We published an update on SG on February 7, 2022. A copy of the associated update report is here.

Sweetgreen (SG: $24/share midpoint of IPO price range) is expected to go public on November 18, 2021 with a midpoint valuation of $24/share, which would earn the stock our Unattractive rating.

We do not think investors should expect to make any money in Sweetgreen stock if the expected valuation comes true. A $24/share valuation implies Sweetgreen’s revenue will grow 8x 2020 levels and faster than Chipotle in its first 10 years after going public.

We think the stock is likely worth $0 given the company’s limited differentiation and the intense competition from other new entrants and established restaurants, which are easily replicating Sweetgreen’s menu and concept.

Despite its large online presence, Sweetgreen lost market share in 2020 to stronger, better-positioned competitors. Sweetgreen’s locally-sourced supply chain adds safety risks and hurts the company’s ability to achieve the economies of scale that more vertically integrated restaurants enjoy.

The company has never achieved profits in any fiscal period since it began operations, and we see little to no path to profitability in the future.

Our IPO research aims to provide investors with more reliable fundamental research.

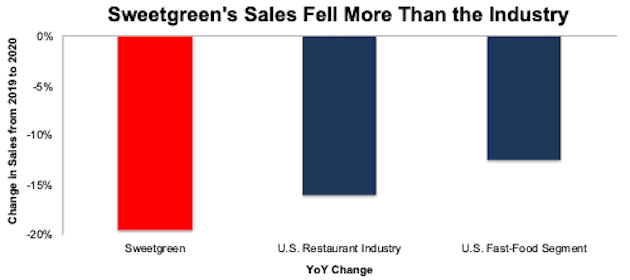

Sweetgreen’s Big Miss In 2020

More than 10% of U.S. restaurants closed in 2020, and the survivors took their market share. In particular, quick-service restaurants (QSR) fared better than the overall industry. While U.S. restaurant sales fell 16% year-over-year in 2020, QSR sales fell just 12%.

With consumers turning to quick service and online options, 2020 was an opportune time for Sweetgreen, which generated half of its 2019 revenue from online sales, to gain market share. Instead, Sweetgreen’s share of the fast-food and overall restaurant market fell as its revenue declined 20% YoY, more than the market, in 2020, per Figure 1.

Figure 1: Sweetgreen Vs. U.S. Restaurant Industry & Fast-Food Segment: 2020 YoY Change in Sales

Sources: New Constructs, LLC, company filings, FRED, and Statista

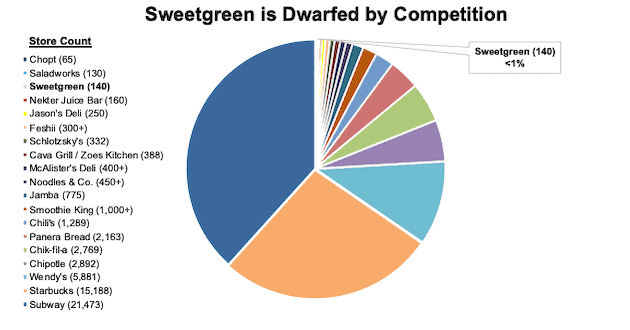

Fresh Fast Food Isn’t a Fresh Concept

Sweetgreen isn’t the first restaurant to offer consumers “real food”. Subway’s “Eat Fresh” concept helped the company grow to more than 21,000 stores in the U.S. today. For decades, Chipotle has marketed its “Food With Integrity” concept and grown to 2,892 stores as of 3Q21. Meanwhile, the market is filled with incumbents who offer fresh and healthy meals and other health-conscious new entrants, per Figure 2. With just 140 store locations, Sweetgreen is a minor player in a very fragmented, large, and competitive market.

Figure 2: Sweetgreen’s Store Count Vs. Competitors[1]

Sources: New Constructs, LLC and company filings

Online Ordering Is Not Fresh Either

Sweetgreen’s high-priced menu means that it competes not just with other fast-food and fast-casual restaurants, but also with traditional restaurants that offer similarly priced salad and bowl options. Many of these restaurants improved their online sales channels and improved take-out operations during 2020.

As a whole, the U.S. restaurant online orders from March 2020 to March 2021 rose 124%. More sophisticated online operations are eating away at what was once was a technological advantage for Sweetgreen.

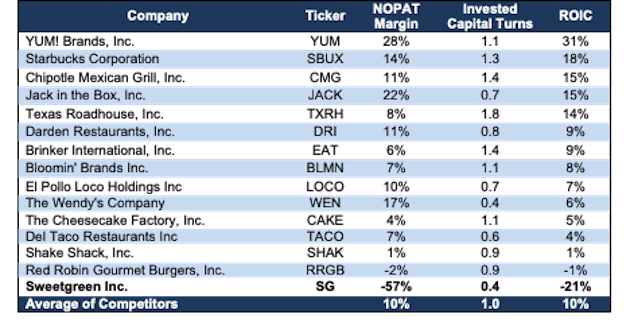

Not Surprisingly, Sweetgreen Ranks Last Among Peers

Given Sweetgreen’s inefficient supply chain (more below) and the intense competition that it faces, it comes as no surprise that the company’s fundamentals are much worse than its peers. Peers include traditional, fast-food and fast-casual restaurants.

