Picking good stocks is hard, which is why many investors are drawn to ETFs and mutual funds. However, most ETFs and mutual funds are not good substitutes for picking good stocks. Most of them pick bad stocks and charge high fees for this disservice.

This week’s Danger Zone pick is a fund that allocates too much capital to bad stocks. To make matters worse, it charges well above-average fees. Talk about a double whammy.

Look out, Morningstar gives this fund 5 stars!

We think you should steer clear of this fund.

Last week, we highlighted a mutual fund as our Long Idea to promote our 3Q25 ETF and mutual fund sector and style ranking reports. This week, we are showing you the other side of the coin by highlighting a mutual fund that you should sell immediately.

We all know that past performance is not an indicator of future performance, yet nearly all fund research firms (other than ours) base their ratings on past performance. We think the quality of the fund’s underlying individual stocks matters more than past performance. Strong holdings are what ultimately drive fund performance.

This week’s Danger Zone pick is a fund that allocates too much capital to bad stocks. To make matters worse, it charges well above-average fees, especially considering its below average portfolio. Donoghue Forlines Momentum Fund (MOJAX) is this week’s Danger Zone pick.

Forward-Looking Research Protects Investors

While legacy fund research is backward-looking, our fund research is forward-looking and based on proven-superior fundamental analysis and ratings on each individual holding.

MOJAX earns our Very Unattractive (equivalent to Morningstar’s 1 Star) rating while Morningstar gives the fund a 5 Star rating. Figure 1 shows how our forward-looking Fund Ratings compare to Morningstar’s (MORN) ratings.

MOJCX, one of the other share classes of the mutual fund, earns a 5 Star rating while we rate it Unattractive. MOJOX earns a 5 Star rating while we rate it Neutral.

Figure 1: Donoghue Forlines Momentum Fund Ratings

Sources: New Constructs, LLC, company filings, mutual fund filings, and Morningstar

Fund Methodology Looks Good on Paper, But Not in Practice

Donoghue Forlines Momentum Fund follows a strategy based on what the advisor calls the “Momentum Index”, which provides a “formulaic methodology for allocating investments between securities of issuers who demonstrate positive free cash flow (FCF) and positive momentum, and short-term treasuries (maturity of 1 to 3 years).” This Momentum Index only includes companies with positive FCF over the previous twelve months.

The fund’s prospectus mentions that the methodology of the “Momentum Index” is designed to convey the benefits of high FCF and momentum, sector diversification and equal weighting. The fund’s advisor uses moving average indicators to allocate more to the equity portfolio or treasury portfolio, based on whether the indicators lean bullish or defensive.

Even with details behind the advisors’ “rules-based, tactical allocation methodology”, we prefer to judge MOJAX’s managers based on what we can measure: the quality of the stocks they hold in their fund. And MOJAX’s subpar holdings tell us that management isn’t identifying companies with strong risk/reward, but rather highly overvalued stocks, as we’ll show below.

Our analysis reveals MOJAX’s investment process leads to holdings with lower returns on invested capital (ROIC), lower cash flows, and more expensive valuations than its benchmark and the S&P 500. See below.

Holdings Research Reveals a Low-Quality All Cap Blend Portfolio

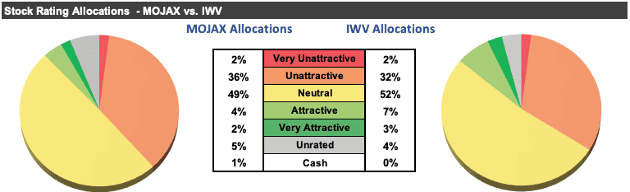

Our holdings analysis, which leverages our Robo-Analyst technology[1], reveals that MOJAX holds lower-quality stocks than its benchmark iShares Russell 3000 ETF (IWV). For reference, IWV earns an Attractive rating.

Per Figure 2, MOJAX allocates 38% of its portfolio to Unattractive-or-worse rated stocks compared to 34% for IWV. On the flip side, MOJAX allocates only 6% of its assets to Attractive-or-better rated stocks compared to 10% for IWV.

