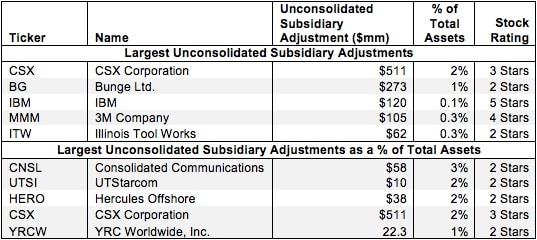

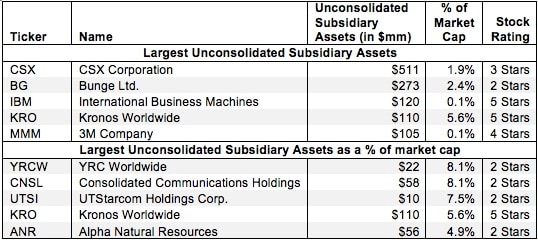

Unconsolidated Subsidiary Assets – Valuation Adjustment

Investors who ignore unconsolidated subsidiary assets are not getting a true picture of the cash available to be returned to shareholders. By adding unconsolidated subsidiary assets one can better understand the value of the stock to shareholders. Diligence pays.