GreenSky Inc. (GSKY: $22/share midpoint of IPO price range), a technology platform facilitating consumer loans at the point of purchase, will IPO on Thursday, May 24. At a price range of $21 to $23 per share, the company plans to raise up to $902 million and has an expected market cap of ~$4.1 billion. At the midpoint of its price range, GSKY currently earns our Neutral rating.

GreenSky was recently valued as one of the largest fintech firms in the United States and its IPO is getting a lot attention. Its technology platform allows consumers to access small-balance loans (often with special interest terms) while managing the full loan transaction lifecycle, from application, to funding, to settlement.

While the firm is profitable, unlike some other recent IPOs, it is not without risks. This report aims to help investors sort through GreenSky’s financial filings to understand the fundamentals and valuation of this IPO.

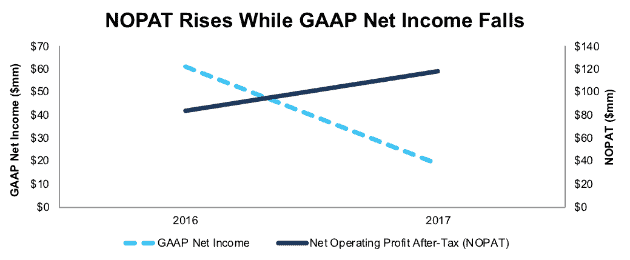

NOPAT Reveals True Profits Are Rising

GSKY monetizes its platform by charging an upfront transaction fee every time a merchant receives a payment using the platform. It also charges the lending banks a recurring servicing fee over the life of a loan. The company notes active merchants grew 52% year-over-year (YoY) while transaction volume (or the dollar value of loans facilitated through GSKY) grew 21% YoY in 2017.

Unlike recent IPOs, GKSY is actually profitable. However, at first glance, GSKY’s 2017 pro-forma net income fell significantly from its net income attributable to class A unit holders in 2016. GAAP net income declined from $61 million in 2016 to $19 million in 2017, or 69%. However, Figure 1 shows that the after-tax operating profit (NOPAT) actually increased from $84 million to $118 million in 2017, or 41% year-over-year.

Figure 1: GKSY GAAP Net Income and NOPAT Since 2016

Sources: New Constructs, LLC and company filings

Non-operating items understated GKSY’s profitability in 2016 and more heavily in 2017, which caused the large decline in accounting results. In 2016, GSKY’s reported profits included a $25 million charge to participating interests, which was included as an operating expense on GSKY’s income statement. We remove this non-operating expense when calculating NOPAT to get at the true recurring profits of the business.

In 2017, Robo-Analyst[1] uncovered larger non-operating expenses, such as:

- $108 million in minority interest expense

- $2.6 million in nonrecurring transaction expenses

- $2.1 million in fair value change in servicing liabilities

After all adjustments, we removed net $99 million in non-operating expenses in 2017.

With only two years of history, it’s hard to draw any firm conclusions about the long-term trend in profitability for GSKY, but our adjustments show that true profits increased in 2017 despite GAAP net income’s large decline.

Asset-Light Business Model Leads to Impressive Profitability

GreenSky operates as a middleman between merchants and banks. The company does not hold or own the loans facilitated through their platform, nor do they need to market directly to consumers. Instead, GSKY leverages its merchant base to offer loan terms which each merchant can then promote to their customers.

This business model enables GSKY to efficiently convert revenue into profits and earn a return on invested capital (ROIC) that ranks near the top of our coverage universe. In 2017, GKSY’s NOPAT margin improved from 32% to 36%. It earns a 150% ROIC, which is seventh highest of the nearly 3000 companies under coverage.

While impressive, it’s also worth noting that such high ROIC businesses often face significant competition. Competitors can see the profit potential relative to the required capital to build the business, and they work hard to get a piece of the profitable market. Well-known firms such as Affirm and PayPal (PYPL) already provide similar loan offerings for online merchants. Beyond these firms, current banking partners could decide that building their own platform is a worthy investment, which would significantly impact GSKY’s very profitable business.

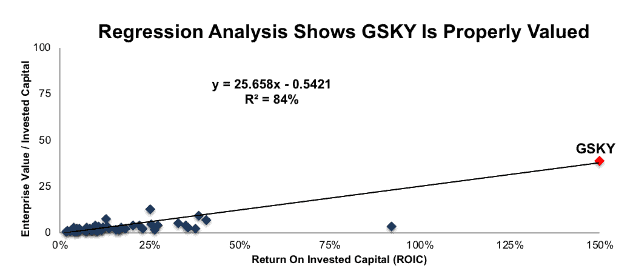

GSKY Looks Fairly Valued at Midpoint of Offering Price

Numerous case studies show that getting ROIC right[2] is an important part of making smart investments. Ernst & Young recently published a white paper that proves the material superiority of our forensic accounting research and measure of ROIC. The technology that enables this research is featured by Harvard Business School.

