Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life and Marketwatch.com

At the end of the day, the goal of a business is not to grow revenue, but profits. The purpose of capital markets is to reward those companies that derive the greatest profits from the capital trusted with them, i.e. return on their invested capital (ROIC). So what happens when a company focuses on top-line growth, ignores cash flows or economic earnings, and generates a low ROIC? That company, Mobile Mini (MINI: $30/share), goes in the Danger Zone this week.

Acquisitions Boost Revenue While Killing Profits and Diluting Investors

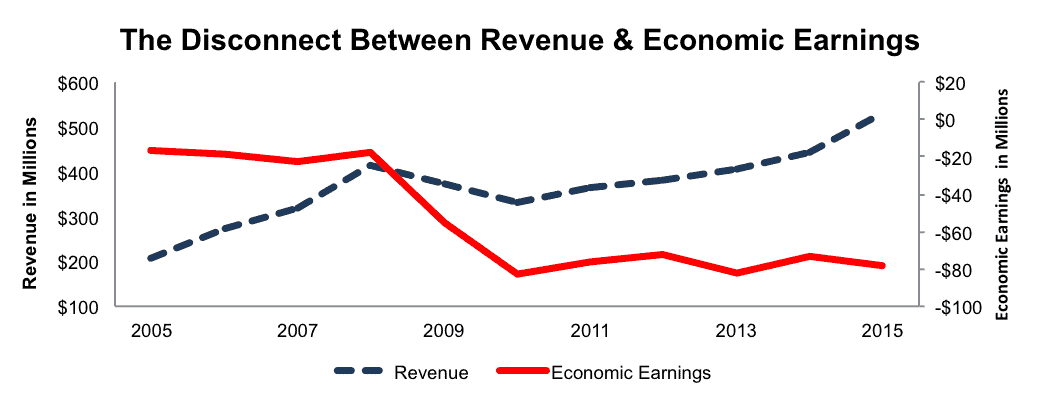

Mobile Mini has built its business by acquiring smaller storage providers to quickly improve the company’s customer base, leasable storage units, and revenue. Since 2005, Mobile Mini’s revenue has grown by 10% compounded annually while the company’s economic earnings, the true cash flows of business, have declined from -$16 million in 2005 to -$78 million in 2015. Per Figure 1, the acquisitions to grow revenue were done with little care to the economic repercussions. See the reconciliation of Mobile Mini’s GAAP net income to economic earnings here.

Figure 1: Revenue Grows Inverse To Economic Earnings

Sources: New Constructs, LLC and company filings

Sources: New Constructs, LLC and company filings

Aside from negative economic earnings, Mobile Mini’s return on invested capital (ROIC) has fallen from 7% in 2005 to a bottom quintile 4% over the last twelve months.

Acquisitions Diluted Shareholder Value

Compounding the issues, MINI has significantly grown the balance sheet and diluted shareholders over this time frame. From 2005 to 2015, MINI’s debt grew over 11% compounded annually to $964 million (71% of market cap). Over the same time, the company’s invested capital, or the sum of all cash invested into a company, grew by 12% compounded annually, to $2.1 billion in 2015. Essentially, MINI funded its acquisition-based growth at the expense of shareholders, while generating no profits.

Misaligned Executive Compensation Drives Shareholder Destructive Strategic Decisions

In 2016, the targets for short-term bonuses, which represent nearly 30% of executive pay, are rental revenue and adjusted EBITDA. Both of these metrics are easily grown by acquiring other storage providers with no accountability for the cost of that growth.

Long-term incentives, which account for over 40% of executive pay, are linked to stock grants, half of which vest based on return on capital employed (ROCE) targets and the other half vest over time. We would normally commend a compensation committee for using a metric based on some measure of return on capital, but not in this case. Mobile Mini’s ROCE metric begins with the non-GAAP metric “adjusted compensation EBITDA”, which removes the effect of acquisitions, “certain non-cash expenses” and “transactions that the Committee believes are not indicative of our ongoing business.” With such leeway in the calculation of “adjusted compensation EBITDA,” and therefore ROCE, the metric has no teeth and we cannot be sure executives will curtail the destructive acquisitions that occurred in the past. At this time, executives can still earn large bonuses without focusing on shareholder value creation.

