We published an update on this Danger Zone pick on July 19, 2023. A copy of the associated report is here.

After 1Q23 earnings and another missed growth goal, we continue to see Tesla (TSLA: $185/share) as one of the most overvalued stocks in the market. Even in an optimistic future cash flow scenario, shares could trade as low as $28/share.

Tesla’s latest earnings definitively show that it is not immune to competitive challenges and will likely see lower profitability in the future. But, its valuation implies the opposite. Any investor doing due diligence needs to be aware of the disconnect between Tesla’s fundamentals and the future growth implied by its stock price, which we will quantify below. See all our reports on Tesla here.

What Happened?

Where’s the 50% Growth? The Tesla bull case has centered around the company’s growth goals, which it is failing to meet. Tesla has grown deliveries at less than the 50% year-over-year (YoY) “goal” in four straight quarters as well as for the full year 2022. If the company cannot meet its own growth goals, no matter how lofty, then the time has come for bulls to re-evaluate their growth expectations. They will likely find that even their best-case scenarios for Tesla’s future fundamentals are not good enough to justify the current stock price.

Price Cuts for a Supply Constrained Business: Bulls have long argued that Tesla is supply-constrained, as demand outstrips the available supply of vehicles. However, Tesla’s multiple price cuts, six so far in the U.S. in 2023, raise questions about this claim. A company that is supply-constrained should not have to cut prices to drive demand. Instead, Tesla’s price cuts more likely point to its lack of pricing power in the increasingly competitive affordable EV market. Going forward, we would expect Tesla’s ASP to fall as further price cuts are needed as incumbent manufacturers scale up EVs at much lower entry prices. Such price cuts will directly undermine Tesla’s ability to grow profits at anywhere close to the rate implied by its valuation.

Continued Cash Burn: Despite Tesla’s top line growth, it continues to burn massive amounts of cash. Over the past five years, Tesla has burned a cumulative $4.2 billion in free cash flow (FCF) and generated negative FCF in all but one year (2019) of its existence as a public company.

Gross Margin Decline: Tesla failed to include automotive gross margin, a widely watched metric, in its 1Q23 earnings release. Instead, we are left to analyze the company’s “GAAP gross margin”, which at 19.3% in 1Q23 fell well below expectations of 22.4% and is at the lowest level since 4Q20. We would expect Tesla’s margins to fall further as it has instituted two price cuts in April, which will impact 2Q23’s results.

What Does It Mean?

Tesla is operating in a highly competitive market, and its stock remains highly overvalued. The company is not immune to incumbents introducing EVs in masse or consumers less willing to spend on new vehicles in a slowing economy. Worse yet, competition isn’t going away, as legacy automakers have ample resources and cash flow to invest in the EV market for years to come. Tesla faces an increasingly uphill battle to secure its competitive position, which makes its current valuation look even more unrealistic.

Reverse DCF Math: Tesla Priced to Generate More Profits Than Apple

In our prior report, we showed that to justify a $200 share price, Tesla would need to sell anywhere from 12 million to upwards of 30 million vehicles in 2031, depending on average selling price (ASP) assumptions. Such production would give Tesla a projected EV market share ranging from 37% to 95% in 2031.

Below, we use our reverse discounted cash flow (DCF) model to provide more clear, mathematical evidence that Tesla’s valuation remains too high and offers unattractive risk/reward.

In order to justify its current share price, Tesla would need to:

- maintain a 13% net operating profit after tax (NOPAT) margin (equal to 2022 and 1.8x Toyota’s TTM margin),

- grow revenue by 28% compounded annually through 2031, and

- limit invested capital growth to only 14% CAGR (vs. 50% CAGR from 2012–2022) to meet capacity requirements for the next decade

In this scenario, Tesla would generate $735 billion in revenue in 2031, which is 98% of the combined revenues of Toyota (TM), Stellantis (STLA), General Motors (GM), and Ford (F) over the TTM, and 9x Tesla’s 2022 revenue.

