We closed this position on March 30, 2020. A copy of the associated Position Update report is here.

Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life and Marketwatch.com

Online retail is widely regarded as the biggest threat to brick-and-mortar stores. What about the threat that online retail is to other online retail? Going up against the likes of Amazon, with its impressive scale and pricing power, has proven difficult for bricks-and-mortar as well as other online retail firms. With negative profitability, rising costs, and an overvalued stock price, Overstock (OSTK: $15/share) is on October’s Most Dangerous Stocks list and is in the Danger Zone this week. Could OSTK be the next victim of the retail market?

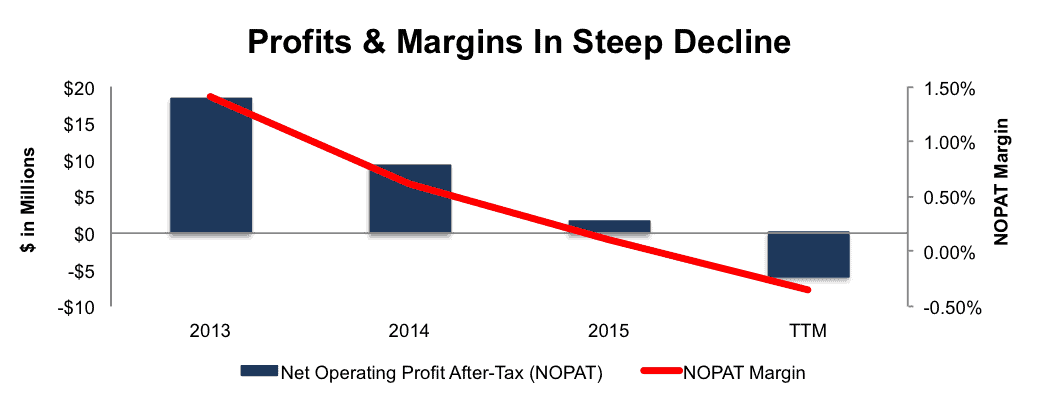

Overstock’s Profits Are On the Decline

Overstock’s after-tax profit (NOPAT) has declined from $18 million in 2013 to $2 million in 2015, and even further, to -$6 million over the last twelve months (TTM). The company’s NOPAT margin has fallen from 1.4% in 2013 to -0.4% TTM, per Figure 1. The deterioration in Overstock’s profitability comes despite revenue growing 13% compounded annually from 2013-2015.

Figure 1: Overstock’s Growing Losses

Sources: New Constructs, LLC and company filings

Overstock’s return on invested capital (ROIC) has fallen from a once impressive 58% in 2013 to a bottom-quintile -4% TTM. It’s clear that Overstock’s business is showing significant signs of deterioration across multiple key metrics.

Compensation Plan Misaligns Executive Interests

Overstock’s executive compensation plan is weighted heavily towards equity incentive awards with a smaller focus on annual cash bonuses. The criteria for earning equity awards appear largely subjective, as Overstock’s proxy statement states that “the number of awards are determined by the compensation committee on the basis of management’s recommendation and the comp committee’s subjective views of the relative ability of key employees to make positive contributions to the company.”

Annual cash bonuses are paid out through a company-wide bonus pool, of which the pool’s total value is determined as a percentage of a “measurement amount.” In 2015, this “measurement amount” was adjusted net income, which removed stock-based compensation, development project expenses, and general & administrative expenses, among others from net income. No bonuses are paid out unless the “measurement amount” exceeds a target level. With significant leeway in the calculation of this “measurement amount,” one must question whether executive interests are correctly aligned with that of shareholder interests.

In either case, executives are incentivized by metrics that do little to create shareholder value and investors should be wary of heavy use of stock price as an incentive. We would much rather see executive compensation tied to ROIC, as there is a clear correlation between ROIC and shareholder value. Currently, OSTK’s executive compensation plan has done little to create shareholder value, as its economic earnings, the true cash flows of the business, have declined from $16 million in 2013 to -$16 million TTM.

