We closed this position on May 17, 2022. A copy of the associated Position Update report is here.

Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life.

Last week we warned investors to avoid the Small Cap Growth style. This week, we’ve identified a fund that has outperformed in recent years but allocates to significantly overvalued stocks.

Despite its 4 or 5-Star Morningstar rating (depending upon share class), Columbia Small Cap Growth Fund (CGOAX and more) is a mutual fund investors should avoid. Our research into the fund’s holdings[1] reveals stocks with poor risk/reward compared to the benchmark. Throw in costly fees, and this fund lands in the Danger Zone.

Traditional Research Overrates this Fund

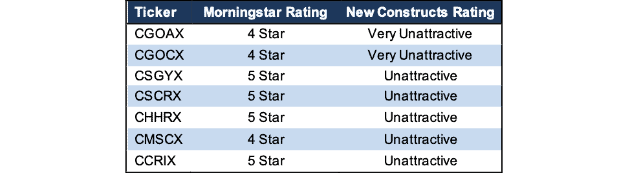

Per Figure 1, CGOAX, CGOCX, and CMSCX receive a 4-Star rating from Morningstar and CSGYX, CSCRX, CHHRX, and CCRIX receive a 5-Star rating. All seven classes receive a “Strong Buy” rating from Zacks. When viewed through our Predictive Risk/Reward Fund Rating methodology, all share classes earn an Unattractive or Very Unattractive rating.

Figure 1: Columbia Small Cap Growth Fund Ratings

Sources: New Constructs, LLC, company, ETF and mutual fund filings, Morningstar, and Zacks

Holdings Research Reveals a Low-Quality Portfolio

The only justification for a mutual fund to charge higher fees than its ETF benchmark is “active” management that leads to out-performance. A fund is most likely to outperform if it has higher quality holdings than its benchmark. To assess holdings quality, we leverage our Robo-Analyst technology[2] to drill down and analyze the individual stocks in every fund we cover.

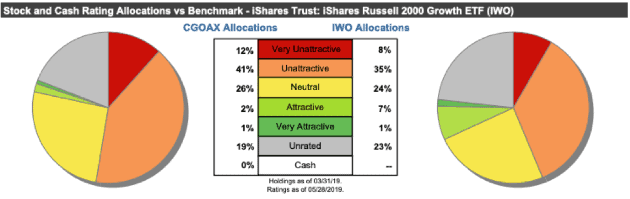

Figure 2: Columbia Small Cap Growth Fund Asset Allocation vs. Benchmark

Sources: New Constructs, LLC and company, ETF and mutual fund filings

We showed last week that stocks in the Small Cap Growth style as a whole are less profitable and more expensive than the S&P 500. Per Figure 2, Columbia Small Cap Growth Fund’s asset allocation poses even greater downside risk and holds less upside potential than the already risky style benchmark, the iShares Russell 2000 Growth ETF (IWO). CGOAX allocates only 3% of its portfolio to Attractive-or-better rated stocks compared to 8% for IWO. On the flip side, CGOAX’s exposure to Unattractive-or-worse rated stocks is much higher, at 53%, than IWO, at 43%.

Six of the mutual fund’s top 10 holdings receive an Unattractive-or-worse rating. These 6 stocks make up 17% of its portfolio. In total, each of the top 10 holdings receive a Neutral-or-worse rating and make up 26% of CGOAX’s portfolio.

Given the unfavorable allocation of Very Attractive vs. Very Unattractive stocks relative to the benchmark, Columbia Small Cap Growth Fund appears poorly positioned to generate the outperformance required to justify its fees.

Stock Selection Process Doesn’t Find Quality Stocks

When selecting investments, the managers of CGOAX look for “high-quality companies earning above their cost of capital with the ability to sustain above-average rates of EPS growth.” In the fund’s annual report, it’s stated some factors considered include “five-year+ growth opportunities, ability to redeploy capital repeatedly with high and/or improving returns, and management teams that operate their businesses with a culture of ownership.”

We’ve shown before that earnings growth has little correlation with creating shareholder value, and the other factors the fund uses to select stocks have not led it to quality stocks, either. Instead, the fund allocates to stocks less profitable and more expensive than its benchmark and the S&P 500.

