In addition to my stock-brawl interview on Thursday (9/29/11), I have commented to the media on Starbucks (SBUX) many times. Below is a list (with links) to my past opinions/comments on SBUX.

Most of my research and publishing tends to focus on companies manipulating accounting rules to make their reported earnings look better than the real economic cash flows of their business.

It is unfortunately rare that I find a company whose economic earnings are outpacing the reported accounting results and whose stock is cheap.

One such company is Lam Research (LRCX – very attractive rating). One of September’s most attractive stocks, LRCX offers investors hidden value.

Here is a free copy of our report on GE for Ask Matt readers. This report provides details behind Matt’s analysis of GE in his recent article in USA Today. Click here for our report: General Electric (GE) Neutral Risk/Reward Rating.

MarketWatch's Chuck Jaffe feature's New Constructs mutual fund rating system, which has a "neutral" rating on the Magellan fund.

Our fund rating system is the same as our stock rating system, which has received many accolades for its predictive power.

It is only a matter of time before oil and gas stocks stop moving with the price of oil and start reflecting their underlying economics.

When this happens, Baker Hughes (BHI – “very dangerous” rating) will be among the stocks that fall the hardest.

I do not think so. The question, however, is not so much about what directors ignore. You cannot ignore something about which you are unaware.

The real issue is that most directors and investors are simply unaware of the many one-time items because they are buried deep in the annals of footnotes in annual reports or 10-K filings.

I take great pleasure in recommending investors buy Clorox (CLX) – an attractive-rated stock, not just because of its strong profitability and cheap valuation but also because of the unusually high quality and integrity of its financial reporting.

Great interview this am with Dagan McDowell and Ashley Webster about my recent article: "The Fed’s Bazooka: Revealed As Final Policy Firepower in Jackson Hole".

Too much of the rhetoric surrounding S&P’s downgrade of US debt misses the largest and most important point made by S&P’s bold move: the U.S. financial situation is very bad and getting worse with no reconciliation in sight.

It is difficult to deny the poor credit quality of an entity that grossly overspends its revenues, has a mountain of debt (most of which matures within the next few years) and has taken no meaningful steps toward remedying the situation?

By quibbling over S&P’s procedures and calculations, the Treasury and White House reveal that they have no solid rationale for disagreeing with the downgrade.

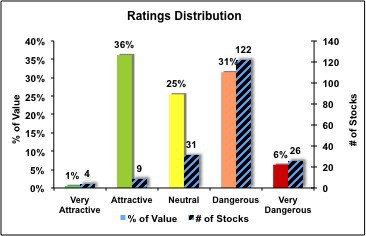

The financial sector is one of four sectors to earn our “dangerous” rating and is the worst-ranked sector in the our 3Q11 Sector Roadmap report according to my methodology at New Constructs.

Here is a free copy of our report on RIMM for readers of Ask Matt.

The valuation of RIMM's stock implies the company's after-tax cash flow (NOPAT) will permanently decline by nearly 75%.

The paramount innovation in the Federal Reserve’s statement yesterday was that it will keep interest rates low until at least the middle of 2013.

Did anyone really expect the Fed to announce it would raise rates anytime in the near future?

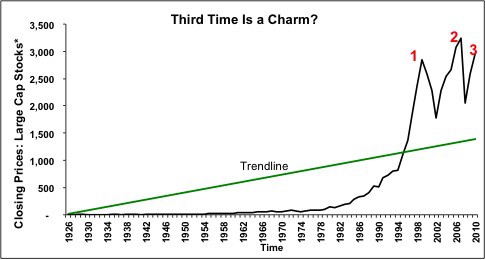

The market decline experienced thus far is closer to its beginning rather then its end. Today’s refreshing market rise is likely just a flash in the pan.

The market needs to go down again before it can sustain any future rise.

I recommend investors avoid all energy sector ETFs. There are no ETFs in the energy sector with an attractive-or-better rating from my methodology at New Constructs. None of the ETFs rank better than the S&P500.

Investors should sell all dangerous-rated energy sector ETFs. The five ETFs below are the worst-rated of all energy sector ETFs:

In Barron's 1st Half of 2011 Survey: “Stumbling To the Halfway Mark”, performance of our Most Attractive stocks won the #2 ranking over the prior 3 years.

The valuation of MCD'’s stock implies the company will grow its after-tax cash flow (NOPAT) by less than 10% over its remaining life. I think market expectations are too low, especially when the company’s return on invested capital (ROIC) is so high at 14.5%.

We recommend investors avoid all utility sector ETFs. There are no ETFs in the utility sector with an attractive-or-better rating. None of the ETFs rank better than the S&P500.

Investors should sell the following dangerous-rated utility sector ETFs:

The consumer staples and information technology sectors are tops among the ten major sectors. Both get our “attractive” rating. Our Sector Roadmap report ranks and rates all of the 10 sectors. It also benchmarks all sectors against the S&P 500, which gets our “neutral” rating and the Russell 2000, which gets our “dangerous” rating.