We published an update on this Danger Zone pick on March 31, 2025. A copy of the associated report is here.

GitLab Inc. (GTLB: $57.50/share midpoint of IPO price range), a software development platform, is set to IPO soon with a price range of $55-60/share. At the midpoint of that range, the firm would have a valuation of $8.2 billion and earn our Unattractive rating.

GitLab is a subscription based SAAS company with a large total addressable market (TAM), which may entice investors. However, the firm sells to only a tiny portion of its TAM and is competing against some of the largest technology companies in the world. With worst-in-class fundamentals and an already overpriced valuation, we don’t think investors should expect to make any money in this stock.

We believe the stock is worth as little as ~$770 million or $5/share, 91% below the midpoint of the expected price range. An $8 billion valuation implies that GitLab will achieve very optimistic milestones, including reversing a downward trend in profits, growing revenue by more than 17x, and nearly tripling its current market share.

With only ~21 months of cash to cover its current cash burn rate, GitLab’s current owners need this IPO to help the company avoid bankruptcy. We don’t think new investors should bail them out.

Freemium Model Is Not Profitable

GitLab’s model for growing revenue is based on the freemium model: gain users with a free version of its software and convert those users to paying members. As of June 2021, GitLab had 30 million free users with just 15,356 paying users.

In other words, GitLab has converted less than 1% of its user base, which is well below the average estimated freemium conversion rate of 2-5%. Most of these converted users are also on lower priced, less profitable plans. GitLab notes that it has 3,632 “base customers”, which generate more than $5,000 in annual recurring revenue (ARR). It discloses only 383 customers generating $100,000+ in ARR.

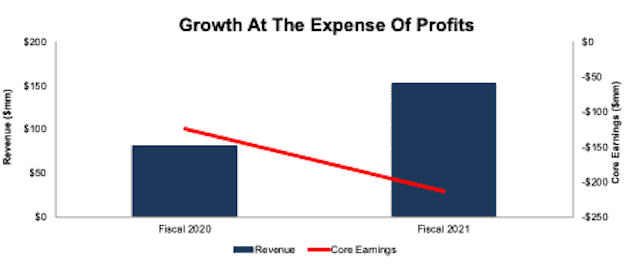

This model has proven capable of driving revenue growth, as GitLab’s revenue grew 87% year-over-year (YoY) in fiscal 2021. However, Core Earnings[1] fell from -$125 million to -$213 million over the same time.

Figure 1: GitLab’s Revenue & Core Earnings: 2019-2020

Sources: New Constructs, LLC and company filings

GitLab’s strategy is clearly focused on growing its top line and forgoing profitability for now. While GitLab’s net operating profit after-tax (NOPAT) margin improved slightly from -158% in fiscal 2020 to -141% in fiscal 2021, it remains highly negative. Additionally, the firm’s return on invested capital (ROIC) declined from -41% to -76% over the same time. GitLab’s economic earnings, the true measure of cash flows, declined from -$149 million in fiscal 2020 to -$229 million in fiscal 2021. Despite growing its top line, GitLab is destroying shareholder value.

Small Share of a Large Market

GitLab operates in the highly competitive infrastructure software market, which the firm notes in its S-1 is estimated to be worth $328 billion in 2021 and grow to $458 billion in 2024, or 12% compounded annually. Such a large TAM may entice investors looking for another tech growth story.

However, Gitlab recognizes that it cannot provide products to the entire TAM and, instead, aims to serve $43 billion of the industry in 2021 and $55 billion in 2024. At its current run rate revenue[2] of $233 million, Gitlab has just 0.5% share of its “serviceable” market in 2021.

If we narrow in on the Global DevOps segment of the infrastructure software market, the expected CAGR is higher, but the addressable market is much smaller. Global Industry Analysts projects the Global DevOps market will grow by 20% compounded annually through 2026 to reach $18 billion. Regardless of the addressable market, Gitlab’s IPO valuation implies it will take significant share and grow much faster than either of these market projections, as we’ll show below.

GitLab Competes Against Industry Giants

Some of GitLab’s closest competition comes from massive incumbents such as Microsoft (MSFT), Amazon (AMZN), Oracle (ORCL), International Business Machines (IBM), and Atlassian Corp (TEAM). This market is dominated by established tech companies that are consistently taking market share.