Figure 2: Donoghue Forlines Momentum Fund Allocates to Far Worse Stocks than IWV

Sources: New Constructs, LLC, company, ETF, and mutual fund filings

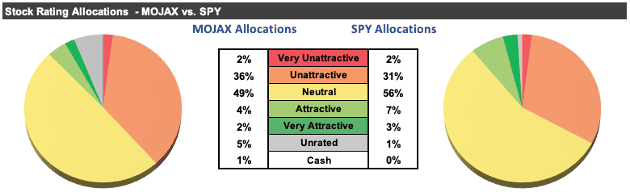

Per Figure 3, our holdings analysis also reveals MOJAX’s portfolio is lower quality than the S&P 500, as represented by State Street SPDR S&P 500 ETF (SPY), which earns an Attractive rating.

At just 33% of its portfolio, SPY allocates less to Unattractive-or-worse rated stocks compared to MOJAX. SPY also allocates more to Attractive-or-better rated stocks compared to MOJAX, at 10% of its portfolio.

Figure 3: Donoghue Forlines Momentum Fund Allocates to Worse Stocks than SPY

Sources: New Constructs, LLC, company, ETF, and mutual fund filings

Given MOJAX allocates just 6% of assets to Attractive-or-better rated stocks, it appears poorly positioned to generate the outperformance required to justify higher active management fees.

Expensive Stocks Drive Very Unattractive Risk/Reward Rating

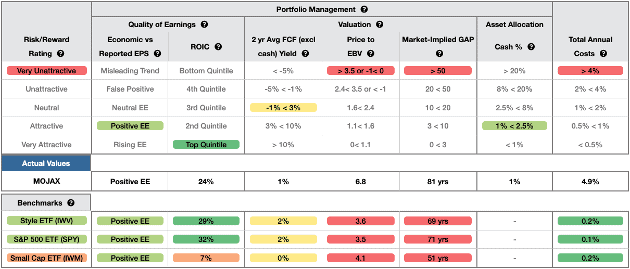

Figure 4 shows our detailed rating for MOJAX, which includes each of the criteria we use to rate all ETFs and mutual funds under coverage. These criteria are the same for our Stock Rating Methodology, as the performance of a mutual fund equals the performance of its holdings minus fees. Figure 4 also compares MOJAX’s rating with those of IWV and SPY.

Figure 4: Donoghue Forlines Momentum Fund Rating Details

Sources: New Constructs, LLC, company, ETF, and mutual fund filings

As Figure 4 shows, MOJAX is inferior to IWV and SPY in four of the five criteria that make up our Portfolio Management rating. Specifically:

- MOJAX’s holdings generate positive economic earnings, same as IWV and SPY.

- MOJAX’s ROIC is 24%, which is lower than IWV’s (29%) and SPY’s (32%) ROIC.

- MOJAX’s 2-yr average free cash flow (FCF) yield of 1% is lower than IWV’s and SPY’s at 2%.

- The price-to-economic book value (PEBV) ratio for MOJAX is 6.8, which is greater than the 3.6 for IWV and 3.5 for SPY.

- Our discounted cash flow (DCF) analysis reveals an average market-implied growth appreciation period (GAP) of 81 years for MOJAX’s holdings compared to 69 years for IWV’s and 71 years for SPY’s holdings.

In other words, market expectations for stocks held by MOJAX imply profits will grow substantially more than the stock’s held by IWV and SPY (measured by PEBV ratio), despite IWV’s and SPY’s holdings being more profitable (as measured by ROIC).

This rigorous holdings analysis reveals that MOJAX provides exposure to less profitable companies, while taking much more valuation risk than the benchmark and S&P 500.

High Fees Make Owning MOJAX Worse

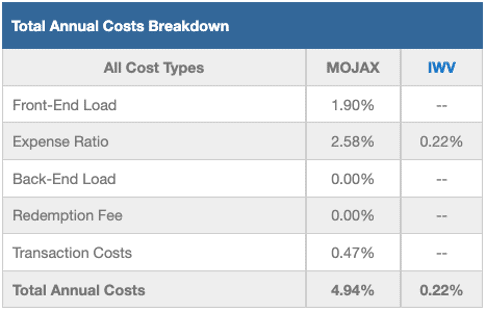

At 4.94%, MOJAX’s total annual costs (TAC) are higher than 98% of All Cap Blend mutual funds under coverage. For comparison, the simple average TAC of all the All Cap Blend mutual funds under coverage is 1.66% and the asset-weighted average is 0.35%. IWV charges just 0.22% and SPY has total annual costs of just 0.10%. Why pay higher fees for inferior stock selection?

