We published an update to this Danger Zone pick on January 10, 2022. A copy of the associated Earnings Update report is here.

Tesla’s (TSLA: $1,200/share) market cap surpassed the trillion-dollar mark, driven by a post-earnings rally that got a boost from the announcement of a 100,000-vehicle order from Hertz (HTZ), which might not even happen.

Even if it does come to pass, the Hertz order is a drop in the bucket of growth expectations baked into Tesla’s valuation. Tesla needs 155 Hertz-sized orders to justify the revenue expectations in its stock price. Put another way, the $1.2 trillion valuation implies Tesla owns 60%+ of the entire global passenger EV market and becomes more profitable than Apple (AAPL) by 2030.

This report provides objective perspective on how outrageously high the valuation of Tesla stock is and the clear impracticality of the company meeting the expectations baked into its valuation.

Tesla’s Valuation vs. Competitors Makes No Sense

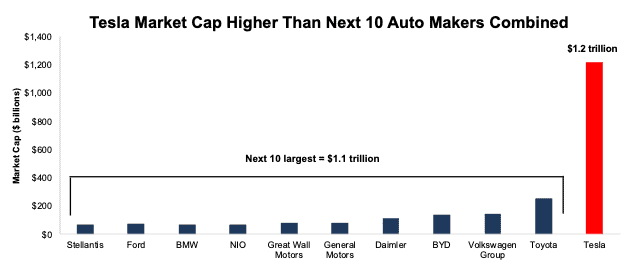

Tesla’s market cap is now greater than the next 10 largest (ranked by market cap) auto manufacturers combined.

Figure 1: Tesla’s Market Cap Vs. Competitors

Sources: New Constructs, LLC and company filings

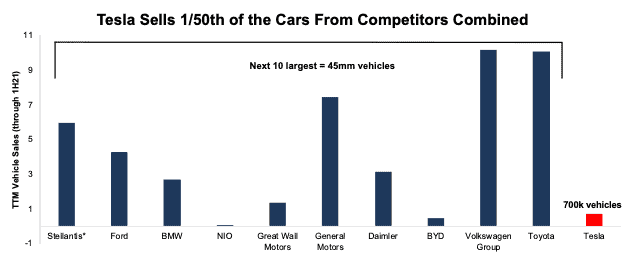

This valuation comes despite Tesla selling less than 1/50th of the vehicles than the combined total sold by the next 10 largest automakers over the trailing twelve months ended the first half of 2021. See Figure 2.

We cannot conceive of a straight-faced argument for the disconnect between Tesla’s valuation and its vehicle sales compared to its competitors.

Figure 2: Tesla’s Car Sales Vs. Competitors

Sources: New Constructs, LLC and company filings

* Stellantis sales estimated as Fiat Chrysler and PSA Group’s 2H20 sales and Stellantis’ 1H21 sales. Stellantis was formed as a merger between the two in January 2021.

Is the Hertz Deal Really Worth $100 Billion+ in Market Cap?

Even if Hertz eventually agrees to buy 100,000 Tesla Model 3s, we do not think it is worth the $100 billion in market cap, or $1 million per vehicle, that we saw investors give Tesla’s market cap after the Hertz deal made headlines. Even Elon Musk questioned the surge in share price, noting that the price movement was “strange” given that Tesla is “very much a production ramp problem, not a demand problem.”

This $100 billion market cap jump makes even less sense in the context of Tesla’s sky-high valuation before the announcement. Clearly, the feasibility of Tesla meeting the sales expectations embedded in its market cap plays no role in its valuation. For those that do care about expectations investing, we did the math and Tesla needs to successfully deliver on 155 Hertz-sized deals to meet the sales implied by a $1.2 trillion market cap.

Will the Hertz Deal Result in Any Profits – If It Goes Through?

After Elon Musk tweeted on November 1, 2021 that “no contract has been signed yet”, the Hertz deal reminds us of another famous tweet: "am considering taking Tesla private at $420. Funding secured.”

