This report highlights last month’s top performers and features a stock from the current portfolio. May’s Dividend Growth Stocks Model Portfolio was made available to members on May 30, 2018.

Recap from April’s Picks

Our Dividend Growth Stocks Model Portfolio outperformed the S&P 500 last month. The Model Portfolio rose 1.4% on a price return basis and 1.6% on a total return basis. The S&P 500 rose 0.6% on a price return and total return basis. The portfolio’s best performing stock was Nu Skin Enterprises (NUS), which was up 13%. Overall, 16 out of the 30 Dividend Growth Stocks outperformed the S&P last month, and 19 had positive returns.

The long-term success of our model portfolio strategies highlights the value of our Robo-Analyst technology[1], which scales our forensic accounting expertise (featured in Barron’s) across thousands of stocks[2].

The methodology for this model portfolio mimics an All-Cap Blend style with a focus on dividend growth. Selected stocks earn an Attractive or Very Attractive rating, generate positive free cash flow (FCF) and economic earnings, offer a current dividend yield >1%, and have a 5+ year track record of consecutive dividend growth. This model portfolio is designed for investors who are more focused on long-term capital appreciation than current income, but still appreciate the power of dividends, especially growing dividends.

Featured Stock from May: PepsiCo Inc. (PEP: $100/share)

PepsiCo (PEP), a global food and beverage company, is the featured stock from May’s Dividend Growth Stocks Model Portfolio. PEP was previously featured as a Long Idea in September 2017 and is currently on our Focus List – Long Model Portfolio.

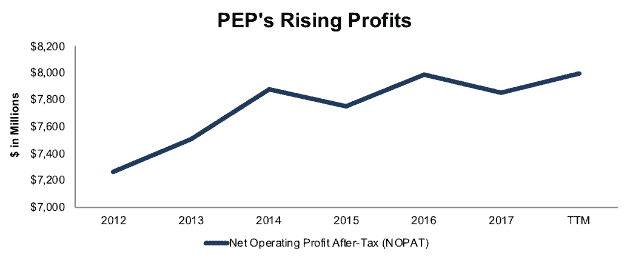

Since 2007, PEP has grown after-tax profit (NOPAT) by 3% compounded annually to $7.8 billion in 2017. Over the last twelve months, PEP’s NOPAT has increased to $8 billion. PEP’s NOPAT margin has improved from 11% in 2012 to 12% TTM while its return on invested capital (ROIC) has averaged 10% over the past five years.

Figure 1: PEP After-Tax Operating Profit Since 2012

Sources: New Constructs, LLC and company filings

Steady Dividend Growth Supported by FCF

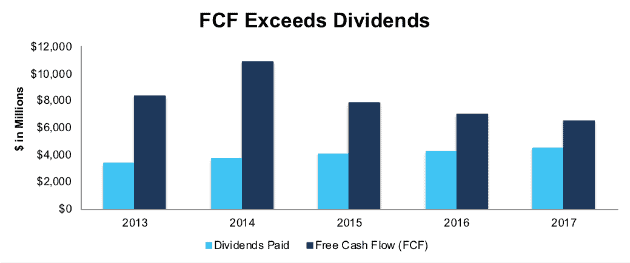

PEP has increased its annual dividend each of the last 45 years. The current annualized dividend has grown from $2.24/share in 2013 to $3.17/share in 2017, or 9% compounded annually. Positive FCF has fueled dividend growth in the past and should continue to do so in the future. From 2013-2017, PEP generated cumulative FCF of $40.4 billion (28% of market cap), which is more than double the $19.9 billion in dividends paid over the same time.

Companies with FCF well in excess of dividend payments provide higher quality dividend growth opportunities because we know the firm generates the cash to support the current dividend as well as a higher dividend. On the flip side, the dividend growth trajectory of a company where FCF falls short of the dividend payment over time cannot be trusted to grow or sustain its dividend because of inadequate free cash flow.

Figure 2: Free Cash Flow (FCF) vs. Regular Dividend Payments

Sources: New Constructs, LLC and company filings

PEP Presents Significant Upside Potential

At its current price of $100/share, PEP has a price-to-economic book value (PEBV) ratio of 1.0. This ratio means the market expects PEP’s NOPAT to never meaningfully grow over the remaining life of the corporation. This expectation seems overly pessimistic for a firm that has grown NOPAT by 3% compounded annually over the past decade and 7% compounded annually since 1998.

If PEP can maintain current NOPAT margins (12% TTM) and grow NOPAT by just 3% compounded annually over the next decade, the stock is worth $132/share today – a 32% upside. Click here to see the math behind this dynamic DCF scenario. Add in PepsiCo’s 3.7% dividend yield and history of dividend growth, and it’s clear why this stock is in May’s Dividend Growth Stocks Model Portfolio.

Critical Details Found in Financial Filings By Our Robo-Analyst Technology

As investors focus more on fundamental research, research automation technology is needed to analyze all the critical financial details in financial filings. Below are specifics on the adjustments we make based on Robo-Analyst findings in PepsiCo’s 2017 10-K:

Income Statement: we made $6.3 billion of adjustments with a net effect of removing $3 billion in non-operating expense (5% of revenue). We removed $4.6 billion related to non-operating expenses and $1.7 billion related to non-operating income. See all adjustments made to PEP’s income statement here.

Balance Sheet: we made $55.9 billion of adjustments to calculate invested capital with a net increase of $17.7 billion. The most notable adjustment was $13.5 billion (23% of reported net assets) related to goodwill. See all adjustments to PEP’s balance sheet here.

Valuation: we made $71.9 billion of adjustments with a net effect of decreasing shareholder value by $32.9 billion. Apart from $45.1 billion in total debt, which includes $1.6 billion in operating leases, the largest adjustment to shareholder value was $17.4 billion in excess cash. This cash adjustment represents 12% of PEP’s market value. Despite the decrease in shareholder value, PEP remains undervalued.

This article originally published on June 5, 2018.

Disclosure: David Trainer, Kyle Guske II, and Sam McBride receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] Harvard Business School features the powerful impact of our research automation technology in the case New Constructs: Disrupting Fundamental Analysis with Robo-Analysts.

[2] Ernst & Young’s recent white paper “Getting ROIC Right” proves the superiority of our holdings research and analytics.

Click here to download a PDF of this report.

Photo Credit: Pictures of Money (flickr)