Non-GAAP Earnings Don’t Pay Real Expenses

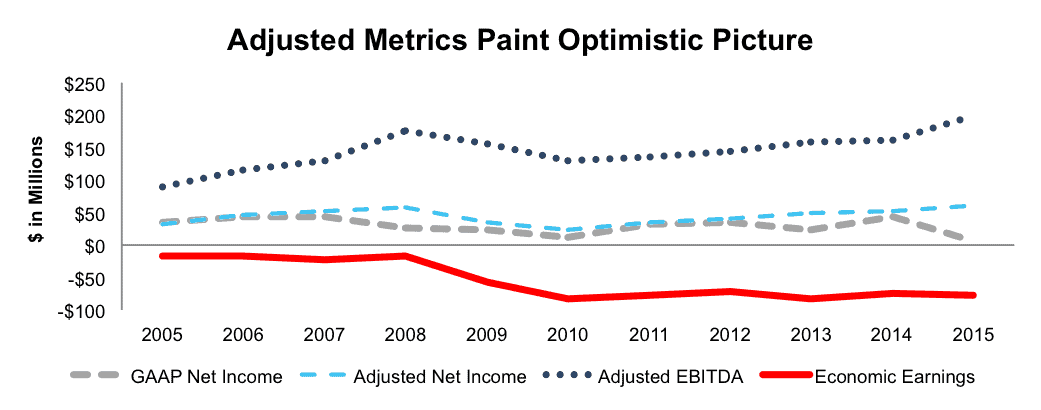

Investors following trends in MINI’s “adjusted EBITDA” may be shocked to learn that the company is in worse economic shape than Mobile Mini’s management would have you believe. When looking through the “adjusted” noise, the underlying economics of the business reveal a much worse situation per Figure 1. Here are the expenses MINI removes to calculate its non-GAAP metrics, including adjusted EBITDA and adjusted net income:

- Restructuring expense

- Acquisition-related expense

- Transition services

- Unclaimed property settlements

- Deferred financing cost write-offs

- Share based compensation expense

By removing these costs, Mini creates a highly misleading picture of its business, not “a better representation of business.” Since 2005, Mobile Mini’s adjusted net income has grown from $33 million to $60 million in 2015, or 6% compounded annually. More misleading, adjusted EBITDA has grown from $89 million in 2005 to $201 million in 2015, or 8% compounded annually. Meanwhile, economic earnings have declined from -$16 million in 2005 to -$78 million in 2015. Figure 2 highlights the discrepancies between GAAP net income, adjusted net income, adjusted EBITDA, and economic earnings over the past decade.

Figure 2: MINI’s Non-GAAP Disconnect With Reality

Sources: New Constructs, LLC and company filings

Sources: New Constructs, LLC and company filings

Low Profitability Puts MINI At A Disadvantage

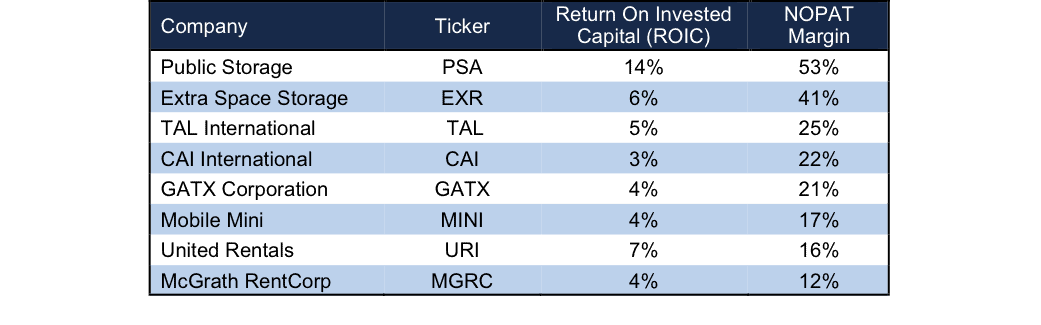

Mobile Mini operates largely in the portable storage industry, which represented 80% of revenue in 2015. The storage industry is highly competitive, and MINI faces competition from fixed self storage facilities, such as Public Storage (PSA) and Extra Space Storage (EXR). At the same time, MINI faces competition from many private and/or captive companies, including Algeco Scotsman, PODS, Pac-Van, 1-800-PACK-RAT, Haulaway Storage Containers and ModSpace. Most of the peers MINI lists in its 2015 10-K have an equal or higher ROIC and NOPAT margin. A lower ROIC and NOPAT margin mean lower pricing flexibility, a concern management has voiced: “To the extent that we choose to match our competitors’ declining prices, it could harm our results of operations as we would have lower margins”. Figure 3 has the details.