Even if the deal does go through, the pricing terms are very unclear. Elon insists that no cars will be sold at a discount. Meanwhile, Hertz CEO Mark Fields has made it clear that he is playing the field and working on getting cars from all EV manufacturers on his lot.

Either Tesla is selling cars at a (large or small) discount, the deal terms are wrong, or the deal does not get done. If the deal gets done, we do not expect it to be profitable. Rental car companies are accustomed to getting discounts for bulk orders, and we see no reason for Hertz to expect to pay list prices on a deal for so many cars.

At the end of the day, we’re not sure pricing matters because we don't think the Hertz deal gets done. This affair is more about headlines and fueling speculation than doing any real business.

Tesla’s Global Market Share Getting Smaller

Tesla’s first-mover is already eroding, and its market share continues to decline. In the first half of 2021, Tesla sold 14.6% of the EVs sold worldwide compared to 18.8% over the same period in 2020.

Rising volumes, and falling market share are to be expected in a nascent industry. The problem is that Tesla’s isn’t priced for declining market share. It is priced for massive market share gains, unheard of gains in nearly any industry across the globe, especially in an industry as large and competitive as passenger vehicles.

Reverse DCF Math: Valuation Implies Tesla Will Own 60%+ of the Global Passenger EV Market

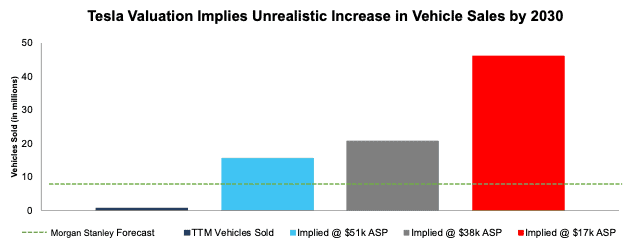

At its current average selling price (ASP) of ~$51k, Tesla’s stock price of ~1,200/share implies the firm will sell 16 million vehicles in 2030 (versus ~800k TTM), or 60% of the projected base case global EV passenger vehicle market in 2030. For reference, Adam Jonas, a Morgan Stanley analyst with a price target of $1,600/share, projects Tesla will sell 8.1 million vehicles in 2030.

We think it is unlikely that Tesla will sell such a high volume of vehicles at a $51k ASP, yet the implied vehicle sales based on lower ASPs look even more impractical.

As detailed in the next section, this analysis assumes Tesla achieves profit margins twice as high as Toyota (TM) and quadruples its current auto manufacturing efficiency. In other words, we aim to provide inarguably best-case scenarios for assessing the expectations reflected in Tesla’s stock price.

Per Figure 3, Tesla’s current valuation implies that, in 2030, it will sell the following number of vehicles based on these ASP benchmarks:

- 16 million vehicles – current ASP of $51k

- 21 million vehicles – ASP of $38k (average new car price in the U.S. in 2020)

- 46 million vehicles – ASP of $17k (equal to General Motors over the TTM)

If Tesla achieves those EV sales, the implied market share for the company would be the following (assuming global passenger EV sales reach 25.8 million in 2030, the base case projection from the IEA):

- 60% for 16 million vehicles

- 80% for 21 million vehicles

- 179% for 46 million vehicles

If we assume the IEA’s best case for global passenger EV sales in 2030, 46.8 million vehicles, the above vehicle sales represent:

- 33% for 16 million vehicles

- 44% for 21 million vehicles

- 98% for 46 million vehicles

Figure 3: Tesla’s Implied Vehicle Sales in 2030 to Justify Current Valuation

Sources: New Constructs, LLC and company filings

The Math Shows that Tesla Must be More Profitable Than Apple

Here are the assumptions we use in our reverse discounted cash flow (DCF) model to calculate the implied production levels above.

To justify its current price of ~$1,200/share, Tesla must:

- immediately achieve a 17.2% NOPAT margin (double Toyota’s margin, which is the highest of the large-scale automakers we cover), compared to Tesla’s TTM margin of 7.7%) and

- grow revenue by 38% compounded annually for the next decade.

In this scenario, Tesla generates $783 billion in revenue in 2030, which is 102% of the combined revenues of Toyota, General Motors, Ford (F), Honda Motor Corp (HMC), and Stellantis (STLA) over the TTM.

