well below the company’s 70% target, and JCP recently stopped disclosing its omnichannel sales amidst struggles in that business line.

If investors use JCP’s reported operating lease liability instead of our calculation, the company only needs to hit the assumed 3% margin target – without any revenue growth – to justify its current valuation. Investors who rely on JCP’s balance sheet might think the company can create upside through cost cutting alone, while our model shows that JCP needs to return to growth as well.

Diversicare Healthcare Services (DVCR)

No company faces a larger impact to its balance sheet than DVCR from this new rule. Our initial analysis showed that DVCR had the largest amount of operating leases as a percent of total assets for all of the ~2,800 companies under our coverage.

Rising Lease Burden: When we estimated the impact of adding operating leases to DVCR’s balance sheet, we calculated that it should increase total assets by 411%. Instead, the company’s assets increased by just 233% due to its unusually high 9.9% discount rate.

DVCR’s large lease obligations are crucial to understanding the valuation of this small company. DVCR has a market cap of just $25 million and just $75 million in non-operating lease debt. As a result, the company’s $474 million in operating leases account for ~80% of its total enterprise value.

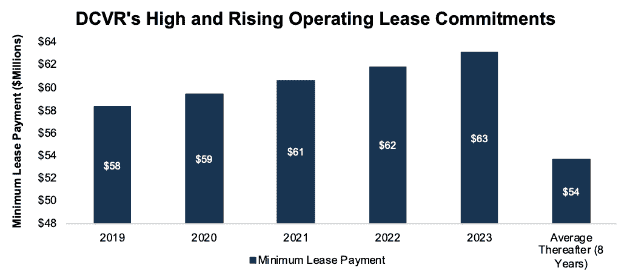

Figure 3 shows that DVCR’s annual operating lease commitments are double its total market cap. Even worse, these payments are rising over the next five years, and still average over $50 million for the following eight years.

Figure 3: DVCR’s Operating Lease Commitments by Year

Sources: New Constructs, LLC and company filings

By using such a high discount rate, DVCR obscures the significant long-term costs it faces from these rising lease obligations.

Valuation Implies Unrealistic Growth: DVCR earns an ROIC of 2%, so it is a slightly healthier business than JCP, but the company still has a negative economic book value of -$373 million.

In order to justify its valuation of ~$3/share, DVCR must immediately achieve 7% NOPAT margins (last achieved in 2016) and grow revenue by 3% compounded annually for the next decade. See the math behind this dynamic DCF scenario.

As with JCP, if we use the reported lease liabilities rather than our calculation, DVCR only needs to expand its margin without growing revenue to justify its valuation. Investors who rely on the balance sheet will significantly underestimate the growth expectations implied by DVCR’s stock price.

This article originally published on June 27, 2019.

Disclosure: David Trainer, Kyle Guske II, and Sam McBride receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] Figure 1 uses Q1 2019 data for reported operating leases because that’s the first period where these leases are disclosed on the balance sheet but FY 2018 data for the calculated lease liability because the disclosure in 10-Ks is superior. In all three cases, the disclosure that does exist in the Q’s suggests that the difference between the two values is due primarily to the discount rate.