We closed this position on November 20, 2018. A copy of the associated Position Update report is here.

Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life and Marketwatch.com

Despite what management or Wall Street says, 1+1 does not equal 3 for most mergers. Newell Rubbermaid’s (NWL: $44/share) recently announced intention to acquire Jarden Corporation (JAH: $56/share) is a perfect example of 1+1 < 2. The acquisition between two companies previously in the Danger Zone is in the Danger Zone this week.

Low Quality Business #1: Newell Rubbermaid

Newell’s business has been, at best, stagnant over the past decade. Revenues have steadily declined by 2% compounded annually since 2004 while after-tax profit (NOPAT) has stagnated since 2007. Those who believe the acquisition of JAH will fix Newell’s business are ignoring its history of failed acquisitions.

Since 2000, the company has acquired Paper Mate, Liquid Paper, Irwin Tools, DYMO Labeling, Elmer’s Glue and more. However, these acquisitions have hurt profitability not helped it. Newell’s current return on invested capital (ROIC) of 5% is the same return earned in 2000. Worse yet, Newell’s economic earnings, the true cash flows available to equity investors, have been negative throughout the company’s history.

If Newell hopes to turn things around through acquisition, it needs to acquire a high quality, profitable firm at an inexpensive price, neither of which describes the acquisition of Jarden.

Low Quality Business #2: Jarden Corporation

Jarden Corporation has a similar business model to Newell though it has been even more aggressive in its attempt to grow by acquisition, which has been highly destructive to shareholder value. Despite growing revenues by 26% compounded annually over the past decade, Jarden’s economic earnings have declined from -$27 million in 2004 to -$298 million over the trailing twelve months (TTM). Since 2002, Jarden has diluted shareholders to the tune of a 24% compounded annual increase in shares outstanding. At the same time, the company’s debt has risen 30% compounded annually. If Jarden were making as much money as it claims, why is it constantly raising additional capital that dilutes equity investors?

How Newell And Jarden Create The Illusion Of Profitability

How do NWL and JAH claim to be highly profitable despite the evidence above? The answer lies in the non-GAAP numbers both companies invent to create the illusion of profitability. See Figure 1 and Figure 2.

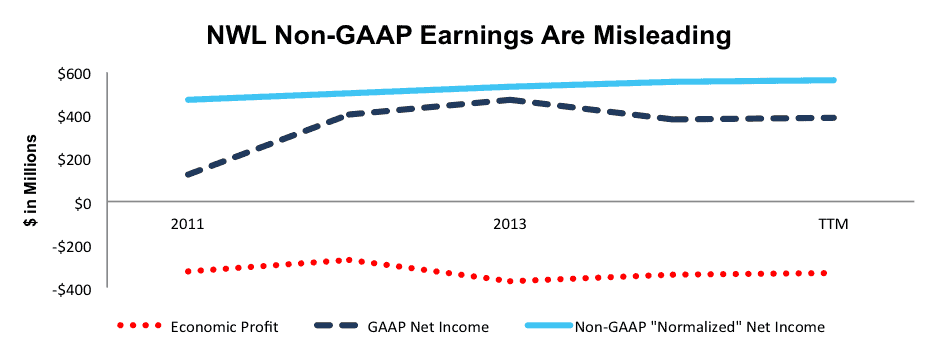

Figure 1: Newell’s Misleading Net Income

Sources: New Constructs, LLC and company filings

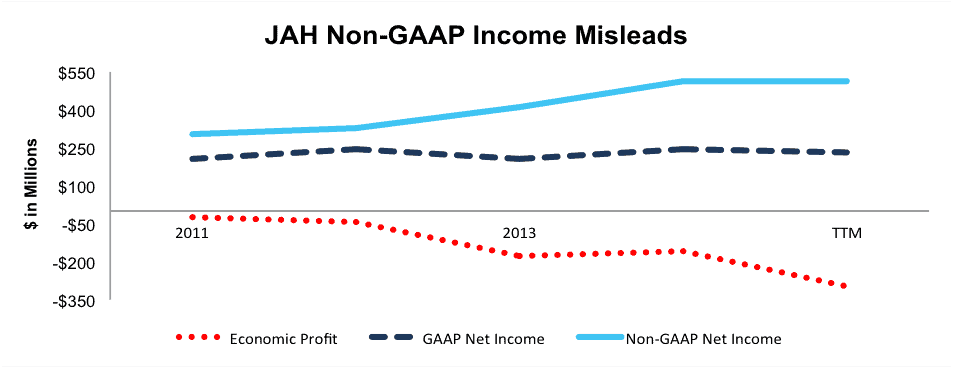

Figure 2: Jarden’s Misleading Net Income

Sources: New Constructs, LLC and company filings

Both Newell and Jarden’s GAAP net income is significantly greater than their economic earnings while non-GAAP net income is, of course, highest and moves attention farthest away from the true cash flows.

Investors Need To Ignore The Non-GAAP Metrics

As is clear, this acquisition involves one value-destroying firm acquiring another that destroys even more value. How can management justify the acquisition? Just look at page 14 of the presentation provided by Newell. The first two “financial implications” of the acquisition are:

- “Strong, competitive core sales growth”

- “Immediately accretive to normalized EPS”

Note the significance of the words “core” and “normalized” as they are simply Newell’s term for non-GAAP, which should quickly raise a red flag. What is removed from sales to reach core sales? Newell removes the effects of foreign currency fluctuations, acquisitions, and completed and planned divestitures. Making these adjustments allowed Newell to report core sales growth of 6% despite only 3% growth in GAAP sales in 3Q15.

