To help investors sort through the confusion, we present three different proposed valuations for Spotify based on three different scenarios of growth and profitability.

This firm's shrinking cash flows can’t cover its debt burden, its accounting is confusing and possibly unreliable, its industry faces technological disruption, and its valuation assumes implausibly high profit growth.

This company has an unprecedented history of growth and profitability, along with a well-deserved reputation as one of the most advanced and innovative companies in the world.

Today’s news that Alphabet, Apple, and Disney are unlikely to bid for Twitter should come as no surprise. We think these companies (and many investors) are doing the same work we have done and simply cannot stomach paying anywhere close to Twitter’s current price.

It’s time to consider a new paradigm for interest rates – a paradigm where treasury rates remain ultra low and riskier investments are priced by a decentralized market instead of a central bank.

The bottom line is that there is a limit for how much Alphabet should pay for TWTR in order for the deal to be economically profitable. Even in the most optimistic scenario for TWTR’s future cash flows, Alphabet should pay no more than $1.1 billion, or $1.55/share, for Twitter.

I think we are seeing the start of that process in late 2015 and early 2016. The combination of a slowdown in China, falling energy prices, and the end of zero interest rate policy from the Fed have put markets and the global economy in an interesting state of transition.

After greatly outpacing the gains of the market over the past two years, we believe Expedia Inc. (EXPE) could be the next momentum stock to see its run end. A mix of overvaluation and destruction of shareholder value lead Expedia into the Danger Zone this week.

Telecom and wireless operators are often cited as following the same path as traditional television providers, e.g. Comcast (CMCSA) and Time Warner Cable (TWC), which many believe are being replaced by newer, streaming providers like Netflix (NFLX), Amazon (AMZN), or Google’s (GOOGL) YouTube. This negative view has created an investing opportunity in one of the best companies the telecom industry has to offer.

Twitter went public in late 2013 touting excellent customer growth, equally impressive revenue growth, and the potential to be the “next big thing.” The stock has much farther to fall and earns a place in the Danger Zone this week.

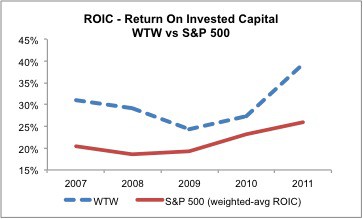

This week's stock pick of the week has one of the highest returns on invested capital (ROIC) in our model, and its recent guidance update and cheap valuation indicates that now might be the perfect entry point.

Without careful footnotes research, investors would never know the amount of employee stock options that decrease the amount of future cash flow available to shareholders by diluting the value of existing shares.

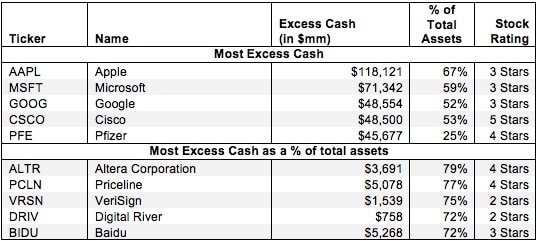

Most companies hold some cash—or cash equivalents in the form of investments—above this required amount. Companies hold excess cash in order to cushion against economic downturns, prepare for acquisitions, or any number of other reasons. Sometimes, past profits pile up on balance sheets and are a form of excess cash. Excess cash is not needed for the operations of a company. It is removed from our calculation of invested capital.

Too many investors are looking at AAPL through the rear view mirror and assume that its sky-high profits and return on invested capital (ROIC) are sustainable. As I detail in my CNBC interview, Apple is not cheap and investors should not underestimate the impact of losing Steve Jobs.