We published an update on PTON on May 15, 2023. A copy of the associated update report is here.

Time is running out for cash-burning companies kept afloat with easy/cheap access to capital. These “zombie” companies are at risk of going bankrupt if they cannot raise more debt or equity, which is not as easy as it used to be.

As the Fed raises interest rates and ends quantitative easing, access to cheap capital is drying up quickly. At the same time, many companies face declining margins and may be forced to default on interest payments without the possibility of refinancing. As these zombie companies run out of the cash needed to stay afloat, risk premiums will rise across the market, which could further squeeze liquidity and create an escalating series of corporate defaults.

This report features Peloton (PTON: $11/share), a zombie company with a high risk of seeing its stock go to $0/share. We also feature Freshpet (FRPT: $55/share) here and Carvana (CVNA: $25/share) here.

Zombie Companies with Little Cash Are Risky

Companies with heavy cash burn and little cash on hand are risky in today’s market. Being forced to raise capital in this environment, even if the company is ultimately successful, is not good for existing shareholders.

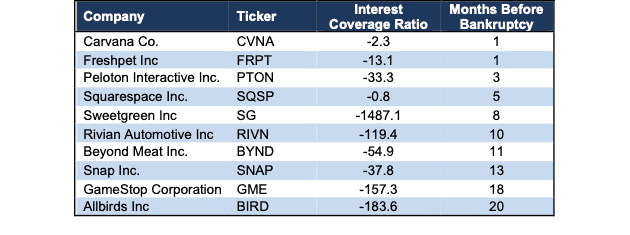

Figure 1 shows the zombie companies most likely to run out of cash first, based on free cash flow (FCF) burn and cash on the balance sheet over the trailing-twelve-months (TTM). Each company in Figure 1 has:

- Negative interest coverage ratio (EBIT/Interest expense)

- Negative FCF over the TTM

- Less than 24 months before it needs more capital to subsidize the TTM FCF burn rate

- Been a Danger Zone pick

Not surprisingly, the companies that are most at risk of seeing their stock price go to $0 are the ones with a poor underlying business model, which was overlooked by investors during the 2020-2021 meme stock-driven market frenzy. Companies such as Carvana, Freshpet, Peloton, and Squarespace (SQSP) have less than six months of cash on their balance sheets based on their FCF burn over the past twelve months. These stocks have a real risk of going to zero.

Figure 1: Danger Zone Stocks with Less than Two Year’s Worth of Cash on Hand: as of 1Q22

Sources: New Constructs, LLC and company filings.

To calculate “Months Before Bankruptcy” we divided the TTM FCF burn by 12, which equals monthly cash burn. We then divide Cash and Equivalents on the balance sheet through 1Q22 by monthly cash burn.

And Overvalued Zombie Stocks Are the Riskiest

Stock valuations that embed high expectations for future profit growth add more risk to owning shares of zombie companies with just a few months’ worth of cash left. For the riskiest zombie companies, not only does the stock price not reflect the short-term distress facing the company, but it also reflects unrealistically optimistic assumptions about the long-term profitability of the company. With these stocks, overvaluation risk is stacked on top of short-term cash flow risk.

Below, we’ll take a closer look at Peloton and detail the company’s cash burn and how much further its stock price could fall.

Peloton Interactive (PTON: $11/share)

We put Peloton (PTON) in the Danger Zone in September 2019, prior to its IPO and have reiterated our negative opinion on the stock many times since. Since our original report, the stock has outperformed the S&P 500 as a short by 91%. Even after falling 92% from its 52-week high, 73% YTD, and 74% since our most recent report in February 2022, we think the stock has much more downside.

Peloton’s issues are well telegraphed – given the stock’s decline over the past year – but investors may not realize that the company only has a few months worth of cash remaining to fund its operations.

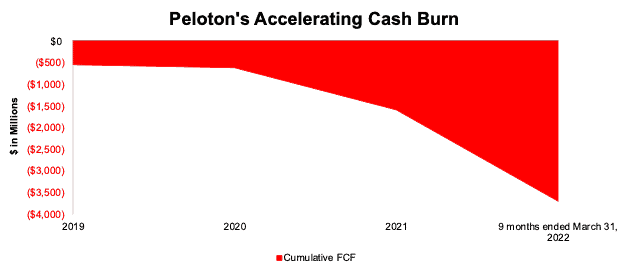

Despite rapid top-line growth, particularly in 2020 and 2021, Peloton’s free cash flow (FCF) has been negative every year since fiscal 2019. Since then, Peloton has burned through $3.7 billion in FCF, per Figure 2.

Peloton burned through $3.3 billion in FCF over the TTM ended fiscal 3Q22. With just $879 million in cash and cash equivalents on the balance sheet at the end of fiscal 3Q22, Peloton’s cash balance could keep the company afloat for just over three months from the end of its fiscal 3Q22.

