I have a pair trade (i.e. long/short) ETF strategy for investors who want to maximize upside potential and minimize downside risk in Technology stocks.

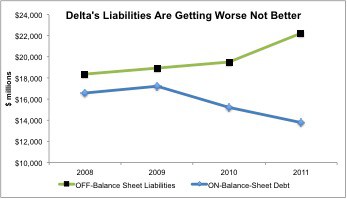

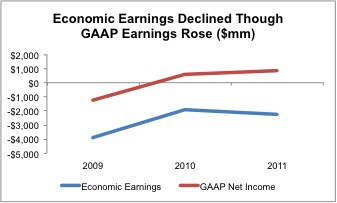

I do not think S&P's analysts are aware of Delta's staggering $22.3 billion in off-balance sheet liabilities, which include $14.1 billion in underfunded pensions and $8.2 in operating leases.

I recommend investors avoid Delta Airlines (DAL). I think the stock could see significant downward pressure as more investors realize how the company is propping up its earnings with relatively aggressive accounting for its pension and postretirement plan (“pensions”), which are already seriously underfunded.

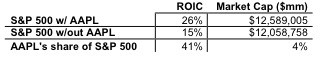

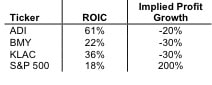

With so much written about Apple (AAPL), I am amazed that so few have focused on the most important driver of its stock price: the company 270% return on invested capital (ROIC).

MSFT gets my best rating because the company’s ROIC, at 72%, ranks 8th in the S&P 500 while its stock price (~$31.52/share) implies the company’s profits will permanently decline by about 20%. High profitability and low valuation create excellent risk/reward in a stock. Here is my free report on MSFT.

Be wary of advice from the bandwagon riders. They care more about getting more people in the bandwagon than anything else.

The Starbucks (SBUX) bandwagon is a big one. I am not on it.

Always flattered when a journalist, especially one as famous and respected at Mr. Taibbi, references my work. His article "Bank of America In Trouble?" incorporated the meat of my "Raising Fees Is A Desperate Measure: Sell BAC" article.

Year to date, Bank Of America (BAC) stock is up nearly 45% compared to the S&P at +about 8%. BAC stock has bounced back nicely after dropping precipitously at the end of last year.

I would call the 45% bounce a “dead cat” bounce because I expect the stock to fall right back to $5/share, where it bottomed last Thanksgiving, or lower.

Recent news that Bank Of America (BAC) is considering jacking up its fees on basic checking accounts suggests the company is bad shape. As I wrote yesterday, I believe BAC stock is headed back to its lows and today’s news confirms my view that the expectations basked into the stock’s valuation are writing checks that the company cannot cash.

As discussed in “The Real Earnings Season Starts Now”, annual reports are the best source for developing investment ideas. I provided my clients with dozens of insights in 2011 that delivered impressive returns, and I continue that trend with my recommendation of MO.

In an increasingly challenging market, Intel [s: INTC] is one of the safest investments with compelling upside potential. That’s right, investors get to have their cake and eat it too – at least for now.

Not everyone has the luxury of or stomach for being net short as I recommended in my last article.

So, I offer some of my top picks for those that must be long.