Compared to its peer group, Sweetgreen’s net operating profit after-tax (NOPAT) margin of -57% is last, its invested capital turns of 0.4 is second to last, and its return on invested capital (ROIC) of -21% ranks last. See Figure 3.

Figure 3: Sweetgreen’s Profitability Vs. Competitors: TTM

Sources: New Constructs, LLC and company filings

IPO Capital Raise Can’t Save the Business from Heavy Competition

While Sweetgreen’s IPO will certainly help fund its expansion ambitions, no amount of capital can stop the number of current restaurants that offer salads and bowls on their menus or the ever-growing number of salad-focused fast-casual concepts.

Sweetgreen reminds us of another fast-casual concept facing heaving competition, Shake Shack (SHAK), which was once touted as the next Chipotle (CMG). Shake Shack’s shares have underperformed the S&P 500 since its IPO, and the company has failed to grow Core Earnings[2] since 2018. Sweetgreen’s path to profitability is even more narrow, given its more niche market and costly business model, as detailed below.

Local Sourcing Model Is Expensive

Unlike McDonald’s, and other more established restaurants, which enjoy economies of scale from a vertically integrated supply chain, Sweetgreen focuses on sourcing its food locally. To do this, Sweetgreen typically relies on a single, regional third-party distributor for fresh products and another regional distributor for dry goods. By not utilizing national distributors, Sweetgreen adds complexity to its supply chain, which makes it more difficult and potentially more costly to manage. For instance, Sweetgreen has more domestic food partners (200) than restaurants (140).

Chipotle, which offers its own variation of a salads relies on more traditional large-scale food suppliers which helps the company better manage costs. In 2020, Chipotle locally sourced only 11% of its produce from 54 local farmers to serve its ~2,900 stores.

This relative inefficiency leads to higher operating costs. Sweetgreen’s restaurant operating costs increased from 84% of revenue in 2019 to 88% of revenue in the nine months ended September 26, 2021. Chipotle’s restaurant operating costs[3], on the other hand, were just 77% of its food and beverage revenue in the nine months ended September 30, 2021.

Local Sourcing Is also Risky

While Sweetgreen claims it’s “connecting people to real food,” it will be increasingly difficult to maintain the quality of its produce as it increases the number suppliers and regional distribution partners. Relying on numerous third-party sources makes guaranteeing that quality control standards are maintained throughout the supply chain more complex.

A lack of control over its supply chain exposes Sweetgreen to even more risk than other types of restaurants as it serves large amounts of uncooked food, which is more susceptible to foodborne diseases. In 2019, when Sweetgreen received reports from New York City customers about illnesses caused from spoiled blue cheese from a local supplier, the company had difficulty tracing which restaurants received the spoiled product. As the company grows its store footprint, its ever-increasingly complex supply chain could expose its customers to riskier food.

Work-From-Home Trends Are Bad for Business

Before the pandemic, Sweetgreen had more than 1,000 Outposts – drop off points for offices, residential buildings, and hospitals – that delivered meals to consumers on a regular schedule. Sweetgreen notes in its S-1 that “Outpost customers have been our most habitual users, with the average Outpost customer ordering approximately six times per quarter.” Nearly all of its Outposts were closed in 2020 as offices closed during the pandemic. While the number of Outposts rose to ~35% of pre-pandemic levels in 3Q21, the long-term shift toward work-from-home will continue to slow this once promising growth driver.

Decreased Outpost sales mean lower sales per store for Sweetgreen. Though restaurant industry sales in the U.S. now exceed pre-pandemic levels, Sweetgreen’s average sales per store in 3Q21 is 18% below pre-pandemic 1Q20 levels. For comparison, Chipotle’s sales have already surged past pre-pandemic levels, and its average sales per store in 3Q21 is 19% above 1Q20 levels.

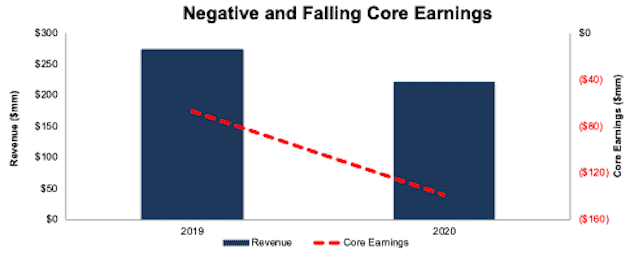

Profits Are Likely to Remain Negative

Unlike Shake Shack and Chipotle before their IPOs, Sweetgreen has never been profitable in any of its fiscal periods. On the other hand, Shake Shack’s pre-IPO GAAP earnings in 2014 were $2 million and Chipotle’s pre-IPO earnings in 2005 were $38 million.