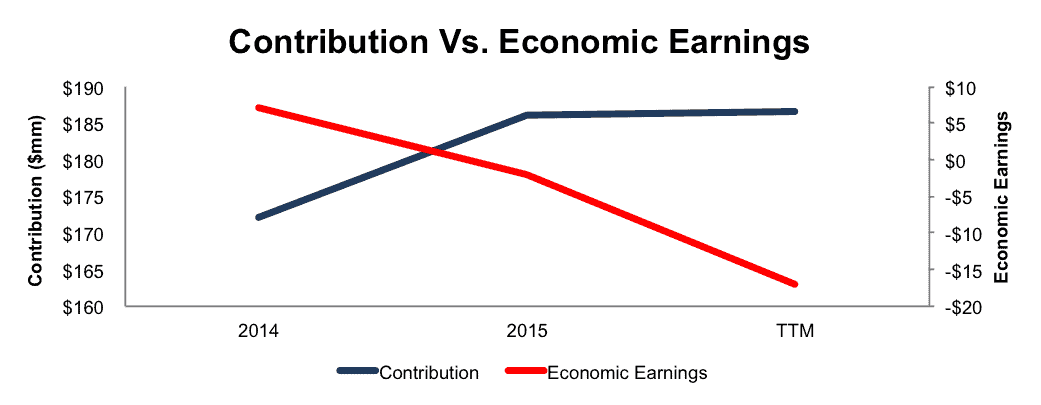

Non-GAAP Metric Ignores Economic Reality

Overstock doesn’t represent the most egregious abuse of non-GAAP metrics we’ve come across in our Danger Zone picks, but its use of “contribution” still distracts from the economic realities of the business. Overstock’s “contribution” is calculated from gross profit and removes the effect of sales and marketing expense and Club O Rewards & gift card breakage. The issue with “contribution” is management claims it provides additional insight into the firm’s operations while it actually diverges significantly from economic earnings. See the dangers of non-GAAP metrics for more details on how companies can abuse non-GAAP.

Per Figure 2, Overstock’s “contribution” has increased from $172 million in 2014 to $187 million over the last twelve months. Meanwhile, economic earnings have declined from $7 million to -$17 million over the same time. Investors following “contribution” would believe Overstock’s business to be in much better condition than those calculating the true cash flows of the business.

Figure 2: Discrepancy Between Non-GAAP & Economic Earnings

Sources: New Constructs, LLC and company filings

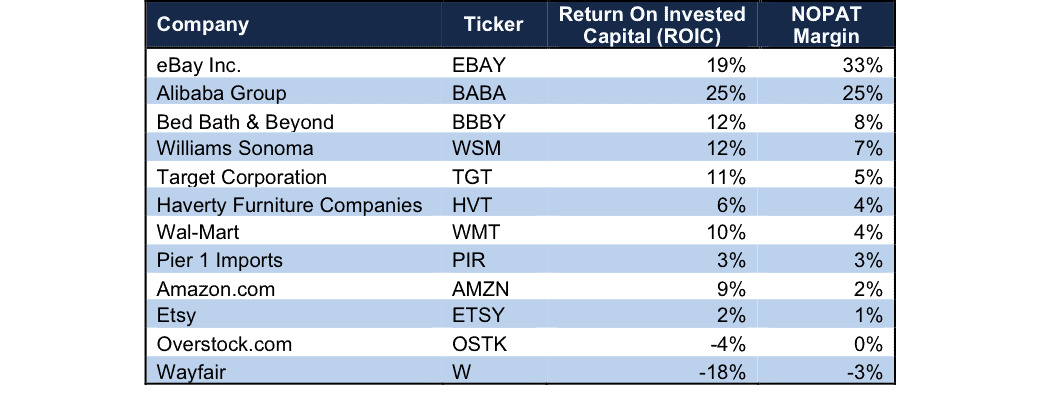

Negative Profitability In The Cutthroat Retail Industry

Overstock’s business, an online retailer of home goods, jewelry, apparel, electronics, and more, places it in one of the most competitive industries in the world. Retailers across the globe compete with one another in terms of product offering, pricing, availability, delivery time, and even ease of use. At the same time, Overstock is not only competing against Internet retailers such as Amazon (AMZN), Etsy (ETSY), Wayfair (W), eBay (EBAY), or Alibaba (BABA), but also thousands of brick-and-mortar stores operating across the country such as Bed Bath & Beyond (BBBY), Wal-Mart (WMT), and Williams-Sonoma (WSM).

