Six new stocks make March’s Exec Comp Aligned with ROIC Model Portfolio, available to members as of March 15, 2023.

Recap from February Picks

Our Exec Comp Aligned with ROIC Model Portfolio (-8.7%) underperformed the S&P 500 (-5.6%) from February 16, 2023 through March 13, 2023. The best performing stock in the portfolio was down 3%. Overall, six out of the 15 Exec Comp Aligned with ROIC Stocks outperformed the S&P from February 16, 2023 through March 13, 2023.

This report leverages our cutting-edge Robo-Analyst technology to deliver proven-superior[1] fundamental research and support more cost-effective fulfillment of the fiduciary duty of care.

This Model Portfolio includes stocks that earn an Attractive or Very Attractive rating and align executive compensation with improving ROIC. This combination provides a unique list of long ideas as the primary driver of shareholder value creation is return on invested capital (ROIC).

New Stock Feature for March: Robert Half International (RHI: $75/share)

Robert Half International (RHI) is the featured stock in March’s Exec Comp Aligned with ROIC Model Portfolio.

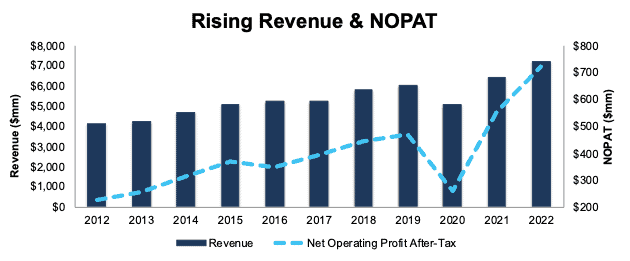

Robert Half has grown revenue and NOPAT by 6% and 12% compounded annually, respectively, since 2012. The company’s NOPAT margin improved from 6% in 2012 to 10% in 2022, while invested capital turns rose from 4.2 to 4.9 over the same time. Rising NOPAT margins and invested capital turns drive the company’s return on invested capital (ROIC) from 23% in 2012 to 49% in 2022.

Figure 1: Robert Half’s Revenue & NOPAT: 2012 – 2022

Sources: New Constructs, LLC and company filings

Executive Compensation Properly Aligns Incentives

Robert Half’s executive compensation plan aligns the interests of executives and shareholders by tying the payout of performance shares to “three-year ROIC”, according to the company’s proxy statement.

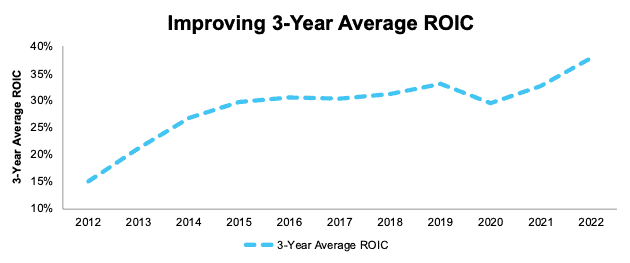

The company’s inclusion of “three-year ROIC” as a performance goal has helped create shareholder value through rising ROIC and economic earnings. When we calculate three-year average ROIC using our superior fundamental data, we find that Robert Half’s three-year average ROIC has increased from 15% in 2012 to 38% in 2022. Economic earnings rose from $176 million to $613 million over the same time.

Figure 2: Robert Half International’s ROIC: 2012 – 2022

Sources: New Constructs, LLC and company filings

RHI Has Further Upside

At the current price of $75/share, RHI has a price-to-economic book value (PEBV) ratio of 0.9. This ratio implies the market expects Robert Half’s NOPAT to permanently fall by 10%. This expectation seems overly pessimistic for a company that has grown NOPAT 12% compounded annually over the past decade and 9% compounded annually over the past two decades.

If Robert Half’s NOPAT margin falls to 8% (5-year average vs. 10% in 2022) and the company grows revenue by 5% compounded annually over the next decade, the stock would be worth $92/share today – a 23% upside. See the math behind this reverse DCF scenario. In this scenario, Robert Half’s NOPAT would grow just 2% compounded annually over the next decade.

For reference, Robert Half has grown revenue by 6% compounded annually over the past decade and NOPAT by 12% compounded annually over the same time. Should the company grow NOPAT more in line with historical growth rates, the stock has even more upside.

Critical Details Found in Financial Filings by Our Robo-Analyst Technology

Below are specifics on the adjustments we made based on Robo-Analyst findings in Robert Half’s 10-K:

Income Statement: we made $125 million in adjustments with a net effect of removing $67 million in non-operating expenses (1% of revenue). Clients can see all adjustments made to Robert Half’s income statement on the GAAP Reconciliation tab on the Ratings page on our website.

Balance Sheet: we made $1.5 billion in adjustments to calculate invested capital with a net decrease of $439 million. One of the largest adjustments was $907 million (52% of reported net assets) in adjustments for deferred compensation. Clients can see all adjustments made to Robert Half’s balance sheet on the GAAP Reconciliation tab on the Ratings page on our website.

Valuation: we made $566 million in adjustments, with a net effect of increasing shareholder value by $27 million. The most notable adjustment to shareholder value was $297 million in excess cash. This adjustment represents 4% of Robert Half’s market cap. Clients can see all adjustments to Robert Half’s valuation on the GAAP Reconciliation tab on the Ratings page on our website.

This article was originally published on March 24, 2023.

Disclosure: David Trainer, Kyle Guske II, and Italo Mendonça receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] Our research utilizes our Core Earnings, a more reliable measure of profits, as proven in Core Earnings: New Data & Evidence, written by professors at Harvard Business School (HBS) & MIT Sloan and published in The Journal of Financial Economics.