This scenario also implies Tesla generates $135 billion in net operating profit after-tax (NOPAT) in 2030, or 45% higher than Apple’s (AAPL) TTM NOPAT, which, at $93 billion, is the highest of all companies we cover.

TSLA Has 60%+ Downside If Morgan Stanley Is Right About Sales

If we assume Tesla reaches Morgan Stanley’s estimate of selling 8.1 million cars in 2030 (which implies a 31% share of the global passenger EV market in 2030), at an ASP of $38k, the stock is worth just $483/share. Details:

- NOPAT margin improves to 17.2% and

- revenue grows 27% compounded annually over the next decade, then

the stock is worth just $483/share today – 60% downside to the current price. See the math behind this reverse DCF scenario. In this scenario, Tesla grows NOPAT to $60 billion, or nearly 17x its TTM NOPAT, and just 3% below Alphabet’s (GOOGL) TTM NOPAT.

TSLA Has 88%+ Downside Even with 28% Market Share and Realistic Margins

If we estimate more reasonable (but still very optimistic) margins and market share achievements for Tesla, the stock is worth just $148/share. Here’s the math:

- NOPAT margin improves to 8.5% (equal to General Motors’ TTM margin, compared to Tesla’s TTM margin of 7.7%) and

- revenue grows by consensus estimates from 2021-2023 and

- revenue grows 18% a year from 2024-2030, then

the stock is worth just $148/share today – an 88% downside to the current price.

In this scenario, Tesla sells 7.2 million cars (at an ASP of 38k) and owns 28% of the global passenger EV market in 2030. If Tesla fails to meet these expectations, then the stock is worth less than $148/share.

Also, for this scenario, we assume a much more realistic NOPAT margin, 8.5%, for Tesla. Given the expansion required of the business, struggles to be profitable to date, and formidable competition, we think Tesla will be lucky to achieve and sustain a margin as high as 8.5% from 2021-2030.

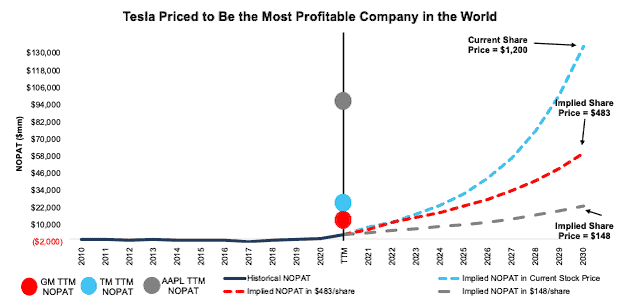

Figure 4 compares the firm’s historical NOPAT to the NOPAT implied by its current stock price, the 8.1 million vehicle sales scenario, and the 7.2 million vehicle sales scenario to illustrate just how high the expectations baked into Tesla’s stock price remain. For additional context, we show Toyota’s, General Motors’, and Apple’s TTM NOPAT.

Figure 4: Tesla’s Historical and Implied NOPAT: DCF Valuation Scenarios

Sources: New Constructs, LLC and company filings

Each of the above scenarios assumes Tesla’s invested capital grows 14% compounded annually through 2030. For reference, Tesla’s invested capital grew 53% compounded annually from 2010-2020 and 29% compounded annually from 2015-2020. Invested capital at the end of 3Q21 grew 21% YoY. Tesla’s property, plant, and equipment has grown even faster, at 58% compounded annually, since 2010.

A 14% CAGR represents 1/4th the CAGR of Tesla’s property, plant, and equipment since 2010 and assumes the company can build future plants and produce cars 4x more efficiently than it has so far.

In other words, we aim to provide inarguably best-case scenarios for assessing the expectations for future market share and profits reflected in Tesla’s stock market valuation.

Why Tesla’s $1 Trillion Valuation Is Ridiculous

Now that we’ve shown how high the expectations baked into Tesla’s valuation are, we’ll present some of the many challenges Tesla faces to meet those expectations.