While the COVID-19 pandemic caused major disruptions to the restaurant industry, 61% of the 33 restaurant companies we cover (excluding Sweetgreen) generated positive Core Earnings in 2020. All but three had positive Core Earnings in 2019.

Sweetgreen’s Core Earnings on the other hand fell from -$67 million in 2019 to -$139 million in 2020, per Figure 4. As the firm pursues its top-line growth strategy, heavy competition is likely to keep the company from ever achieving meaningful profits.

Figure 4: Sweetgreen Revenue & Core Earnings: 2019-2020

Sources: New Constructs, LLC and company filings

Sweetgreen Is Priced to Grow Faster than Chipotle

When we use our reverse discounted cash flow (DCF) model to analyze the future cash flow expectations baked into Sweetgreen’ expected valuation, we can provide clear, mathematical evidence that the $24/share valuation is too high and offers unattractive risk/reward.

To justify a $24/share valuation, Sweetgreen must:

- improve its NOPAT margin to 4% (vs. -57% TTM) in 2021, 8% in 2022, and 12% (Chipotle’s best-ever margin) from 2023-2030, and

- grow revenue by 24% (vs. -20% in 2020) compounded annually for the next ten years, which is 3x the expected industry growth rate through 2025.

In this scenario, Sweetgreen would generate $1.9 billion in revenue, or more than 8x its 2020 revenue, and $233 million in NOPAT, which is nearly equal to the TTM NOPAT of Jack in the Box (JACK) or Brinker International (EAT), which owns Chili’s and Maggiano’s. This implied NOPAT would also be 6x Shake Shack’s 2019 TTM NOPAT.

In this scenario, Sweetgreen’s 24% revenue CAGR is higher than the 22% revenue CAGR Chipotle achieved in its first 10 years after going public.

DCF Scenario 2: Growth Exceeds 2x Fast Casual Projections

We review an additional DCF scenario to highlight the downside risk should Sweetgreen’s revenue grow “only” 2x projected industry growth.

If we assume Sweetgreen’s:

- NOPAT margin rises to 4% (vs. -57% TTM ) in 2021 and 7% in 2022, and 11% (equal to Chipotle’s TTM margin) from 2023-2030, and

- revenue grows by 16% (2x the projected industry growth CAGR from 2021-2025) compounded annually from 2021-2030, then

Sweetgreen is worth just $6/share today – a 75% downside to the expected midpoint IPO valuation. See the math behind this reverse DCF scenario.

Should Sweetgreen struggle to improve margins at such a rapid pace or grow revenue more in line with the overall industry, the stock could be worth nothing.

DCF Scenario 3: Sweetgreen Matches Shake Shack’s Margins

We review an additional DCF scenario to highlight the downside risk should Sweetgreen’s margins match Shake Shack instead of Chipotle.

If we assume Sweetgreen’s:

- NOPAT margin rises to 4% in 2021 and 6% (equal to Shake Shack’s average margin since its IPO) from 2022-2030, and

- revenue grows by 16% (2x the projected industry growth CAGR from 2021-2025) compounded annually from 2021-2030, then

Sweetgreen is worth $0 to shareholders. See the math behind this reverse DCF scenario.

In this scenario, Sweetgreen’s NOPAT in 2030 is $59 million. After accounting for total debt, preferred stock, and outstanding employee stock options that decrease shareholder value by $985 million, there is no remaining value for shareholders. See details at the bottom of the report.

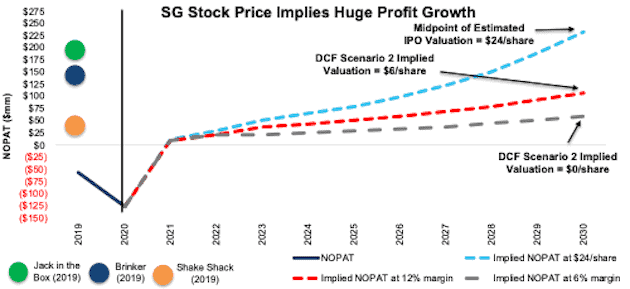

Figure 5 compares the firm’s implied future NOPAT in these three scenarios to its historical NOPAT. We also include the 2019 (pre-pandemic) NOPATs for Jack in the Box, Brinker, and Shake Shack for reference.