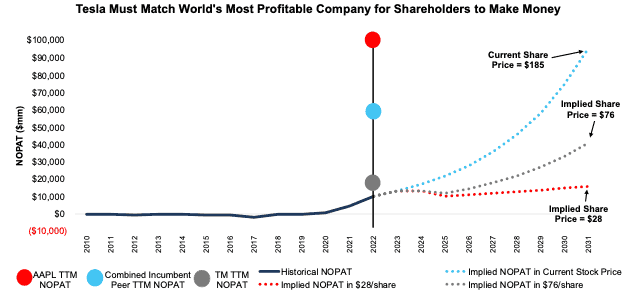

In this scenario, Tesla would earn $95.5 billion in NOPAT in 2031, which would be 1.6x the combined TTM NOPAT of Stellantis, Toyota, General Motors, Honda Motor Co. (HMC), Ford, and Nissan (NSANY) and 95% of Apple’s (AAPL) TTM NOPAT, which, at $100 billion, is the highest of all companies we cover.

TSLA Has 59% Downside Even If Units Sold Surpasses Volkswagen

If we assume Tesla sells 19% more vehicles than Volkswagen, the world’s second largest automaker, sold in 2022, Tesla still has 59%+ downside. In this scenario, Tesla would sell 9.9 million vehicles in 2031 (which implies a 31% share of the global passenger EV market in 2031), at an ASP of $50k. In this scenario we assume Tesla’s:

- NOPAT margin is 13% in 2023 and falls to 7% (equal to Toyota’s TTM margin) in 2023–2031,

- revenue grows at consensus rates in 2023 (26%), 2024 (30%), and 2025 (23%),

- revenue grows 23% a year (continuation of 2025 estimate) from 2026–2031, and

- invested capital grows at a 10% CAGR from 2023-2031, then

the stock would be worth just $76/share today – 59% downside to the current price. In this scenario, Tesla grows NOPAT to $41.1 billion, or 4x its 2022 NOPAT and 2.3x Toyota’s TTM NOPAT.

TSLA Has 85%+ Downside Even If Units Sold Grows 3.5x

If we estimate more reasonable (but still very optimistic) growth achievements for Tesla, the stock is worth just $28/share. Here’s the math, assuming Tesla’s:

- NOPAT margin is 13% in 2023 and falls to 7% (equal to Toyota’s TTM margin) in 2023–2031,

- revenue grows at consensus rates in 2023 (26%), 2024 (30%),

- revenue grows 8% a year from 2025–2031, and

- invested capital grows at a 6% CAGR from 2023-2031, then

the stock would be worth just $28/share today – an 85% downside to the current price.

In this scenario, Tesla sells 4.8 million cars (15% of the global passenger EV market in 2031) in 2031 at an ASP of $40k. Given the required expansion of plant/manufacturing capabilities and formidable competition, we think Tesla will be lucky to sustain a margin as high as 7% from 2023-2031. If Tesla fails to meet these expectations, then the stock is worth less than $28/share.

Figure 1 compares the firm’s historical NOPAT to the NOPAT implied in the above scenarios to illustrate just how high the expectations baked into Tesla’s stock price remain. For additional context, we show Apple’s, Toyota’s, and the combined incumbent peers’[1] TTM NOPAT.

Figure 1: Tesla’s Historical and Implied NOPAT: DCF Valuation Scenarios

Sources: New Constructs, LLC and company filings

Each of the above scenarios assumes Tesla’s invested capital grows between 6-14% compounded annually through 2031 as it increases production capacity to meet the implied vehicle sales in each scenario. This assumption is highly conservative, as Tesla’s invested capital has grown much faster in the past. For reference, Tesla’s invested capital grew 50% compounded annually from 2012-2022. Additionally, Tesla’s property, plant, and equipment line item has grown 46% compounded annually since 2012.

In other words, we aim to provide inarguably best-case scenarios for assessing the expectations for future market share and profits reflected in Tesla’s stock market valuation. Even doing so, we find that Tesla is significantly overvalued.

This article was originally published on April 19, 2023.

Disclosure: David Trainer, Kyle Guske II, and Italo Mendonça receive no compensation to write about any specific stock, sector, style, or theme.

Questions on this report or others? Join our Society of Intelligent Investors and connect with us directly.

[1] Combined incumbent peers’ NOPAT includes Stellantis, Toyota, General Motors, Honda Motor, Ford, and Nissan.