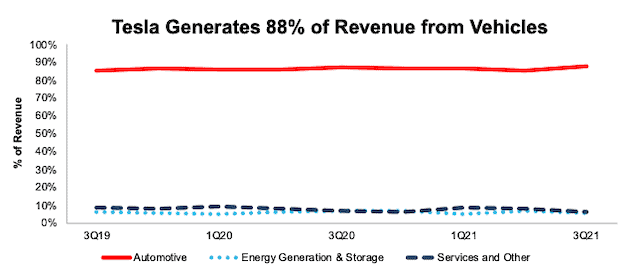

Tesla Remains “Just” a Car Company, Despite Bulls’ Arguments Otherwise. One of the most common arguments bulls make to justify Tesla’s valuation is that the company is more than just a car company. Instead, the argument goes: Tesla is a software, tech, insurance, energy, transportation, “insert any other blank” company. However, the financials bear out a different picture and show the other businesses are more hype than substance. At this point, Tesla is a only car company and generates the entirety of its profits from vehicles.

Per Figure 5, Tesla generated 88% of revenue from Automotive Sales in 3Q21, which is up from 87% in 3Q20, and above the quarterly average of 86% since 3Q19. For reference, automotive sales made up 87% and 93% of General Motors’ and Ford’s 3Q21 revenue respectively.

Figure 5: Tesla’s Revenue Breakdown: 3Q19 – 3Q21

Sources: New Constructs, LLC and company filings

Tesla’s two other segments, Energy generation and storage and Services and other, which make up 12% of revenue in 3Q21, are unprofitable. Over the TTM, Tesla generated $10.8 billion in gross profit. $11.2 billion came from its Automotive segment while Energy generation and storage and Services and other racked up gross losses of $113 million and $263 million. Despite many claims and promises to the contrary over the years, Tesla doesn’t generate gross profit doing anything but selling cars.

Insurance Business Is Not Material. Tesla bulls will also point to Tesla’s insurance business as another way to drive profit growth. We’ve previously covered how Tesla insurance does not have the competitive advantages that bulls ascribe to it and has a long way to go before it can get meaningfully off the ground.

Even if Tesla’s insurance business gets off the ground, we would not expect it to make much money. For example, from 2004-2006, General Motors generated about $70 per car sold in GAAP net income from its insurance business. If we assume Tesla can generate the same level of business, Tesla insurance would result in just $57 million in GAAP net income based on TTM vehicles sold.

Bulls will counter that Tesla will be so much better at insurance than GM and that GM is not a good comp. There is no way to know for sure. Nevertheless, we concede that anything is possible, but the likelihood of Tesla’s insurance business being material profit producer is extremely low.

Regardless of how successful Tesla insurance is, the potential profits from it are nowhere near enough to help to justify the expectations baked into Tesla’s stock price.

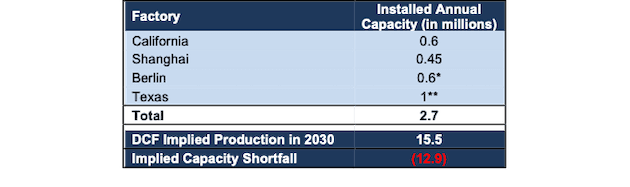

Production Capacity Growth Will Require Billions of $. Current and expected production capacities of all known Tesla factories equals ~2.7 million vehicles, or 12.9 million short of the 2030 production implied by its stock price. See Figure 6.

In other words, despite the new factories coming online, Tesla must spend billions and build many new manufacturing plants before it can approach the capacity needed to sell the number of cars implied by its valuation.

Given the many issues in ramping production in the past, investors should not assume Tesla can increase its production by 5x without any problems.

Figure 6: Tesla’s Pending Production Shortfall

Sources: New Constructs, LLC and company filings

*Projection based on InsideEVs estimate of 600,000 vehicles per year

**Optimistic assumption based on Texas being Tesla’s biggest factory and possibly the largest factory in the United States

Incumbents Must Fail for Tesla to Meet Growth Expectations. For many years now, incumbent automakers have spent billions of dollars building out their EV offerings. Automakers other than Tesla already account for 85% of global EV sales through the first half of 2021.

