The quarterly earnings releases promoted by companies cannot be used to reliably measure economic earnings or return on invested capital (ROIC). These releases are unaudited and don’t contain the footnotes and Management Discussion & Analysis (MD&A) section needed to reverse accounting distortions. Footnotes and the MD&A are only found in 10-Ks.

In the six weeks from mid-February through the end of March, our robo-analyst technology read through 2,139 10-K (or international equivalent) filings and collected 49,862 data points. Our analyst team used this data to make 49,862 adjustments with a dollar value of $16.1 trillion. That breaks down into:

- 21,094 income statement adjustments with a total value of $1.1 trillion

- 20,500 balance sheet adjustments with a total value of $6.9 trillion

- 8,268 valuation adjustments with a total value of $8.1 trillion

During 10-K filing season, we updated our readers on a number of big name tickers:

- We highlighted several new red flags in Valeant Pharmaceuticals (VRX) 10-K.

- We showed how Home Depot’s (HD) ROIC calculation could be misleading.

- Comparisons between this year’s filing and last year’s showed that Royal Dutch Shell (RDS.A) has declining cash flows despite its rising EPS.

- Removing hidden non-operating expenses found in the footnotes led us to upgrade Cigna (CI) to Attractive.

On Twitter, we pointed out red flags found in the footnotes or MD&A such as pricey corporate perks and changes in pension plan assumptions under the hashtag #filingseasonfinds.

A Fiduciary Level of Diligence

Our technology enables us to deliver fundamental diligence at a previously impossible scale. As we wrote in “Diligence Will Matter More Than Ever In 2017,” investors are going to increasingly demand this level of diligence as a baseline level of research to support any advice.

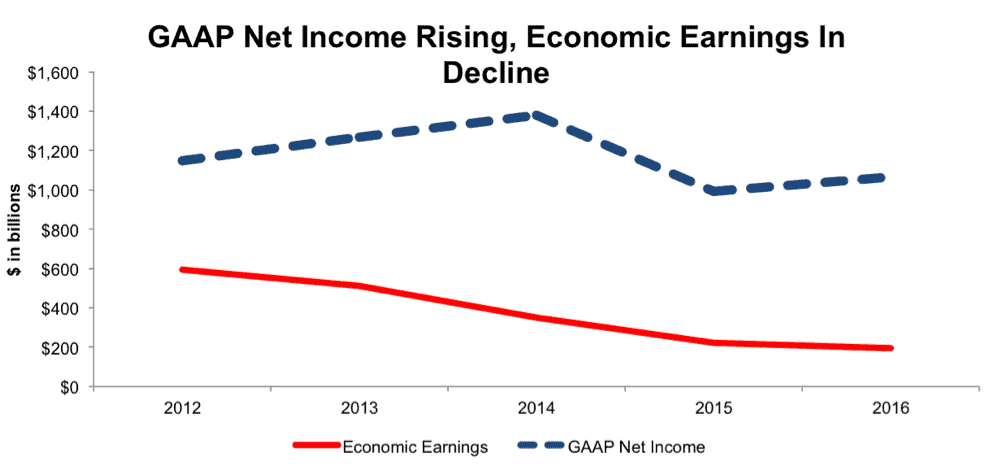

Figure 1: GAAP Net Income Vs. Economic Earnings For The Broader Market

Sources: New Constructs, LLC and company filings.

Figure 1 shows just how big a difference diligence can make. Many analysts have touted the end of the “earnings recession,” but our data tells a different story. For the 2,600+ companies for which we have comparable data going back over 5 years, economic earnings – a measure of companies’ excess return on invested capital over their cost of capital – continue to decline.

Not only will investors increasingly demand this level of diligence, soon it may be required by law. Even if the fiduciary rule does not become law, advisors will likely have to fulfill the duty of care, which requires real diligence behind any investment recommendations, to remain competitive. How can anyone claim to fulfill their duty of care without reading through the footnotes and MD&A to reverse accounting distortions?

One Company To Watch In 2017

Even though filing season has ended, we still have 10-Ks coming in throughout the rest of the year. On April 4, our robo-analyst read through the 10-K for Wal-Mart Stores (WMT). Using this data, analyst Eric Roll made several significant adjustments based on items buried in the footnotes.

On the NOPAT side, we found three hidden non-operating items related to the sales of discontinued operations on page 10. Together, these three items artificially added $359 million to Wal-Mart’s pre-tax income.

On the invested capital side, Wal-Mart disclosed its accumulated other comprehensive loss on page 40. We added back the $14.2 billion in other comprehensive loss back to invested capital so that we hold Wal-Mart’s management accountable for all of the capital invested in its business.

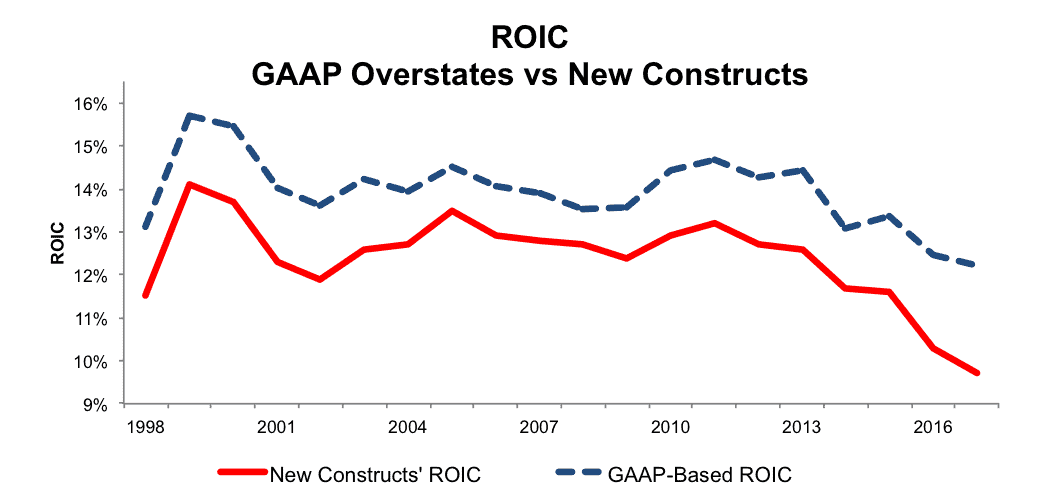

These adjustments reveal a troubling trend for Wal-Mart. Figure 2 shows that the retail giant’s ROIC has fallen for six consecutive years. For comparison, an ROIC calculation that ignores items in the footnotes (what we call “GAAP-Based ROIC”) understates the steadiness and the severity of the decline in recent years.

Figure 2: Wal-Mart’s ROIC Declines To Lowest Level in Past 20 Years

Sources: New Constructs, LLC and company filings.

Wal-Mart’s 9.7% ROIC in 2017 was its worst in the past 20 years, and it represents the only year below double digits in that timeframe. The stock is still cheaply valued, but Wal-Mart’s declining profitability is big part of why we believe Target (TGT) is a better pick in the retail sector.

It’s no secret that Wal-Mart’s profitability has declined in recent years, but our research reveals just how long and deep that decline has been.

This article originally published on April 19, 2017.

Disclosure: David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.