Originally, Amazon’s practice of cutting prices to grow market share was believed to be one of the most significant threats to traditional retailers. However, online retailers are just as susceptible to this competition, Overstock included. Per Figure 3, Overstock earns an ROIC and NOPAT margin well below its main Internet and traditional retail competition. In fact, the only company with lower profitability is Wayfair, a previous Danger Zone pick. With negative profitability, Overstock’s ability to compete on price is diminished, and with increased discounting across the sector, the costs to acquire customers are increased, an issue we’ll touch on later.

Figure 3: Overstock’s Profitability Lags Nearly All Competition

Sources: New Constructs, LLC and company filings

Bull Hopes Ignore Deteriorating Economics

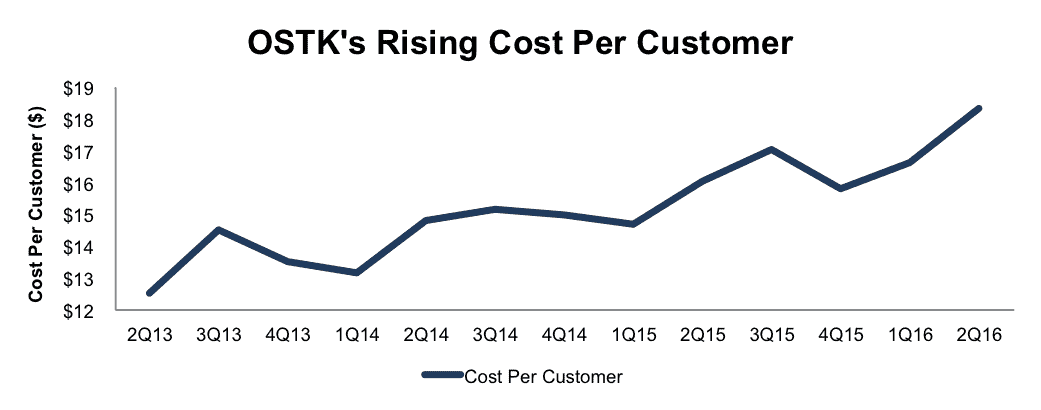

In online retail, the bull case generally centers on a firm’s ability to attract traditionally brick-and-mortar shoppers to its online offering. Retailers can take many approaches to reach this goal, including under pricing the competition, providing a niche offering unavailable elsewhere, or even customer loyalty programs. The problem with many of these approaches is that they can be costly to a retailer’s margins, as noted above, and greatly undermine the firm’s ability to market to new customers while maintaining profitability.

We see this scenario playing out at Overstock, as the firm has increased coupons, sales, and customer rewards programs in an attempt to grow the business. However, the cost per unique customer is continually rising, making each customer worth less to the firm. Per Figure 4, Overstock’s cost per customer has grown from $12.52 in 2Q13 to $18.36 in 2Q16.

Figure 4: Cost Per Customer Threatens Future Profitability

Sources: New Constructs, LLC and company filings

At the same time, the company’s cost of good sold and sales & marketing expenses are growing equal to or faster than the revenue generated by new and existing customers. Since 2011, revenue has grown 9% compounded annually, the same as cost of goods sold. Sales & marketing expenses have grown 15% compounded annually over the same time frame.

Meanwhile, the executive team at Overstock is expanding its interest in side businesses such as blockchain software and bitcoin currency, with claims that it can revolutionize the market and business as a whole. We feel these non-core operations are more of a smokescreen to distract from the growing issues at the business, namely the consistently growing cost to acquire a new customer. Without significant cost controls, the business will be unable to meet the expectations embedded in its stock price.