The global EV market is simply not big enough for Tesla to achieve the sales expectations in its valuation unless nearly all of the incumbents reverse course and completely fail to sell EVs.

Here are the projections from the large incumbent automakers that have provided specific goals for future EV production.

- Volkswagen Group projects that 50% of its global sales will be fully electric by 2030

- Stellantis projects 70% and 40% of its European and North American sales, respectively, will be fully electric by 2030

- Ford projects that 40% of its sales will be fully electric by 2030.

- Toyota projects that it will sell 2 million EVs by 2030

- Honda plans to sell only EVs in China by 2030

- BMW expects at least half its sales to be zero-emission vehicles by 2030

- Daimler, manufacturer of Mercedes Benz, expects half its sales to be “EV and hybrid by 2025”

- General Motors is targeting EV sales of “more than 1 million” by 2025

- Volvo plans to sell only fully electric vehicles by 2030

- Nissan projects 40% of U.S. sales to be EVs by 2030

Based on these projections, we estimate how many EVs each company aims to produce[1] by 2030 and the market share implied by that production as a percentage of base-case global passenger EV sales in 2030.

- Volkswagen Group: 5.5 million, 21% market share

- Stellantis: 3.6 million[2], 14% market share

- Ford: 2.2 million, 9% market share

- Toyota: 2 million, 8% market share

- Honda (in China): 1.5 million, 6% market share

- BMW: 1.3 million, 5% market share

- Mercedes Benz: 1.2+ million, 5% market share

- General Motors: 1+ million, 4% market share

- Volvo: 700,000, 3% market share

- Nissan (in U.S.): 500,000, 2% market share

- Total = 19+ million vehicles and 75% market share

These estimates do not include other incumbents and new entrants (e.g. Jaguar Land Rover, NIO Inc. [NIO], Rivian [RIVN], Ludic [LCID] and more) or other Chinese EV makers because we could not find specific projections for EV production. Nevertheless, we are confident that their combined market share will be more than zero.

The point is that the rest of the world is not planning to stand by, give up existing market share, and let Tesla own majority of the EV market. Many very experienced and successful automakers are spending many multiples of what Tesla is spending to compete in the EV market.

The bottom line is that it is hard to make a straight-faced argument that Tesla can achieve the sales implied by its valuation in a competitive market.

Incumbents Can Afford to Spend More than Tesla. Incumbents already have infrastructure to produce and sell vehicles at scale, and they are spending billions of dollars to compete in the EV market. Ford, Volkswagen, General Motors, and Stellantis alone are planning to spend at least $280 billion through 2025 and produce over 12 million EVs by 2030.

Given the huge investments from multiple competitors, we expect the EV market will be extremely competitive, as manufacturers fight for profits and market share. The “winner take all” outcome implied by Tesla’s valuation is extremely unlikely. Perhaps, Bernstein analyst Toni Sacconaghi said it best, “the automotive industry is an increasingly global and hypercompetitive industry and we believe that surplus profits and technology innovation will likely be competed away over time, as has been the case historically." In such a market, Tesla cannot achieve the market share implied by its valuation.

Unlike Tesla, the incumbents generate plenty of free cash flow (FCF) to fund their EV investments and don’t have to dilute existing shareholders to expand EV capacity as Tesla does. For instance, over the last five years, General Motors, Stellantis, and Ford generated a cumulative $12.4 billion, $7.1, and $6.1 billion in free cash flow while Tesla burned -$19.5 billion.

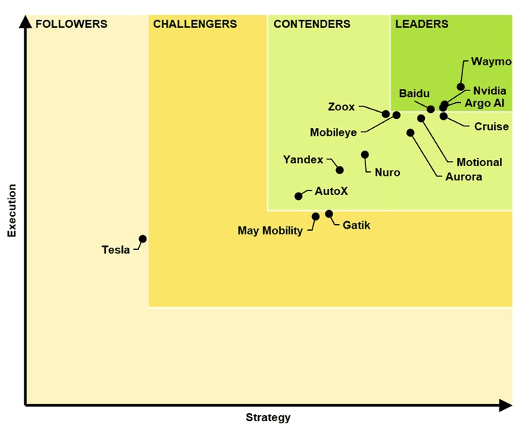

FSD Continues to Overpromise & Underdeliver. Full-self driving (FSD) has been consistently plagued by issues that, unfortunately, have deadly consequences. Industry research provider Guidehouse Insights ranks Tesla last in its 2021 ranking of Automated Driver Systems (ADS), and states flatly, “Tesla needs a thorough rethink of its approach to developing ADS. It has overpromised with its marketing for nearly 5 years and severely underdelivered.”