Figure 5: Expected IPO Valuation Is Too High

Sources: New Constructs, LLC and company filings

Each of the above scenarios also assumes Sweetgreen’s invested capital grows 3-5% annually through 2030. This assumption is conservative given the company plans to double its store count over the next three to five years. For reference, fast-growing, fast-casual restaurant Shake Shack grew invested capital 22% compounded annually from 2012 to 2020. Should Sweetgreen’s invested capital grow at an even faster rate than assumed in the scenarios above, the stock has even more downside risk.

An Acquisition of Sweetgreen Is Unlikely

On its own, Sweetgreen is unlikely to generate the profits needed to justify a valuation of $24/share. The best hope IPO investors in Sweetgreen might have is for an established company to acquire the firm. However, as we’ve stated in our most recent report on Shake Shack, the fast-casual restaurant boom reminds us of the early days in the craft beer industry with many different concepts fighting for a slice of the market.

However, the big difference for the fast-casual industry, is that it is much cheaper for large, national companies to replicate a concept than acquire a firm. Larger firms have a long history of being able to quickly and easily introduce competing products. In other words, the acquisition premium, or hope for a white knight buyer, is low for Sweetgreen.

Look Out for These Red Flags

With a lofty valuation that implies significant improvement in both revenue and profits, investors should be aware that Sweetgreen’s S-1 also includes these other red flags.

Public Shareholders Have No Rights: A downside of investing in Sweetgreen’s IPO, and other recent IPOs, is the fact that the shares provide little to no say over corporate governance. Investors in the IPO will get Class A shares, with just one vote per share. Sweetgreen’s co-founders will retain control of the firm with ~60% of the voting power as holders of Class B shares, which get 10 votes per share.

Non-GAAP EBITDA Understates Losses: Long a favorite of unprofitable companies, Sweetgreen’ chosen non-GAAP metric, Adjusted EBITDA, shows a much rosier picture of the firm’s operations than GAAP net income or our Core Earnings. Adjusted EBITDA gives management significant leeway in how it presents results.

For instance, Sweetgreen’ Adjusted EBITDA in 2020 removes $27 million (12% of revenue) in depreciation and amortization and $5 million (2% of revenue) in share-based compensation expense. After removing all items, Sweetgreen reports adjusted EBITDA of -$107 million in 2020. Meanwhile, economic earnings, the true cash flows of the business, are much lower at -$158 million.

While Sweetgreen’s adjusted EBITDA fell alongside economic earnings from 2019 to 2020, investors need to be aware that there is always a risk that Adjusted EBITDA could be used to manipulate earnings going forward.

We Don’t Know If We’ll Get Full Financial Transparency: Sweetgreen is going public as an emerging growth company which means its, “financial statements may not be comparable to companies that comply with new or revised accounting pronouncements as of public company effective dates.”

More specifically, Sweetgreen is exempt from:

- providing an auditor’s attestation report on the company’s internal controls over financial reporting requirements of Section 404(b) of the Sarbanes-Oxley Act

- disclosing all the obligations regarding executive compensation

- immediately complying with new or revised accounting standards

Without full financial transparency, shareholders in Sweetgreen cannot conduct the same level of due diligence as with other companies.

Critical Details Found in Financial Filings by Our Robo-Analyst Technology

Fact: we provide superior fundamental data and earnings models – unrivaled in the world.

Proof: Core Earnings: New Data and Evidence, forthcoming in The Journal of Financial Economics.

Below are specifics on the adjustments we make based on Robo-Analyst findings in Sweetgreen’ S-1:

Income Statement: we made $17 million of adjustments, with a net effect of removing $15 million in non-operating expenses (7% of revenue). You can see all the adjustments made to Sweetgreen’s income statement here.

Balance Sheet: we made $362 million of adjustments to calculate invested capital, all of which increase invested capital. The most notable adjustment was $289 million in operating leases. This adjustment represented 126% of reported net assets. You can see all the adjustments made to Sweetgreen’s balance sheet here.

Valuation: we made $985 million of adjustments to shareholder value, all of which decrease shareholder value. The most notable adjustment to shareholder value was $506 million in preferred stock. This adjustment represents 19% of the valuation at the midpoint IPO price range. See all adjustments to Sweetgreen’s valuation here.

Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life.

This article originally published on November 15, 2021.

Disclosure: David Trainer, Kyle Guske II, and Matt Shuler receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] This list is a sample of Sweetgreen’s competitors and is not exhaustive, but serves to illustrate the crowded nature of Sweetgreen’s target market.

[2] Only Core Earnings enable investors to overcome the inaccuracies, omissions and biases in legacy fundamental data and research, as proven in Core Earnings: New Data & Evidence, written by professors at Harvard Business School (HBS) & MIT Sloan and published in The Journal of Financial Economics.

[3] Includes food, beverage, and packaging, labor, occupancy, and other operating costs to match Sweetgreen’s “Total Restaurant Operating Costs”, which are reported to include food, beverage, and packaging, labor and related expenses, occupancy and related expenses, and other restaurant operating costs.