The largest risk to the bear case is what we call “stupid money risk”, which is higher in today’s low (organic) growth environment. Another firm could step in and acquire OSTK at a value that is much higher than the current market price. However, we only see an acquisition situation possible if an acquiring firm is willing to destroy shareholder value.

Is OSTK Worth Acquiring?

The biggest risk to any bear thesis is that an outside firm acquires OSTK at a value at or above today’s price. If the negative profitability, weak competitive position, and costly customer acquisition noted above are not enough, we’ll show below that OSTK is not an attractive acquisition target unless a buyer is willing to destroy shareholder value.

To begin, OSTK has liabilities of which investors may not be aware that make it more expensive than the accounting numbers suggest.

- $45 million in off-balance-sheet operating leases (12% of market cap)

After adjusting for this liability we can model multiple purchase price scenarios. Even in the most optimistic of scenarios, OSTK is worth no more than the current share price.

Figures 5 and 6 show what we think Wal-Mart should pay for Overstocks to ensure it does not destroy shareholder value. Wal-Mart has a long history of acquiring online retailers in an effort to spur its e-commerce growth, and Overstock could present another target. However, Wal-Mart’s success in these acquisitions is checkered at best, and WMT must not overpay for OSTK or the company will risk investor backlash. Furthermore, there are limits on how much WMT would pay for OSTK to earn a proper return, given the NOPAT of free cash flows being acquired.

Each implied price is based on a ‘goal ROIC’ assuming different levels of revenue growth. In each scenario, the estimated revenue growth rate in year one and two equals the consensus estimate for 2016 (6%) and 2017 (7%). For the subsequent years, we use 7% in scenario one because it represents a continuation of 2017 expectations. We use 10% in scenario two because it assumes a merger with Wal-Mart could create revenue growth through increased advertising efforts and exposure to Wal-Mart’s large customer base.

We conservatively assume that Wal-Mart can grow OSTK’s revenue and NOPAT without spending on working capital or fixed assets. We also assume OSTK achieves a 0.6% NOPAT margin, the average of the past five years. For reference, Overstock’s TTM NOPAT margin is -0.4%, so this assumption implies immediate improvement and allows the creation of a truly best case scenario.

Figure 5: Implied Acquisition Prices For WMT To Achieve 5% ROIC

Sources: New Constructs, LLC and company filings.

Figure 5 shows the ‘goal ROIC’ for WMT as its weighted average cost of capital (WACC) or 5%. Even if Overstock can grow revenue by 9% compounded annually with nearly a 1% NOPAT margin for the next five years, the firm is not worth more than its current price of $15/share. It’s worth noting that any deal that only achieves a 5% ROIC would be only value neutral and not accretive, as the return on the deal would equal WMT’s WACC.

Figure 6: Implied Acquisition Prices For WMT To Achieve 10% ROIC

Sources: New Constructs, LLC and company filings.

Figure 6 shows the next ‘goal ROIC’ of 10%, which is WMT’s current ROIC. Acquisitions completed at these prices would be truly accretive to WMT shareholders. Even in the best-case growth scenario, the most WMT should pay for OSTK is $4.36/share (70% downside). Even assuming this best-case scenario, WMT would destroy $302 million by purchasing OSTK at its current valuation. Any scenario assuming less than 9% CAGR in revenue would result in further capital destruction for WMT.

Standalone Valuation – Priced for Perfection

Despite a rollercoaster ride over the past few years, OSTK is up nearly 20% year-to-date. This significant price increase coupled with the continued deterioration of business fundamentals leaves OSTK significantly overvalued. To justify the current price of $15/share, OSTK must immediately achieve 1.4% pretax margins (highest ever achieved in 2013, compared to -0.6% TTM) and grow NOPAT by 30% compounded annually for the next 12 years. This scenario assumes Overstock can grow revenue by 9% compounded annually, but with the large increase in margins, NOPAT growth significantly outpaces revenue on a compounded annual basis. In this scenario, Overstock would be generating nearly $4.9 billion in revenue (12 years from now), which is greater than Wayfair and Pier 1 Imports last fiscal year revenue combined, and nearly equal to home goods retailer Williams-Sonoma’s 2016 revenue.