Per Figure 7, Tesla lags the competition by quite a large margin, as it’s the only company that falls into the "Followers" category.

The most recent problems with Tesla’s FSD version 10.3 forced the company to roll back the update as users reported false crash warnings and other problems with autosteer and cruise control. These issues resulted in Tesla recalling nearly 12,000 vehicles because “a communication error may cause a false forward-collision warning or unexpected activation of the emergency brakes,” according to the National Highway Traffic Safety Administration (NHTSA).

While the roll out of an updated 10.3.1 has restarted, Tesla’s haphazard approach to deploying FSD remains unsettling and led Guidehouse Insights to note, “Tesla’s approach to testing its system is fundamentally at odds with virtually every other company in this industry.”

Figure 7: Tesla Ranks Last Amongst Automated Driver Systems

Sources: Guidehouse Insights

Alphabet’s Waymo routinely ranks as the best automated driving system. Importantly, many of the firms ranked ahead of Tesla are focused solely on building automated driving systems and are not distracted by scaling up automobile production, delivery logistics, and the general day-to-day operations of producing cars. Even so, other direct competitors such as GM Super Cruise also get better scores from third-party organizations.

Increased Regulatory Risk. While Tesla has mysteriously avoided regulatory crackdown on its sales of FSD and practice of beta testing software on live drivers and roads, renewed requests from the NHTSA/National Transportation Safety Board (NTSB) signal that Tesla might be held accountable for practices that many find highly misleading and dangerous to citizens.

Missy Cummings, recently appointed as senior advisor for safety at the NHTSA, has expressed concerns about Tesla’s FSD in the past, tweeting as far back as 2019 that Tesla’s “autopilot easily cause mode confusion, is unreliable and unsafe” and that “NHTSA should require Tesla turn it off.”

More recently, Tesla requested “confidential business information treatment” on its responses to a litany of information requests the NHTSA made as part of its investigation into FSD. If approved, the public would likely never see Tesla’s responses to key questions pertaining to Tesla not issuing a recall for Autopilot after multiple accidents involving parked emergency vehicles, the selection criteria for Tesla’s FSD beta testing program, and the non-disclosure agreements Tesla was making drivers sign before they could use the beta system.

The NHTSA is not alone in criticizing Tesla and its FSD rollout. On October 26, 2021, the head of the U.S. NTSB, Jennifer Homendy, said that Tesla has not yet officially responded to the NTSB regarding its safety recommendations while calling the use of full self-driving ”misleading.” She stated, “my biggest concern is that Tesla is rolling out full self-driving technology in beta on city streets with untrained drivers and they have not addressed our recommendations that we’ve issued as a result of numerous investigations of Tesla crashes.”

Battery Technologies Are Nothing Special. Tesla announced it will be switching to a lithium iron phosphate (LFP) battery in all standard range cars. These batteries are already being used in vehicles built in the Shanghai factory, and this switch is expected to bring down costs. The timing of this change comes as other battery producers, in partnership with incumbent auto manufacturers, are ramping up production, which should drive down battery costs for all EV makers. In other words, the competitive advantages of a cheaper battery may be short-lived, as incumbents build economies of scale in their own supply chain in the coming years.

Additionally, while the much heralded 4680 cylindrical battery, produced by Panasonic for Tesla, and nearly ready for production, should bring a higher energy density in a more efficient package, competitors’ offerings all aim to provide the same.