According to the International Data Corporation, Microsoft and Amazon Web Services both hold 13% of the revenue share in the public cloud services market in 2020, which includes infrastructure, system infrastructure, platform, and software-as-a-service providers. In total, the top five companies, including Microsoft, Amazon, Salesforce (CRM), Oracle, and Google (GOOGL), hold 38% of market share.

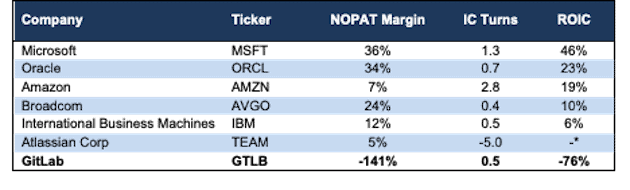

Not only do industry incumbents hold significantly more market share than GitLab, but they are also significantly more profitable. Per Figure 2, GitLab has the worst NOPAT margin and ROIC in the industry by a wide margin. GitLab’s grow-at-all-costs mentality has driven profits into the ground. Given that GitLab burned $158 million in free cash flow (FCF) in fiscal 2021 and has just $283 million in cash and equivalents on its balance sheet, this company needs the IPO cash infusion to remain a going concern. Should operational efficiencies not improve, another equity or debt offering could be needed.

Figure 2: GitLab’s Profitability Vs. Competitors (TTM)

Sources: New Constructs, LLC and company filings

*A top quintile “-“ ROIC indicates a company has positive NOPAT and negative invested capital

Competitors Can Afford the Freemium Model

GitLab’s closest competitor, GitHub, was acquired by Microsoft in 2018. As a cash generating machine, Microsoft can easily afford to offer GitHub services at or below cost in an effort to gain market share and bring users into the Microsoft platform that can monetize the customer relationship in myriad other ways. We are not surprised that, in April 2020, GitHub announced its core features would be free to all users and cut its lowest price plan from $9 per user per month to $4 per user per month. Nor are we surprised that GitHub has 70 million users, or more than twice GitLab’s 30 million.

GitHub isn’t the only competitor with an owner that can afford to use it as a loss leader to grow users. For instance, IBM acquired competitors RedHat in 2019 and UrbanCode in 2013. Atlassian operates competitor Jira alongside many other collaboration/development tools.

The bottom line here is that GitLab’s dependence on one revenue stream is a major competitive disadvantage as it attempts to compete with profitable firms that have many other revenue streams to support loss-leaders.

Scaled Down Research & Development Boosts Margins, But Could Hurt Long-Term

GitLab recently improved its operating margins to -52% over the six months ended July 31, 2021 versus -95% in the six months ended July 31, 2020.

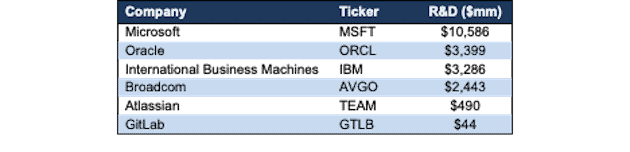

However, much of this improvement came from a significant slowdown in research and development spending. From fiscal 2020 to fiscal 2021, R&D costs increased 79%. In the six months ended July 31, 2021, R&D increased just 13% YoY. While the slowdown in R&D spending certainly helps operating margins in the near term, it could limit the firm’s ability to innovate, improve products and grow revenue in the future, especially given the expansive R&D budgets of its largest competitors.

Figure 3: GitLab’s R&D vs. Competitors (Last Two Fiscal Quarters)

Sources: New Constructs, LLC and company filings

GitLab recognizes that R&D spending to its goal of releasing new features each month, and the company plans “to continue significant investments in research and development.” Should the firm scale R&D back up on par with levels seen in fiscal 2021, the near-term improvement in operating margin would prove a temporary blip for an already highly unprofitable company.

Open Source Is More Accessible, But Creates Risks

One of GitLab’s stated selling points is that many of its features are open source, which allows users to customize their experience and create maximum value out of the service. While this business model is attractive to the developer community, it also opens the company to risks that investors need to know about.

In its S-1 GitLab admits “We face heighted risk of security breaches because we use third-party open source technologies and incorporate a substantial amount of open source code in our products.” Additionally, GitLab notes that by incorporating products subject to open source software licenses, which grant broad permission to use, copy, modify, and redistribute the covered software, the value of its software copyright assets is limited.