Even if we assume OSTK can immediately achieve slightly lower 1% pretax margin and grow NOPAT by 27% compounded annually for the next decade, the stock is only worth $7/share today – a 53% downside. This scenario assumes Overstocks can grow revenue by 7% compounded annually (2017 consensus estimate) but with the increase in margins, NOPAT growth significantly outpaces revenue on a compounded annual basis.

Each of these scenarios also assumes the company is able to grow revenue and NOPAT/free cash flow without spending on working capital or fixed assets. This assumption is unlikely but allows us to create a very optimistic scenario. For reference, Overstock’s invested capital has grown on average $2 million (<1% of 2015 revenue) per year over the last five years.

Market Tires of Overstock’s Lack of Focus

We’ve seen Overstock’s price move upwards of 20% on numerous occasions over the past few years, often in relation to earnings surprises. However, one of the key sticking points recently is Overstock’s lack of focus on its core retail operations. Instead, executives are more interested in non-core operations such as crypto currency (i.e. bitcoin) or blockchain software. These ventures not only cost money, but also take time away from fixing the issues within the retail business. Most recently, OSTK jumped 26% in February when Overstock’s CEO noted the blockchain software could be spun off into its own entity. Clearly investors are excited at the prospects of Overstock focusing solely on its struggling retail operations.

However, with this announcement, Overstock is left in a tough situation. If the software gets spun off, the economics of Overstock’s retail operations do not leave the firm in a position that warrants investment. With fast growing customer acquisition cost, sales & marketing costs, and cost of goods sold, the viability of the business in the retail sector remains in question. If there is no spin off, the focus between managing an online retail firm in a competitive market gets split between the non-core operations, and losses could continue to grow larger.

At the end of the day, without a significant increase in margins, along with impressive revenue growth, Overstock simply cannot meet the expectations baked into its stock price. An earnings miss, particularly in regards to margins, could be all that is needed to send shares to a more rational level as investors wake up to the poor economics of this business.

Insider Action and Short Interest Are Low

Over the past 12 months, 85 thousand insider shares have been purchased and 109 thousand have been sold for a net effect of 24 thousand insider shares sold. These sales represent less than 1% of shares outstanding. Additionally, there are 934 thousand shares sold short, or just under 4% of shares outstanding.

Impact of Footnotes Adjustments and Forensic Accounting

In order to derive the true recurring cash flows, an accurate invested capital, and a real shareholder value, we made the following adjustments to OSTK’s 2015 10-K:

Income Statement: we made $13 million of adjustments with a net effect of removing $1 million in non-operating income (<1% of revenue). We remove $7 million related to non-operating income and $6 million related to non-operating expenses. See all the adjustments made to OSTK’s income statement here.

Balance Sheet: we made $261 million of adjustments to calculate invested capital with a net decrease of $127 million. The most notable adjustment was $64 million (38% of net assets) related to deferred tax assets. See all adjustments to OSTK’s balance sheet here.

Valuation: we made $138 million of adjustments with a net effect of decreasing shareholder value by $40 million. The most notable adjustment was $45 million related to off-balance-sheet operating leases. This adjustment represents 12% of OSTK’s market cap.

Dangerous Funds That Hold OSTK

The following funds receive our Dangerous-or-worse rating and allocate significantly to Overstock.

- Thomson Horstmann & Bryant MicroCap Fund (THBVX) – 1.6% allocation and Dangerous rating.

- BlackRock Disciplined Small Cap Core Fund (BDSAX) – 1.3% allocation and Very Dangerous rating.

- GE Institutional Funds: Small-Cap Equity Fund (GSVIX) – 1.1% allocation and Dangerous rating.

This article originally published here on October 31, 2016.

Disclosure: David Trainer, Kyle Guske II, and Kyle Martone receive no compensation to write about any specific stock, style, or theme.

Scottrade clients get a Free Gold Membership ($588/yr value) as well as 50% discounts and up to 20 free trades ($140 value) for signing up to Platinum, Pro or Unlimited memberships. Login or open your Scottrade account & find us under Quotes & Research/Investor Tools.