Our TAC metric accounts for more than just the expense ratio. We consider the impact of front-end loads, back-end loads, redemption fees, and transaction costs – the latter of which adds 0.47% to MOJAX’s TAC.

Figure 5 shows our breakdown of MOJAX’s total annual costs, which we provide for all ~6,400+ mutual funds and ~1,200+ ETFs under coverage.

Figure 5: Donoghue Forlines Momentum Fund’s Total Annual Costs Breakdown

Sources: New Constructs, LLC, company, ETF, and mutual fund filings

To justify charging higher fees, MOJAX must outperform its benchmark by 472 basis points annually over three years.

However, MOJAX’s load-adjusted 1-year quarter-end average annual total return has underperformed IWV by 614 basis points and SPY by 606 basis points. MOJAX has also underperformed over the 3-year and 5-year periods.

Given that 38% of assets are allocated to stocks with Unattractive-or-worse ratings, and 87% are allocated to stocks with Neutral-or-worse ratings, MOJAX is likely to continue underperforming.

Get an Edge from Holdings-Based Fund Analysis Based on Superior Stock Research

We offer clients in-depth reports for all ~7,600+ ETFs and mutual funds under coverage. Click below for a free copy of our MOJAX standard mutual fund report.

Smart fund (or ETF) investing means analyzing each of the holdings of a fund. Failure to do so is a failure to perform proper due diligence. Simply buying an ETF or mutual fund based on past performance does not necessarily lead to outperformance. Only thorough holdings-based research can help determine if a fund’s methodology leads managers to pick high-quality or low-quality stocks.

Our Robo-Analyst technology analyzes the holdings of all 821 ETFs and mutual funds in the All Cap Blend style and 7,600+ ETFs and mutual funds under coverage to avoid “the danger within”.

Easily Make Any Fund, Even MOJAX, Better

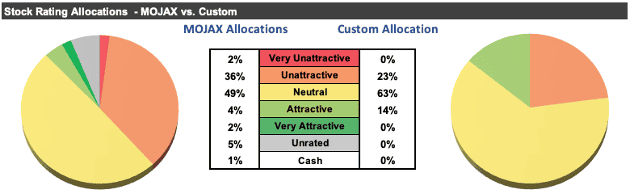

As we show in The Paradigm Shift to DIY ETFs, new technologies enable investors to create their own fund without any fees while also enabling better, more sophisticated weighting methodologies. For example, if we reallocate the fund’s capital to the companies with the best Free Cash Flow Yield, our customized fund allocates more capital to better stocks:

- 14% of assets to Attractive-or-better rated stocks (compared to 6% for MOJAX)

- 23% of assets to Unattractive-or-worse rated stocks (compared to 38% for MOJAX)

Compare the quality of stock allocation in as-is MOJAX vs. our customed version of MOJAX in Figure 6. While we can’t fix the bad stock picks, we can, at least, be sure to allocate more capital to the better stocks.

Figure 6: Donoghue Forlines Momentum Fund Allocation Could Be Improved

Sources: New Constructs, LLC, company, and mutual fund filings

Note that our DIY ETF tool allows clients to pick and weight portfolio holdings based on multiple proprietary metrics, such as Core Earnings, Economic Earnings, ROIC, Net Operating Profit After Tax and more.

Check Out the Indices Based on New Constructs Research

While we’re writing about creating your own fund, we should highlight the indices we’ve developed with Bloomberg’s Index Licensing Group. All three outperformed the S&P 500 in 1H25. See Figures 7-9.