Similar to the situations above, Peloton raised $750 million in a five-year term loan in May 2022 to help shore up its balance sheet. The debt is extremely creditor friendly, as it bears an interest rate of 6.5 percentage points above the Secured Overnight Financing Rate (currently equal to 1.45%) and will increase by 50 basis points if Peloton chooses not to get the debt rated by one of the major credit rating agencies. Additionally, the debt is structured to make it more expensive for Peloton to repay during the first two years. This new cash can keep the company afloat for three month’s, based on TTM cash burn rates.

If we assume the average FCF burn over the past two years, and include the additional capital raised a month ago, Peloton only has 11 months left of cash before needing to raise more capital or go out of business.

Figure 2: Peloton’s Cumulative Free Cash Flow Through Fiscal 3Q22

Sources: New Constructs, LLC and company filings

Annual dates represent fiscal year. Peloton’s fiscal year ends June 30 of each calendar year.

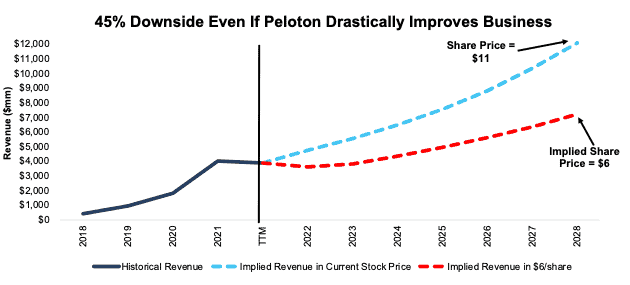

Reverse DCF Math: Peloton Is Priced to Triple Sales Despite Weakening Demand

Below we use our reverse discounted cash flow (DCF) model to analyze the future cash flow expectations baked into Peloton’s stock price. We also provide an additional scenario to highlight the downside potential in shares if Peloton’s revenue grows at more reasonable rates.

If we assume Peloton’s:

- NOPAT margin immediately improves to 1.7% (Peloton’s best-ever margin, compared to -30% over the TTM) and

- revenue grows 16% compounded annually through 2028, then

the stock would be worth $11/share today – equal to the current stock price.

In this scenario, Peloton would generate $12.1 billion in revenue in fiscal 2028, which is over 3x its TTM revenue and 7x its fiscal 2020 revenue. At $12.4 billion, Peloton’s revenue would imply a 17% share of its total addressable market (TAM) in calendar 2027, which we consider the combined online/virtual fitness and at-home fitness equipment markets. For reference, Peloton’s share of its TAM in calendar 2020, or before the major pandemic boost, was just 13%. Of competitors with publicly available sales data, iFit Health, owner of NordicTrack and ProForm, Beachbody (BODY), and Nautilus (NLS) held, respectively, 9%, 6%, and 4% of the TAM in 2020.

We think it is overly optimistic to assume Peloton will vastly increase its market share given the current market landscape, supply chain issues, and significant price and subscription changes, while also achieving its highest ever margins. In a more realistic scenario, detailed below, the stock has large downside risk.

PTON Has 45%+ Downside if Consensus Is Right

We perform a second DCF scenario to highlight the downside risk to owning Peloton should it grow at consensus revenue estimates. If we assume Peloton’s:

- NOPAT margin improves to 1.7%,

- revenue grows at consensus rates in 2022, 2023, and 2024, and

- revenue grows 14% a year in 2025-2028 (continuation of consensus from 2024), then

the stock would be worth just $6/share today – a 45% downside to the current price. This scenario still implies Peloton’s revenue grows to $7.2 billion in fiscal 2028, which would imply a 10% share of its total addressable market in 2028.

If Peloton fails to achieve the revenue growth or margin improvement we assume for this scenario, the downside risk in the stock would be even higher, putting the stock at risk of declining to $0 per share.

Figure 3 compares Peloton’s historical revenue to the revenue implied by each of the above DCF scenarios.

Figure 3: Peloton’s Historical and Implied Revenue: DCF Valuation Scenarios

Sources: New Constructs, LLC and company filings.

Dates represent Peloton’s fiscal year, which runs through June of each year

Each of the above scenarios also assumes Peloton grows revenue, NOPAT, and FCF without increasing working capital or fixed assets. This assumption is highly unlikely but allows us to create best-case scenarios that demonstrate the expectations embedded in the current valuation. For reference, Peloton’s TTM invested capital is five times its fiscal 2018 level. If we assume Peloton’s invested capital increases at a similar historical rate in DCF scenarios 2 above, the downside risk is even larger.

This article originally published on June 23, 2022.

Disclosure: David Trainer, Kyle Guske II, and Matt Shuler receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.