As Figure 2 shows, ROIC explains 84% of the difference in enterprise value per invested capital (a cleaner version of price to book) for the 63 Banking Services companies we have under coverage.

Figure 2: ROIC vs. Enterprise Value/Invested Capital for GSKY

Sources: New Constructs, LLC and company filings

If GSKY were valued at the same level as its peers, it would be worth $21.60/share, or just 2% below the midpoint of the proposed offering range.

Industry, Customer and Lending Concentration Could Pose Risks

Historically, the home improvement market has represented nearly all of GreenSky’s transaction volume. The company recently expanded into the elective healthcare industry but remains heavily concentrated in the home improvement market. In a growing market, such concentration represents opportunity, but should the home improvement market slow or begin to decline, GSKY’s business would follow suit.

GKSY’s business is also heavily concentrated with specific customers. Renewal by Andersen, a replacement window installer with affiliate dealers around the country, represented 19% of revenue in 2017. The Home Depot (HD) represented 6% of revenue in 2017.

In total, the top ten merchants accounted for 30% of revenue in 2017. This revenue concentration creates risks for GSKY’s business. First, should any of these partners face economic trouble, they may be unwilling to offer special loan terms or may have to cease use of GSKY’s platform. Second, if any of these merchants terminates an existing agreement, GSKY’s revenues and profits would take a big hit. Retailers looking at other financing options is not unheard of either. The Wall Street Journal recently reported that Apple (AAPL) is preparing to launch a joint credit card with Goldman Sachs (GS) and end a longstanding partnership with Barclays (BCS).

Lastly, GSKY’s lending concentration could also pose risks. GSKY relies on banks to originate all of the loans made through its platform. Its four largest bank partners, SunTrust Bank (STI), Regions Bank (RF), Fifth Third Bank (FITB), and Synovus Bank (SNV) provided 89% of the commitments to originate loans as of March 31, 2018. Similar to the merchant concentration above, losing partnership with any of these four banks could leave GSKY without a significant source of loan origination, which would hamper its ability to provide loan offers to consumers.

While each one of these concentration issues may not pose an immediate threat, they add up to GKSY having little leverage over its key partners. Should banks demand better terms on servicing fees, or one of the large merchants require lower transaction fees, GKSY has little bargaining power given the importance (to overall revenues) of each one of its large partners.

Multi Class Share Structure Means Investors Have Nearly No Voting Power

GreenSky plans to follow in the footsteps of EVO Payments (EVOP), Snapchat (SNAP), Dropbox (DBX), and more by using multiple share classes that prevent public investors from having a real say in the governance of the company.

Post-IPO, GreenSky will have two separate share classes. Investors in this offering will own ~83-85% (depending upon underwriter exercise options) of outstanding Class A shares but hold just 2.8% of the voting power in the company.

Class B shares, which have no economic rights but ten votes per share, will hold 97.2% of the voting power in the company. Class B shares will be held by executive officers, directors, and original equity and profit interest holders, such as Pacific Investment Management Company and TPG Georgia Holdings. Each Class B share has the right to exchange shares for newly issues shares of Class A stock on a one-for-one basis.

This poor corporate governance, means investors have largely no say while executives retain control of the company, despite “going public.”

Critical Details Found in Financial Filings By Our Robo-Analyst Technology

As investors focus more on fundamental research, research automation technology is needed to analyze all the critical financial details in financial filings. Below are specifics on the adjustments we make based on Robo-Analyst findings in GreenSky’s 2017 S-1:

Income Statement: we made $155 million of adjustments, with a net effect of removing $99 million in non-operating expense (30% of revenue). We removed $28 million in non-operating income and $127 million in non-operating expenses. You can see all the adjustments made to GSKY’s income statement here.

Balance Sheet: we made $264 million of adjustments to calculate invested capital with a net decrease of $234 million. The largest adjustments was $218 million in excess cash. This adjustment represented 70% of reported net assets. You can see all the adjustments made to GSKY’s balance sheet here.

Valuation: we made $489 million of adjustments with a net effect of decreasing shareholder value by $143 million. The largest adjustment to shareholder value was $361 million in total debt, which includes $15 million in operating leases. This debt adjustment represents 9% of GSKY’s proposed market cap.

This article originally published on May 23, 2018.

Disclosure: David Trainer, Kyle Guske II, and Sam McBride receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] Harvard Business School features the powerful impact of research automation in the case New Constructs: Disrupting Fundamental Analysis with Robo-Analysts.

[2] Ernst & Young’s recent white paper “Getting ROIC Right” demonstrates the link between an accurate calculation of ROIC and shareholder value.