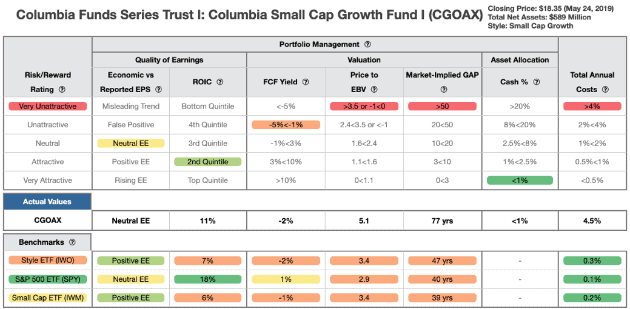

Figure 3 contains our detailed rating for CGOAX, which includes each of the criteria we use to rate all funds under coverage and shows the fund’s poor portfolio management. These criteria are the same for our Stock Rating Methodology, because the performance of a fund’s holdings equals the performance of a fund after fees.

Figure 3: Columbia Small Cap Growth Fund Rating Breakdown

Sources: New Constructs, LLC and company, ETF and mutual fund filings

As Figure 3 shows, CGOAX’s holdings are inferior or only equal to IWO and SPY in four of the five criteria that make up our holdings analysis. Specifically:

- The return on invested capital (ROIC) for CGOAX’s holdings is 11%, which is below the 18% earned by companies held by SPY.

- The -2% free cash flow yield of CGOAX’s holdings means managers do not allocate to companies generating positive cash flows and is equal to the FCF yield of IWO stocks and less than the 2% earned by SPY stocks.

- The price-to-economic book value (PEBV) ratio for CGOAX is 5.1 compared to 3.4 for IWO and 2.9 for SPY.

- Our discounted cash flow analysis reveals an average market-implied growth appreciation period (GAP) of 77 years for CGOAX holdings compared to 47 years for IWO and 40 years for SPY.

While the fund finds stocks with a higher ROIC than the benchmark, it fails to find high ROIC stocks trading at cheap valuations. Some top holdings include Alteryx (AYX), Exponent (EXPO), and Paycom Software (PAYC), which earn a 75%, 44%, and 31% ROIC respectively. However, each of these stocks has an Unattractive-or-worse PEBV and GAP rating. Ultimately, these high ROIC stocks are significantly overvalued, which makes them poor investments.

All things considered, this analysis above reveals that the companies held by CGOAX earn inferior cash flows (as measured by ROIC) but are valued at a premium (as measured by FCF yield, PEBV, and GAP) when compared to the benchmark and general market (S&P 500).

How Using the Wrong Metrics Adds Risk

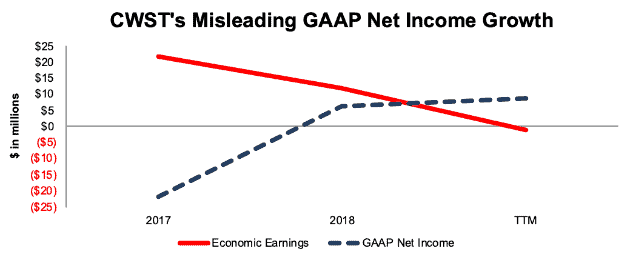

Casella Waste Systems (CWST: $38/share) is one of CGOAX’s holdings that perfectly illustrates why relying on metrics such as earnings can lead to bad stock picks. Since 2017, CWST’s GAAP net income improved from -$22 million to $9 million.

Misleading Earnings Get Missed. However, CWST’s economic earnings, which account for items hidden in the footnotes & MD&A of company filings and changes to the firm’s invested capital, fell from $22 million in 2017 to -$1 million over the trailing twelve months (TTM), as shown in Figure 4.

Figure 4: CWST’s GAAP Obscures Falling Economic Earnings

Sources: New Constructs, LLC and company filings

To calculate economic earnings, we must first remove non-operating expenses and income, such as the $492 thousand (8% of 2018 GAAP net income) gain on the sale of property & equipment. Only by adjusting for these items can we calculate the true operating profits of the business.

Economic earnings also account for changes to the balance sheet, from which we made the following adjustments:

- $85 million (14% of reported net assets) in off-balance sheet operating leases

- $61 million (10% of reported net assets) in asset write-downs

By adding these items back to invested capital, we hold CWST accountable for all capital invested in the business. These adjustments, when combined with a rising weighted average cost of capital (6.3% in 2018, up from 4.6% in 2016), increase the capital charge and decrease economic earnings.

Despite the deterioration in the true profits of the company, shares remain significantly overvalued.