If GitLab becomes the target of any cyber-attack as a result of its open source code, it would be more difficult to weather reputational and financial damage because it is already so unprofitable.

Don’t Bet on a Buyout

While a buyout might be the best bet that investors could hope for, it is unlikely the firm will be an acquisition target at a valuation as high as the one expected for the IPO. While most of its competitors have enough cash to buy GitLab, it would make little financial sense for them to do so when compared to previous acquisitions. For example, when Microsoft acquired GitHub, it did so at “close to 30x annual recurring revenue” multiple. If we assume a similar multiple on GitLab’s $233 million in run rate revenue as of July 31, 2021, the firm would be valued at $7.0 billion at most, or 15% below the midpoint of the IPO price range.

$8.2 Billion Valuation = GitLab Must Triple Its Market Share

When we use our reverse discounted cash flow (DCF) model to analyze the future cash flow expectations baked into GitLab’s IPO valuation, we can provide clear, mathematical evidence that the midpoint of the IPO price range valuation is too high and offers unattractive risk/reward.

In order to justify the midpoint of its IPO price range, or $8.2 billion, GitLab must:

- Immediately achieve a 17% NOPAT margin (above IBM, but below Microsoft, compared to GitLab’s -141% TTM NOPAT margin) and

- grow revenue by 50% compounded annually for the next seven years (equal to 2.5x the projected industry growth rate)

In this scenario, GitLab would generate $2.6 billion in revenue in fiscal 2028, which is more than 17x its fiscal 2021 revenue. GitLab’s NOPAT in this scenario would also improve to $442 million in fiscal 2028, up from -$214 million in fiscal 2021 and 4x Atlassian’s fiscal 2021 NOPAT.

The implied revenue in this scenario represents 1.4% of GitLab’s serviceable market in 2024. In other words, an $8.2 billion valuation implies GitLab will improve its market share by nearly 3x its current share of 0.5% of its serviceable market in 2021.

DCF Scenario 2: Growth at 2x Industry Expectations = $4.6 Billion Valuation

We review an additional DCF scenario to highlight the downside risk even if GitLab’s revenue growth doubles the expected industry growth rate.

If we assume GitLab:

- immediately achieves a NOPAT margin of 17% and

- grows revenue by 40% compounded annually over the next seven years (double the projected industry growth rate) then

GTLB is worth just $32/share today – a 44% downside to the midpoint of the IPO price range. See the math behind this reverse DCF scenario.

DCF Scenario 3: Growth at Industry Expectations = $766 Million Valuation

We review a third scenario to highlight the downside risk if GitLab’s revenue growth is in line with the expected industry growth rate.

If we assume GitLab:

- immediately achieves a NOPAT margin of 17% and

- grows revenue by 20% compounded annually over the next seven years (equal to the projected industry growth rate) then

GTLB is worth just $5/share today – a 91% downside to the midpoint of the IPO price range. See the math behind this reverse DCF scenario.

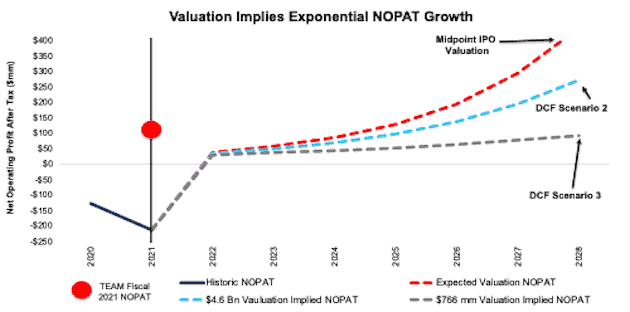

Figure 4 shows GitLab’s historical NOPAT alongside its implied NOPAT in each of the above DCF scenarios.

Figure 4: This IPO Valuation is Unreasonably High

Sources: New Constructs, LLC and company filings

Each of the above scenarios also assumes GitLab grows revenue, NOPAT, and FCF without increasing working capital or fixed assets. This assumption is highly unlikely but allows us to create best-case scenarios that demonstrate the level of expectations embedded in the current valuation.