Figure 3: MINI’s Profitability Is Middle of Road Amongst Peer Group

Sources: New Constructs, LLC and company filings

Sources: New Constructs, LLC and company filings

Bull Hopes On Thin Ice, One Risk To Bear Case

Bulls of Mobile Mini will point to the company’s growing revenue as a sign that the company is doing something right. And, as acquisition costs and restructurings slow down, the company would become highly profitable. As we’ve shown above, these hopes ignore the shareholder destruction of Mobile Mini over the past few years.

Not only have Mini’s acquisitions equated to negative economic earnings, as seen in Figure 1, Mobile Mini’s other attempts at increasing revenue have failed to manifest in improvements to the bottom line. First, in each of the past 13 quarters, Mobile Mini has highlighted an increase in rental rates, signaling that revenue growth can be attributed to price increases. These price increases have done little in terms of boosting margins or profit. On the contrary, Mobile Mini’s NOPAT margin has declined from 18% in 2013 to 17% in 2015, despite increasing prices in each quarter during this time period. As noted above, MINI is aware that competitors are lowering prices while they are raising them. Without a large differentiator to MINI’s service, we doubt MINI can continue these price increases.

Second, bulls will point to Mobile Mini’s expansion into the Specialty Containment industry, with the acquisition of Evergreen Tank Solutions, as a new avenue for profit growth. The flaw in this argument appears when you look at the margin of these segments, especially in the most recent quarter, 1Q16. In this quarter, the Specialty Containment segment had an operating margin of only 6%, while Mini’s Portable Storage segment had an operating margin of 25%. Just as we’ve noted in the case of Netflix, expanding into regions or industries with lower margins, while growing revenue, will not create the profits implied by exuberant optimism embedded in the current stock price.

A third hope for bulls is industry consolidation leading to greater pricing flexibility. An industry leader could stand to raise prices, but only if that firm controlled a large supply of portable storage units and the industry was facing greater demand than supply. It does not appear the portable storage industry is supply constrained, particularly in regards to Mobile Mini. In 2015, Mobile Mini reported a 69% average portable fleet utilization rate. As long as the industry remains fragmented and supply is plentiful, the bulls’ hopes for sustained higher pricing are difficult to believe in given the undifferentiated nature of MINI’s storage offerings.

The biggest risk to our thesis is that Mobile Mini gets acquired at a value well above today’s price by a larger competitor or company looking to enter the storage business. As we’ll show below, any acquisition at current prices, and especially higher, would be ill-advised, and the acquirer would be greatly overpaying.

Acquisition Hopes Don’t Justify Valuation

Could MINI be an attractive acquisition target at current prices? We think not, and to begin with, MINI has hidden liabilities that make it more expensive than the accounting numbers suggest.

- $226 million in deferred tax liability (17% of market cap)

- $52 million in off-balance-sheet operating leases (4% of market cap)

- $14 million in outstanding employee stock options (1% of market cap)

After adjusting for these hidden liabilities (which add up to 22% of market cap), we can model multiple purchase price scenarios. Unfortunately for investors, only in the best of scenarios does MINI warrant a takeover at a price higher than today’s price.

To highlight how overvalued MINI is, Figures 4 and 5 show what we think United Rentals (URI) should pay for MINI to ensure the deal is truly accretive to URI’s shareholder value. Each implied price is based on a ‘goal ROIC’ assuming different levels of revenue growth. We chose to assess the economic value of MINI after 5 years at three different levels of revenue growth: 12%, 14% and 16%. These levels are higher than the 10% compounded annual growth rate achieved over the last 10 years. We believe in increase in revenue is a reasonable expectation given the cross selling opportunities for United Rentals, which leases construction equipment and tools that also need to be stored.

The bottom line is that there are limits on how much URI should pay for MINI to earn a proper return, given the NOPAT or cash flows being acquired. For each of the scenarios, we assume MINI achieves its current 17% NOPAT margin.