- Bloomberg New Constructs Core Earnings Leaders Index (ticker: BCORET:IND)

- Bloomberg New Constructs Ratings VA-1 Index (ticker: BNCVA1T:IND)

- Bloomberg New Constructs 500 Index (ticker: B500NCT:IND)

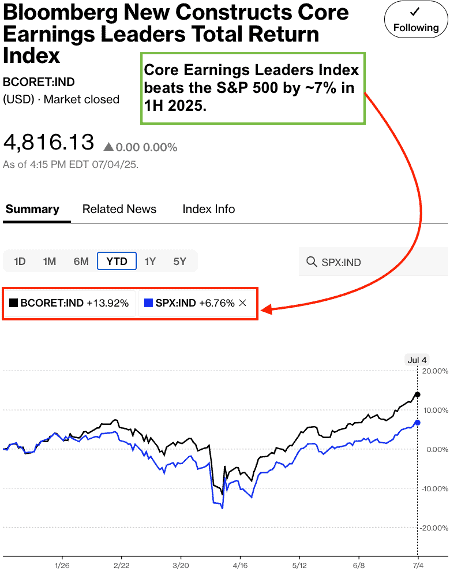

The Bloomberg New Constructs Core Earnings Leaders Index beat the S&P 500 by over 7% in 1H25. Our Index (ticker: BCORET:IND) was up 13.9% while the S&P 500 was up 6.8%. That’s pretty good! See Figure 7 for details.

Figure 7: Bloomberg New Constructs Core Earnings Leaders Index Outperforms the S&P 500 in 1H25

Sources: Bloomberg as of July 4, 2025

Note: Past performance is no guarantee of future results.

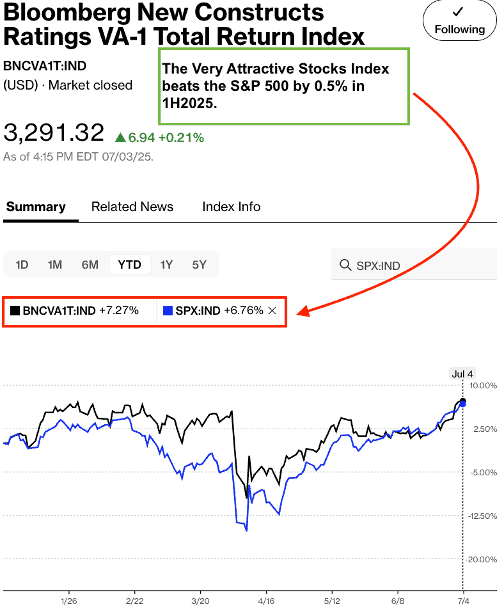

The “Very Attractive Stocks” Index beat the S&P 500 by over 0.5% in 1H25. Bloomberg’s official name for the index is Bloomberg New Constructs Ratings VA-1Index (ticker: BNCVAT1T:IND). Figure 8 shows it was up 7.3% while the S&P 500 was up 6.8%.

Figure 8: Very Attractive-Rated Stocks Strongly Outperform the S&P 500 in 1H25

Sources: Bloomberg as of July 4, 2025

Note: Past performance is no guarantee of future results.

Our “Core-Earnings Weighted S&P 500” Index beat the S&P 500 by over 0.3% in 1H25. Bloomberg’s official name for the index is Bloomberg New Constructs 500 Total Return Index (ticker: BNCVAT1T:IND). Figure 9 shows it was up 7.1% while the S&P 500 was up 6.8%.

Figure 9: Bloomberg New Constructs 500 Index Strongly Outperforms the S&P 500 in 1H25

Sources: Bloomberg as of July 4, 2025

Note: Past performance is no guarantee of future results.

Better Options for All Cap Blend Funds

Below we present All Cap Blend ETFs or mutual funds that feature an Attractive rating, >$100 million in assets under management, and below average TAC:

- Invesco Bloomberg MVP Multi-Factor ETF (BMVP) – 0.32% TAC and Very Attractive rating

- Distillate U.S. Fundamental Stability & Value ETF (DSTL) – 0.43% TAC and Very Attractive rating

- Brown Advisory Beutel Goodman Large Cap Value Fund (BVALX and BIAVX)) – 0.66% TAC and Very Attractive rating

- ETC 6 Meridian Hedged Equity-Index Option Strategy ETF (SIXH) – 0.81% TAC and Very Attractive rating

- Vanguard Total World Stock Index Fund ETF (VT) – 0.07% TAC and Very Attractive rating

This article was originally published on July 21, 2025.

Disclosure: David Trainer, Kyle Guske II, and Hakan Salt receive no compensation to write about any specific stock, sector, style, or theme.

Questions on this report or others? Join our online community and connect with us directly.

[1] See Harvard Business School case study: New Constructs: Disrupting Fundamental Analysis with Robo-Analysts.