Overvalued Price Gets Missed. To justify its current price of $38/share, CWST must maintain TTM NOPAT margins (6%) and grow NOPAT by 10% compounded annually for the next 13 years. See the math behind this dynamic DCF scenario. This scenario seems overly optimistic given that CWST’s NOPAT has fallen from $57 million in 2017 to $43 million TTM and when considering CWST’s shareholder destruction since 2017 (as seen in Figure 4).

Even if we assume CWST can achieve 2018 NOPAT margins (8.5%) and grow NOPAT by 8% compounded annually for the next decade, the stock is worth only $26/share today – a 32% downside. See the math behind this dynamic DCF scenario.

Excessive Fees Make Outperformance Even More Difficult

At 4.53%, CGOAX’s total annual costs (TAC) are higher than all of the 403 Small Cap Growth style funds under coverage. For comparison, the average TAC of all Small Cap Growth mutual funds under coverage is 1.94%, the weighted average is 1.55%, and the benchmark ETF (IWO) has total annual costs of 0.26%.

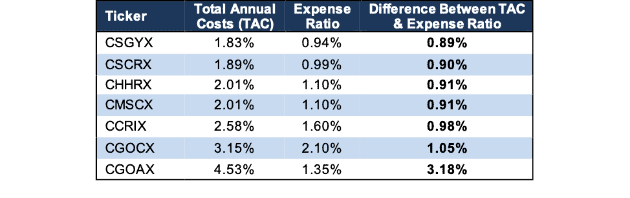

Per Figure 5, Columbia Small Cap Growth Fund’s expense ratios understate the true costs of investing in this fund. Our TAC metric accounts for more than just expense ratios. We consider the impact of front-end loads, back-end loads, redemption fees, and transaction costs. For example, CGOAX’s annual turnover ratio of 156% adds 0.80% to its total annual costs that aren’t captured by the expense ratio.

Figure 5: Columbia Small Cap Growth Fund’s Real Costs

Sources: New Constructs, LLC and company, ETF and mutual fund filings

To justify its higher fees, each class of the fund must outperform its benchmark by the following over three years:

- CGOAX must outperform by an average of 4.26% annually.

- CGOCX must outperform by an average of 2.88% annually.

- CCRIX must outperform by an average of 2.31% annually.

- CMSCX must outperform by an average of 1.74% annually.

- CHHRX must outperform by an average of 1.74% annually.

- CSCRX must outperform by an average of 1.62% annually.

- CSGYX must outperform by an average of 1.56% annually.

An in-depth analysis of CGOAX’s TAC is on page 2 here.

CGOAX’s Performance Can’t Justify Its Fees

When we take into account its load, which adds 2.19% to its total annual costs, we see that while CGOAX has outperformed in the short-term, it has failed to outperform enough to justify its fees.

CGOAX’s 3-year quarter-end average annual total return outperformed IWO by 4%, which does not meet the 4.26% outperformance required to justify its fees. Its 10-year quarter-end average annual total return actually underperformed IWO by 40 basis points. For reference, CGOAX must outperform its benchmark by 2.69% annually over 10 years to justify its fees.

Given that 53% of assets are allocated to stocks with Unattractive-or-worse ratings, CGOAX looks likely to underperform moving forward.

The Importance of Holdings-Based Fund Analysis

Smart fund investing means analyzing the holdings of each mutual fund, which in the past was nearly impossible for the average investor. Instead, investors were content to buy a fund based on past performance, but studies show such a strategy does not necessarily lead to outperformance. Only through holdings-based analysis can one determine if a fund’s methodology is sound and actually allocates to high-quality stocks.

Holdings-based analysis is no longer impractical for the average investor. Through our partnerships with TD Ameritrade and Interactive Brokers, investors can access our research and enjoy the sophisticated fundamental research that Wall Street insiders use. Our machine learning and Robo-Analyst technology helps investors navigate the fund landscape by analyzing the holdings of 7,500+ ETFs and mutual funds under coverage. This diligence allows us to cut through the noise and identify potentially dangerous funds that traditional backward-looking fund research may overlook, such as CGOAX.

This article originally published on June 3, 2019.

Disclosure: David Trainer, Kyle Guske II, and Sam McBride receive no compensation to write about any specific stock, sector, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] This paper compares our analytics on a mega cap company to other major providers. The Appendix details exactly how we stack up.

[2] Harvard Business School features the powerful impact of our research automation technology in the case study New Constructs: Disrupting Fundamental Analysis with Robo-Analysts.