Corporate earnings season may be winding down, but the real earnings season – annual 10-K filing season – starts today.

Corporate earnings announcements provide investors with limited and often misleading data. Only by reading all of the financial footnotes, which are only included in annual 10-K reports, can investors analyze true profits.

In the few 10-Ks already filed in 2019, the footnotes make one stock look better than what the headline numbers show.

Analyzing Footnotes Allows Us to Reverse Distortions in Reported Earnings and Valuations

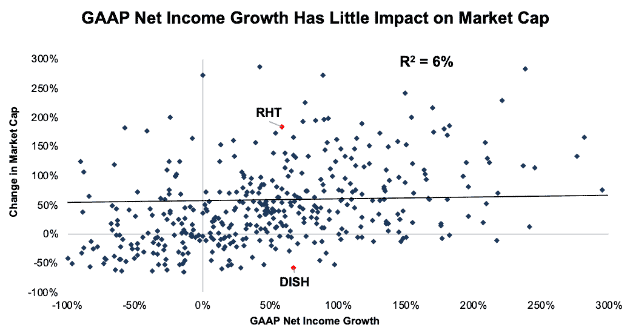

Figure 1 shows that GAAP net income growth over the past five years has almost no impact on the change in market cap for companies in the S&P 500.[1]

Figure 1: GAAP Net Income Growth and Change in Market Cap Over the Past Five Years

Sources: New Constructs, LLC and company filings.

Note that Red Hat (RHT) and Dish Network (DISH) have grown GAAP net income by a similar amount over the past five years (58% for RHT, 67% for DISH). However, RHT’s market cap has nearly tripled while DISH’s has fallen by more than half. When accounting for changes in share count, RHT’s stock is up 206% over the past five years while DISH is down 45%.

GAAP earnings growth for both companies is distorted due to the impact of the new tax law on TTM earnings. When we strip out accounting distortions, RHT grew after-tax operating profit (NOPAT) by 123% over the past five years, while DISH grew NOPAT by just 8%.

In addition, GAAP earnings ignore changes to the balance sheet. RHT employs a capital-light model that helped it improve ROIC from 8% in 2014 to 15% TTM and generate $800 million (3% of market cap) in free cash flow over the same time.

Meanwhile, DISH has spent billions of dollars on wireless spectrum rights that have yet to produce any significant value. As a result, ROIC has fallen from 15% in 2014 to 6% TTM and DISH has burned through $11.6 billion (84% of market cap) in negative free cash flow over that time.

Cash is a fact. Earnings are an opinion. Investors who base their investment decisions on accounting earnings put their portfolios at risk. Advisors who make investment recommendations without performing proper due diligence are not fulfilling their fiduciary responsibilities.

Diligence in Footnotes Pays – Avoid Blowups

All stock research is ultimately judged on one metric: the performance of picks. Over the past year, our in-depth research has helped investors avoid blowups and identify top performers.

At the end of last year’s filing season, we put Hertz Global Holdings (HTZ) in the Danger Zone due to its misleading and possibly unreliable accounting. Since our article, the stock is down 16% while the S&P 500 is flat.

We found a handful of significant items in HTZ’s 2017 10-K that raised red flags at the time.

- On page 139 we found a $679 million (7% of revenue) benefit from tax reform that gave the illusion of rising earnings even though economic earnings continued to decline.

- On page 136, we found operating lease commitments with a present value of $1.9 billion (128% of market cap) to go along with $14.9 billion in debt on the balance sheet.

- On page 78, we found an opinion from HTZ’s auditor that the company failed to maintain effective internal control over its financial reporting. Investors who paid attention to this red flag avoided a nasty surprise this past December when HTZ was forced to pay a $16 million settlement to the SEC over accounting errors.

HTZ currently looks like a value stock due to its cheap P/E of 3 and its P/B of 1.2. However, as we’ve written about in the past, both of those metrics are misleading. HTZ’s P/E will rise dramatically after its next earnings report when it no longer has the tax benefit to boost its earnings, and over half of its accounting book value consists of goodwill that can be written down at any time. The stock has underperformed over the past year, and should continue to fall as investors recognize its lack of value.

Diligence in Footnotes Pays – Hidden Gems

On the other side of the coin, Cummins Inc (CMI) is up 7% (S&P up 3%) since we featured the stock as a Long Idea in November 2018.

In our original Long Idea (featured in Barron’s), we highlighted a $782 million (3% of revenue) charge from tax reform in Q4 2017 and non-recurring expenses in Q1 and Q2 2018 that added up to $368 million (2% of revenue) due to field campaigns to repair older model engines that failed emissions tests.

CMI filed its 2018 10-K on February 11, and while we didn’t find any other items as big as those, we did identify a handful of smaller adjustments that also have a positive impact on NOPAT.

- On page 83, the removal of an additional $12 million in non-operating tax expense in 2018 as the company continues to account for the impact of tax reform.

- On page 87, an adjustment for the impact of a $5 million increase to the company’s LIFO reserve.

- On page 29, the company disclosed that it adopted the new pension cost accounting rule that reclassified components of pension cost from operating to non-operating income. In 2017, CMI earned $31 million in non-operating income from these items, but with the new rule these items are no longer distorting reported operating income.

As a result of these changes and adjustments, both GAAP net income and reported operating income understate CMI’s true profitability. The company reported $2.1 billion in GAAP net income, but our adjustments show that they earned $2.4 billion in NOPAT. Meanwhile, reported operating income increased by 19% from 2017, but our adjustments show that net operating profit before tax (NOPBT) grew by 36%.

Cummins was already one of our top stock picks, and our analysis of its 2018 10-K only heightens our conviction on this stock.

All the media buzz during “earnings” season tends to push investors into shortsighted trades. We help long-term investors create a durable competitive advantage by reading thousands of 10-Ks so they can invest with the level of diligence they’ve always wanted but could not get before.

Using Machine Learning to Provide Footnotes Diligence at Scale

ROIC is much better than EPS at explaining changes in valuation. Unfortunately for investors, it is very difficult to calculate accurately. It’s not enough to read financial statements. A rigorous calculation of ROIC must account for items that are buried in hundreds of pages of footnotes.

For a human analyst, performing this level of analysis on just a handful of companies is a daunting task. Applying that level of rigor to thousands of companies is downright impossible. That’s where the Robo-Analyst comes in.

We use machine learning and natural language processing to automate the analysis of corporate filings. Our statistical comparison engine, which has been trained on over 120,000 human-verified filings and grows more sophisticated every day, can filter through SEC filings to recognize and tag important data, automatically building company models.

Of course, human analysts remain a vital part of the process. From mid-February through the end of March, our expert team of analysts will be coming in early and staying late to validate the data and models built by the machine and interpret unusual items that cannot be automatically processed.

This combination of computerized processing power and human expertise allows us to provide investors with the most accurate research from the “real” earnings season. Harvard Business School featured the powerful impact of our research automation technology in the case study “New Constructs: Disrupting Fundamental Analysis with Robo-Analysts.” Ernst & Young affirmed the superiority of our ROIC calculation in a recent white paper. Best of all, through our partnerships with TD Ameritrade and Interactive Brokers, more investors than ever before can access our research and enjoy the sophisticated fundamental research that Wall Street insiders use.

This article originally published on February 19, 2019.

Disclosure: David Trainer, Sam McBride, and Kyle Guske II receive no compensation to write about any specific stock, sector, style, or theme.

Follow us on Twitter (#filingseasonfinds), Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] Figure 1 excludes companies for which we don’t have data going back 5 years or whose GAAP net income 5 years prior is negative. After these exclusions, the regression analysis contains 467 companies.