We published an update on this Danger Zone pick on November 7, 2022. A copy of the associated Earnings Update report is here.

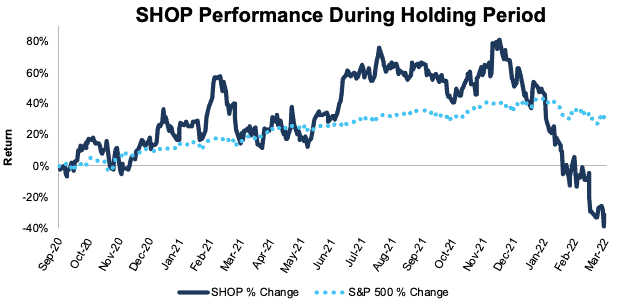

We first put Shopify (SHOP: $600/share) in the Danger Zone in September 2020. Since then, the stock is down 36% compared to a 30% gain for the S&P 500. Though the company benefited greatly from rapid e-commerce adoption in 2021, a continuation of such growth is unlikely, and shares still have further to fall. See our most recent report from August 2021 on Shopify here.

We leverage more reliable fundamental data[1], shown to provide a new source of alpha, with qualitative research to pick this Danger Zone idea.

Shopify’s Stock Has Huge Downside Risk Based On:

- Shopify’s gross merchandise value (GMV) growth rate has fallen below pre-pandemic rates, signaling the end of pandemic-driven growth

- 2022 guidance includes slowing revenue growth rates and higher expenses

- current valuation of the stock implies Shopify’s GMV will be 2x bigger than Amazon’s

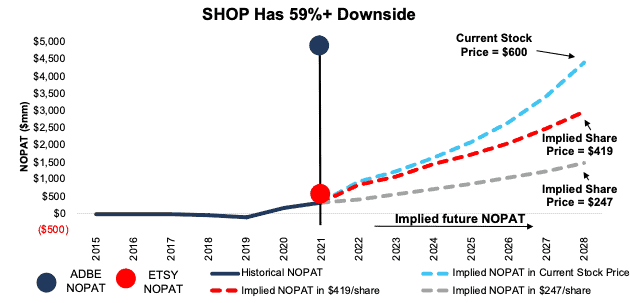

- simple math shows SHOP could fall 59% more, despite already falling 66% from its 52-week high

Figure 1: Danger Zone Outperformance of 65%: From 9/10/20 Through 3/4/22

Sources: New Constructs, LLC

What’s Working for the Business:

The shifting retail landscape throughout each COVID-19 wave drove record revenue growth. Revenue grew 41% year-over-year in 4Q21 and 57% YoY in all of 2021.

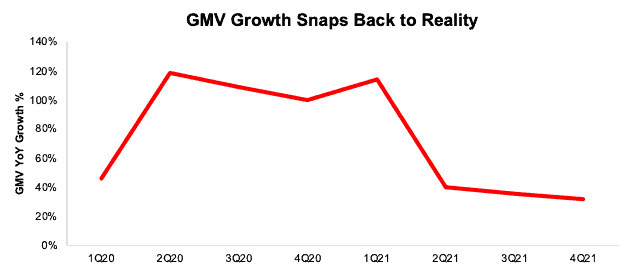

Gross merchandise volume (GMV), the total dollar value of orders facilitated on the Shopify platform, was up 31% YoY in 4Q21 and 47% YoY in 2021. Additionally, Shopify increased adoption of its Shopify Payments solution, from 46% GMV penetration in 4Q20 to 51% GMV penetration in 4Q21.

With record top-line growth, Shopify generated positive net operating profit after-tax (NOPAT) for the second consecutive year and improved its NOPAT margin from 4.8% in 2020 to 6.7% in 2021. However, given management’s guidance for spending moving forward, margins are poised to fall.

What’s Not Working for the Business:

Fundamentals show signs of weakness: Despite improving NOPAT and NOPAT margin, Shopify’s balance sheet efficiency fell significantly in 2021. Invested capital turns fell from 2.3 in 2020 to 1.3 in 2021. This decline offset the improvement in NOPAT margin and drove return on invested capital (ROIC) from 11% in 2020 to 8% in 2021.

Growth rates are already slowing: We already see a slowing of Shopify’s business in 2021, despite record revenue and GMV. Per Figure 2, Shopify’s GMV grew 31% YoY in 4Q21, its slowest YoY growth rate since 1Q20, just before the COVID-19 pandemic began. In fact, annual GMV growth slowed in each of the last three quarters of 2021.

Figure 2: Shopify’s YoY GMV Growth Rate: 1Q20 – 4Q21

Sources: New Constructs, LLC and company filings

2021 growth is unsustainable: The success brought on by COVID-19 shutdowns and subsequent government stimulus is not likely to continue. Management admits as much, noting in its in 4Q21 earnings that “the COVID-triggered acceleration of commerce that spilled into the first half of 2021 in the form of lockdowns and government stimulus will be absent from 2022…”.