Other Red Flags for Investors

With a lofty valuation that implies significant improvement in both revenue and profits, investors should be aware that GitLab’s S-1 also includes these other red flags.

Insiders Have Total Control: GitLab will have multiple classes of common stock, with class A shares sold to the public and class B shares reserved for management and the founders. GitLab discloses in its S-1 that each share of class A stock will be entitled to one vote while each share of class B stock will be entitled to 10 votes.

GitLab states in its S-1 that after IPO, holders of class B shares will hold 99% of the voting power, with directors, executive officers, and beneficial owners holding 62% of the voting power.

In other words, despite new investors paying a premium to buy the IPO, GitLab’s insiders and other owners will continue to control the company, and new shareholders will have no control over corporate governance.

Adjusted Numbers Distort Earnings: Many unprofitable companies present non-GAAP metrics to appear more profitable than they really are, and GitLab is no different. GitLab presents non-GAAP operating loss, similar to the popular Adjusted EBITDA metric, as a key performance indicator. Not surprisingly, non-GAAP operating loss gives a more bullish picture of the firm’s business than GAAP net income and our Core Earnings.

For instance, GitLab’s fiscal 2021 non-GAAP operating loss removes $111 million in stock-based compensation expense. After removing all items, GitLab reports a non-GAAP operating loss of -$102 million in fiscal 2021, compared to a GAAP operating loss of -$214 million. Meanwhile, economic earnings, the true cash flows of the business, are significantly lower at -$229 million. GitLab’s non-GAAP operating loss follows the same declining trend in economic earnings over the past two years, but investors need to be aware that there is always a risk that non-GAAP metrics could be used to manipulate earnings going forward.

We Don’t Know If We Can Trust the Financials: Investors should take GitLab’s reported numbers with a grain of salt because the firm is not required to have an auditor provide an opinion on its internal controls. In other words, the firm may have a material weakness with its internal controls that it is unaware of at the time. In its S-1 GitLab acknowledges “weaknesses in our internal controls may be discovered in the future.”

Additionally, the firm uses adjusted numbers and internally developed metrics to track its performance. In its S-1 GitLab admits “We calculate and track performance metrics with internal tools, which are not independently verified by any third-party.”

While the lack of disclosure around the firm’s internal controls over financial reporting and its individual performance metrics may never be an issue, it does increase the risk that the firm’s financials are fraudulent and/or misleading when compared to a firm required to have an auditor attest to its internal controls.

Emerging Growth Status Limits Transparency: By electing to operate as an “Emerging Growth Company”, GitLab is exempt from certain requirements that are beneficial to shareholders. For instance, and as noted above the SEC does not currently require GitLab to have an independent auditor provide an opinion on internal controls. Additionally, GitLab is not required to provide information on executive compensation structure and can delay adoption of certain accounting procedures, which limit the transparency of its financial statements. Get more details on the risks of investing in emerging growth companies here.

Critical Details Found in Financial Filings By Our Robo-Analyst Technology

Fact: we provide superior fundamental data and earnings models – unrivaled in the world.

Proof: Core Earnings: New Data and Evidence, published in The Journal of Financial Economics.

Below are specifics on the adjustments we make based on Robo-Analyst findings in GitLab’s S-1:

Income Statement: we made $28 million in adjustments, with a net effect of removing $22 million in non-operating income (14% of revenue). You can see all the adjustments made to GitLab’s income statement here.

Balance Sheet: we made $47 million in adjustments to calculate invested capital, all of which increased invested capital. The most notable adjustment was $20 million in other comprehensive income. This adjustment represented 8% of reported net assets. You can see all the adjustments made to GitLab’s balance sheet here.

Valuation: we made $965 million in adjustments to shareholder value, all of which decreased shareholder value. The largest adjustment to shareholder value was $540 million in outstanding employee stock option (ESO) liability. This adjustment represents 7% of GitLab’s valuation at the midpoint of its IPO price range. You can see all the adjustments made to GitLab’s valuation here.

This article originally published on October 8, 2021.

Disclosure: David Trainer, Kyle Guske II, Alex Sword, and Matt Shuler receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] Only Core Earnings enable investors to overcome the flaws in legacy fundamental research, as proven by The Journal of Financial Economics.

[2] Gitlab calculates run rate revenue as revenue for the three months ended July 31, 2021 multiplied by 4.