Figure 4: Implied Acquisition Prices For URI To Achieve 7% ROIC

Sources: New Constructs, LLC and company filings.

The first “goal ROIC” is URI’s weighted average cost of capital (WACC) or 7%. Figure 4 shows the prices URI should pay for MINI assuming different levels of revenue growth achieved post acquisition. Only if MINI can continue growing revenue at 16% each year for the next five years is the firm worth more than its current share price of $30/share. We include this scenario to provide a “best-case” view. Regardless, any deal that only achieves a 6% ROIC would be value neutral, as the return on the deal would equal URI’s WACC.

Figure 5: Implied Acquisition Prices For URI To Achieve 9% ROIC

Sources: New Constructs, LLC and company filings.

Figure 5 shows the next “goal ROIC” of 9%, which is an improvement from URI’s current ROIC of 7%. This deal would be truly accretive to shareholders as it would improve URI’s ROIC. In the best case growth scenario, the most URI should pay for MINI is $20/share (33% downside).

Without A Takeover, Organic Growth Expectations Are Unrealistic

Barring acquisition, to justify its current stock price ($30/share), MINI must grow NOPAT by 15% compounded annually for 12 years. In a more realistic scenario, given that MINI focuses on organic growth and ditches acquisitions, we assume that MINI can grow NOPAT by 9% compounded annually for the next decade, the stock is worth only $10/share today – a 66% downside.

Catalyst: Earnings Miss Will Sink Shares

Despite the struggles noted above, MINI is up nearly 41% over the past five years and has slightly outperformed the Russell 2000 year-to-date. However, the signs of trouble began to reveal themselves in Mobile Mini’s 1Q16 earnings release. In that release, MINI reported revenue was down 6% year-over-year, after year-over-year revenue growth dating back to 3Q13. We believe this revenue miss may be more a sign of things to come, rather than an outlier. With the company exhausting price increases while facing pricing competition, it seems profits and revenue will get harder and harder to grow. At the same time, growth through acquisition has not been truly profitable, and the strategy added a business segment that as of 1Q16, had worse margins than MINI’s existing business. When the momentum stops, particularly in stocks that tout revenue growth at the expense of profits or ROIC, the results can be damaging for those investors still holding the stock. Just ask investors in previous momentum-driven stocks that we put in the Danger Zone. Twitter (TWTR), El Pollo Loco (LOCO), and SolarCity (SCTY) are all down over 50% since going in the Danger Zone.

Insider Sales Rather Low But Short Interest Is High

Over the past 12 months 145 thousand shares have been purchased and 37 thousand have been sold for a net effect of 108 thousand insider shares purchased. These purchases represent <1% of shares outstanding. Additionally, there are 3.7 million shares sold short, or just over 8% of shares outstanding.

Impact of Footnotes Adjustments and Forensic Accounting

In order to derive the true recurring cash flows, an accurate invested capital, and a real shareholder value, we made the following adjustments to Mobile Mini’s 2015 10-K:

Income Statement: we made $175 million of adjustments with a net effect of removing $83 million in non-operating expenses (16% of revenue). We removed $129 million related to non-operating expenses and $46 million related to non-operating income. See all adjustments made to MINI’s income statement here.

Balance Sheet: we made $252 million of adjustments to calculate invested capital with a net increase of $233 million. The most notable adjustment was $108 million (6% of net assets) related to asset write-downs. See all adjustments to MINI’s balance sheet here.

Valuation: we made $1.2 billion of adjustments with a net effect of decreasing shareholder value by $1.2 billion. There were no adjustments that increased shareholder value. One of the largest adjustments was the removal of $226 million (17% of market cap) due to deferred tax liabilities.

Dangerous Funds That Hold MINI

The following funds receive our Dangerous-or-worse rating and allocate significantly to Mobile Mini.

- Broadview Opportunity Fund (BVAOX) – 2.2% allocation and Dangerous rating.

- CRM Small Cap Value Fund (CRISX) – 1.7% allocation and Very Dangerous rating.

This article originally published here on May 23, 2016

Disclosure: David Trainer and Kyle Guske II receive no compensation to write about any specific stock, style, or theme.

Click here to download a PDF of this report.

Photo Credit: smussyolay (Flickr)