Perhaps more alarming are the adjustments Newell makes to reach normalized EPS, as many of the items removed are direct costs of running its business operations. The following are items removed from GAAP net income to calculate normalized EPS:

- Advisory costs

- Personnel costs

- Restructuring costs

- Inventory charges due to currency devaluation

- Acquisition and integration costs

Of course the acquisition will be “immediately accretive to normalized EPS” since normalized EPS removes acquisition costs as well as the numerous costs attributed to Newell’s restructuring projects.

Unfortunately for investors, Newell’s use of non-GAAP is not likely to decrease with the addition of Jarden’s management team as Jarden has long removed restructuring costs, inventory adjustments, acquisition related costs, and foreign currency charges to derive their non-GAAP metric “Segment Earnings.”

What we have here is management exploiting non-GAAP to show growth in metrics that do not account for the cost of growth. Where can I get a deal like that?

Executives Benefit Most From The Acquisition – At The Expense Of Shareholders

We’ve previously raised issues with executive compensation, in general, and specifically at Jarden. It should come as no surprise then that the acquisition of Jarden will significantly benefit executives while shareholders are left with a combined company that has a history of destroying shareholder value.

Under the terms of Newell Rubbermaid’s executive compensation plan, the performance goals executives must meet to earn their bonuses consist of core sales, normalized EPS, and normalized gross margin. Conveniently, two of these items are the top financial implications highlighted in Newell’s presentation of the acquisition. By acquiring Jarden, the new company can show sales growth and EPS growth with no regard to the economics, i.e. the costs, of the acquisition. Another name for this trick is the high-low fallacy.

Big Overpayment As Implied Synergies Are Well Above Excepted Synergies

Not only will executives benefit, but they’re paying an unnecessary premium for Jarden. The only reason for a firm to pay a premium is if they believe there to be attainable synergies. By modeling the impact of the acquisition, we can analyze the implied synergies based upon the market value of Jarden prior to the announcement of the acquisition. In doing so, we find that the implied synergies of the deal are just under $1.6 billion. Meanwhile, Newell has stated they expect only $500 million in cost synergies over four years, and failed to provide any other figures in regards to the “significant revenue synergy opportunities” referenced in the acquisition press release. As we have shown before, large write-downs are directly correlated with big acquisitions that result in goodwill, and the NWL/JAH acquisition fits the bill. Investors must be on the lookout for damaging write-downs occurring in the future.

Even if we assume that management achieves the synergies it claims, which is not likely, they have still overpaid. We think it is clear that this management team is more focused on lining its pockets than investors.

Acquisition Is, Yet Another, Inefficient Use of Capital

Ignoring the overpayment for synergies, we can analyze whether the acquisition is a quality use of capital by calculating the ROIC earned on the deal. In 2014, Jarden earned $579 million in NOPAT, which Newell is paying $13.2 billion to acquire. This deal generates an ROIC of only 4%, which is actually lower than the already poor 5% ROIC Newell earned over the last twelve months. Additionally, the deal’s ROIC is lower than Newell’s 7.4% weighted average cost of capital (WACC). Simply put, the money being spent to acquire Jarden is more costly than the profits it provides.

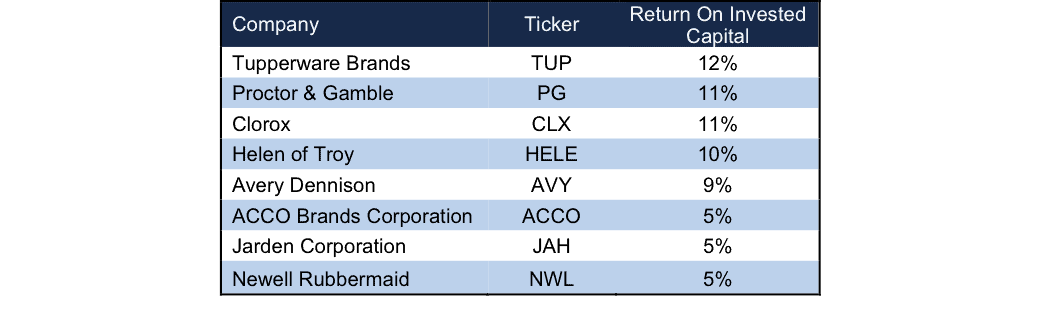

Neither Company Has Better Profitability Than Competition

Separately, Newell and Jarden earn the lowest profitability across their numerous competitors. Combining the two firms, which as shown above does not generate a return above NWL’s current ROIC, simply creates a larger, more cumbersome firm with low profitability.

Figure 3: Competitors Have One Key Advantage

Sources: New Constructs, LLC and company filings

What Should Newell Pay?

As we have done in other Danger Zone reports, we can create a scenario to determine a reasonable price a competitor should pay in an acquisition. In this case, if we assume that upon acquisition, Jarden immediately achieves Newell’s 11% NOPAT margin, the company would still have to grow profits by 25% compounded annually for the next 22 years to justify the acquisition price of $60/share.

A more realistic price Newell should pay for Jarden is $32/share, which is the value of Jarden’s business based on the value of the firm if it achieves Newell’s NOPAT margin in year 1 of the acquisition.

Disclosure: David Trainer and Kyle Guske II receive no compensation to write about any specific stock, style, or theme.

Click here to download a PDF of this report.

Photo Credit: Rubbermaid Products (Flickr)

2 replies to "Danger Zone: Newell Rubbermaid / Jarden Acquisition"

NWL falls nearly 27% after earnings miss and guidance cut.

NWL down ~20% as 4Q18 sales miss expectations. Now down over 60% since the Danger Zone report above while the S&P is up 37%.