Additionally, the current inflationary environment provides a further headwind to growth in 2022, with management noting “there is caution around inflation and consumer spend near term.”

Slower growth and less profitability in 2022: In its guidance for 2022, management noted that revenue growth will be lower than 2021. Consensus revenue estimates call for 31% YoY revenue growth, which, while impressive, would be the slowest YoY growth rate since the company went public in 2015.

At the same time growth is slowing, Shopify is ramping up its spending. The company expects to “reinvest back into our business aggressively throughout 2022” by hiring more engineers and salespeople, while also increasing international marketing efforts. Shopify’s aim to offset decelerating revenue growth with more sales and marketing could hurt profitability. Unfortunately for current shareholders, the stock price implies the company will not only accelerate growth, but also improve margins. Even with the recent stock price decline, shares remain priced for Shopify to be bigger than Amazon, creating significant downside in any other scenario, as we’ll show below.

Shopify Priced for GMV to Be 2x Bigger than Amazon

Despite falling 66% from its 52-week high, Shopify remains significantly overvalued. Below, we use our reverse discounted cash flow (DCF) model to illustrate the lofty expectations for future cash flows implied by Shopify’s current valuation.

To justify its current price of ~$600/share, Shopify must:

- Immediately improve its NOPAT margin to 15% (compared to 7% in 2021) and

- grow revenue at a 30% CAGR through 2028 (over 3x projected global e-commerce market growth through 2028)

In this scenario, Shopify would generate nearly $4.4 billion in NOPAT (13x 2021 NOPAT), which at a 15% NOPAT margin implies $29.2 billion in revenue (6x 2021 revenue). However, this scenario seems unlikely given the need to more than double NOPAT margin while also implementing expected spending increases in 2022.

The rate of sales growth required to justify Shopify’s stock price is, quite simply, astonishing. In the scenario outlined above, assuming the same sales mix as 2021[2], Shopify would generate $1.1 trillion in GMV in 2028 – which would be 14% of the forecasted $7.6 trillion global market for B2C e-commerce forecasted by Research and Markets. To put that market share in context, Amazon’s 2021 GMV totaled 15% of the estimated global market and Shopify’s totaled 4%. If, by 2028, Shopify has not become a more dominant player in e-commerce than Amazon is now, purchasers of the stock at the current price will lose money.

SHOP Has 30%+ Downside: if we assume:

- Shopify improves its NOPAT margin to 13.4% (double 2021 NOPAT margin) and

- revenue grows at consensus rates in 2022, 2023, and 2024 and

- revenue grows 20% a year in 2024-2028 (double e-commerce market CAGR through 2028), then

the stock is worth $419/share today – a 30% downside to the current price. In this scenario, Shopify would earn $2.9 billion in NOPAT in 2028, which is nearly 10x its 2021 NOPAT and 73% of PayPal’s (PYPL) 2021 NOPAT.

SHOP Has 59%+ Downside: if we assume:

- Shopify maintains its NOPAT margin at 7% and

- revenue grows at consensus rates in 2021, 2022, and 2023 and

- revenue grows 20% a year in 2024-2028 (double e-commerce market CAGR through 2028), then

the stock is worth $247/share today – a 59% downside to the current price. In this scenario, Shopify would still earn $1.5 billion in NOPAT in 2028, which is 5x its 2021 NOPAT. In this scenario, if we assume the same revenue to GMV rate as 2021, Shopify generates $836 billion in GMV in 2028, 139% of Amazon’s 2021 GMV.

Figure 3 compares the firm’s historical NOPAT with the implied NOPAT in each of the above scenarios. For additional context, we show Etsy (ETSY) and Adobe’s (ADBE), two providers of competing services, 2021 NOPAT.

Figure 3: Shopify’s Historical vs. Implied NOPAT: DCF Valuation Scenarios

Sources: New Constructs, LLC and company filings.

Each of these scenarios also assumes Shopify is able to grow revenue, NOPAT, and free cash flow (FCF) without increasing working capital or fixed assets. This assumption is unlikely but allows us to create best-case scenarios that demonstrate how high expectations embedded in the current valuation are. For reference, Shopify’s invested capital has grown 42% compounded annually since 2016.

Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life.

This article originally published on March 7, 2022.

Disclosure: David Trainer, Kyle Guske II, and Matt Shuler receive no compensation to write about any specific stock, sector, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] Our research utilizes our Core Earnings, a more reliable measure of profits, as proven in Core Earnings: New Data & Evidence, written by professors at Harvard Business School (HBS) & MIT Sloan and published in The Journal of Financial Economics.

[2] In 2021, Shopify generated $4.6 billion in revenue from $175 billion in GMV – or $1 of revenue from every $38 of GMV.