General Motor’s Ultium platform will enable up to 400-450 miles of range, and the firm is building a new battery research facility aimed at building batteries capable of 600 miles on a single charge. General Motors recently announced a joint venture with LG Chem to build a second U.S. battery cell plant, which is expected to have an annual capacity of 35 gigawatt hours, or slightly above the 30 gigawatt hour capacity of its first Lordstown battery plant. Morgan Stanley analyst Adam Jonas noted that the “formation of Ultium/Ultium Cells LLC will prove to be a critical point of strategic differentiation that will ultimately drive value creation for [GM] shareholders.”

Ford’s Mustang Mach-E became the first electric SUV not made by Tesla to reach an EPA-rated range of up to 300 miles, and the company recently entered a partnership with SK Innovation to build three U.S.-based battery plants to power 1 million EVs annually.

On its own, LG Chem plans to expand its existing U.S. facilities and build two more plants that will produce both pouch cells used by General Motors, Ford, Jaguar, Audi, Porsche, and more, as well as the cylindrical cells used by Tesla.

Ultimately, the race for the “perfect” battery is less important than the race to procure battery supplies to build the number of EVs each manufacturer aims to produce in the coming years. The incumbents have proven they can maintain and win a race to procure supplies, and they’ve only been doing it for multiple decades now.

Not All Supply Issues Can Be Coded Away. To its credit, Tesla managed the global chip shortage relatively well by re-writing software to allow the use of alternative chips. However, not all supply issues can be solved via software, as evidenced by the growing wait times for Tesla’s vehicles. As Electrek notes, Tesla recently updated its delivery timelines for new orders, and depending upon specs, some vehicles won’t be delivered until September 2022 if ordered today. New orders for the Model 3 Standard Range Plus, which is Tesla’s cheapest vehicle, are currently on pace to be delivered in May 2022, or seven months from now.

While certainly not unique to Tesla, extended delivery/wait times give consumers ample time to comparison shop and possibly switch orders to a competitor’s EV that would be available sooner.

Delivery delays aren’t exclusive to in-production vehicles, but Tesla’s future vehicles as well. The much-hyped Cybertruck has recently been delayed again, this time until at least 2023 (compared to an original late 2021 release), which ultimately gives competitors more time to establish a presence in the EV truck market. We recently outlined the many competitors in the EV truck market in our report on Rivian.

Putting It All Together: Tesla Provides Poor Risk/Reward

Given the challenges ahead for Tesla, coupled with a valuation that implies it will take 60%+ of the global EV market share, we think it is clear: Tesla’s stock offers poor risk/reward.

Tesla has proven risky to short, but investors need not buy shares today at such an elevated price.

If you’re buying Tesla at its current valuation, you’re not only betting that it will be the only winner of the electrification of the global automotive fleet, but that it will somehow be twice as profitable as Toyota and achieve at least 60% market share. With anything less than total market domination, TSLA presents large downside risk.

This article originally published on November 2, 2021.

Disclosure: David Trainer, Kyle Guske II, and Matt Shuler receive no compensation to write about any specific stock, sector, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] Assuming sales equal to 2019 (pre-pandemic) levels.

[2] Calculated as 70% of Fiat Chrysler and Groupe PSA’s 2019 European vehicle sales and 40% of Fiat Chrysler and Groupe PSA’s 2019 North American vehicle sales. Stellantis was formed as a merger between the two in early 2021.

3 replies to "$1 Trillion of Speculation"

Why is FSLEX attractive by your estimation and Tesla is its second biggest holding?

Thanks for the question. Our ETF and mutual fund ratings are based on our Portfolio Management Rating and total annual costs. While Tesla does comprise 8% of the fund’s holdings, after evaluating all of FSLEXs holdings, we find that 72% of the fund’s assets are allocated to Netural-or-better rated stocks which contributes to its overall Very Attractive rating.

Thank you for the analysis. Tesla reminds me of Qualcomm in 1999. That bubble was largely fueled by its 2:1 stock split in May and then a 4:1 stock split in December. Analysts kept cranking up their price targets along the way. 20 years later Qualcomm investors broke even. It just goes to show that you can have the right thesis on the future, but you’ve got to get the price right too.