We closed this position on September 15, 2021. A copy of the associated Position Update report is here.

Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life and Marketwatch.com

Often times, revenue growth, coupled with non-GAAP income, can mask losses to those not willing to look under the surface. This week’s Danger Zone pick is a company that touts 61 consecutive quarters of revenue growth despite five years of shareholder value destruction. Increased competition, misleading non-GAAP metrics, and an overly optimistic valuation land SPS Commerce (SPSC: $66/share) in the Danger Zone.

Top Line Growth Hides Losses

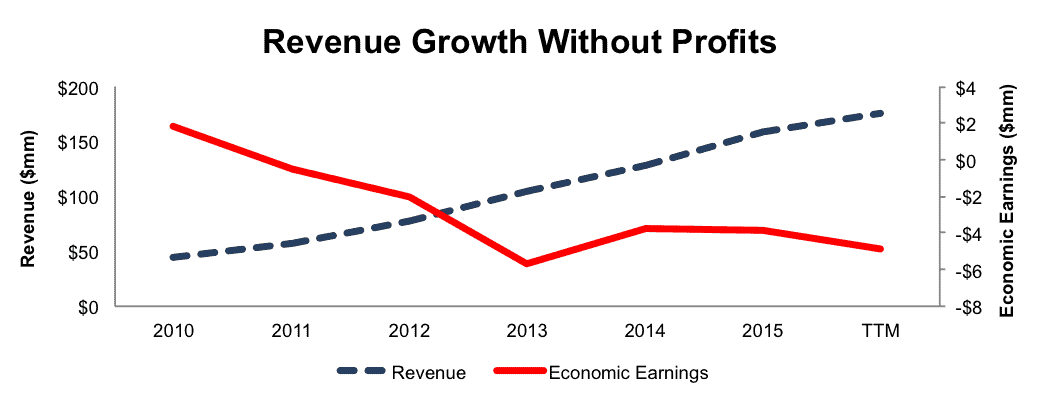

SPS Commerce’s economic earnings, the true cash flows of the business, have declined from $2 million in 2010 to -$4 million in 2015 and -$5 million over the last twelve months (TTM). This decline comes despite revenue growing from $45 million in 2010 to $159 million in 2015, or 29% compounded annually. Figure 1 highlights the contrast between economic earnings and revenue. See a reconciliation of SPS Commerce’s GAAP net income to economic earnings here.

Figure 1: SPSC’s Profitless Revenue Growth

Sources: New Constructs, LLC and company filings

SPS Commerce’s return on invested capital (ROIC) has fallen from 24% in 2010 to a bottom quintile 4% TTM. The company’s after-tax profit (NOPAT) margins more than halved from 7% in 2010 to 3% TTM. Further compounding the poor fundamentals, the company has burned through cumulative $81 million in free cash flow (FCF) since 2011 and FCF sits at -$19 million TTM.

Misaligned Incentives Fuel Shareholder Value Destruction

Executive’s annual bonuses are paid out based upon the achievement of revenue and adjusted EBITDA goals. The compensation committee believes that SPSC’s “financial results are driven most significantly by the revenues we generate.” Unsurprisingly, SPSC has done an impressive job growing revenue and adjusted EBITDA, but not real profits. Adjusted EBITDA, a non-GAAP metric, excludes stock based compensation expense, which represents a significant portion of GAAP results, as we’ll show below. Through the use of either revenue or adjusted EBITDA, executives are incentivized by metrics that do little to create shareholder value, and can actually improve while shareholder value is destroyed. The best way to create shareholder value, and align executives with the best interest of shareholders, is to tie performance bonuses to ROIC.

Non-GAAP Metrics Improve While Economic Earnings Decline

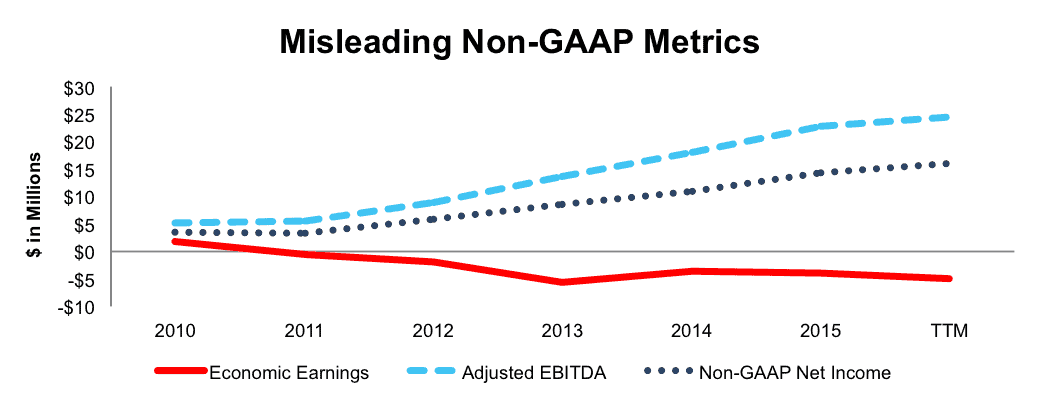

Because businesses have discretion over which items they choose to remove or leave in non-GAAP, these metrics often obfuscate true profits and lack comparability across firms. See dangers of non-GAAP metrics. Here are the expenses SPSC has removed to calculate its adjusted EBITDA and non-GAAP net income:

- Stock based compensation expense

- Amortization of intangible assets

While SPSC may not remove a large number of expenses, the dollar value has a meaningful impact on reported results. In 2015, SPSC removed just over $6 million (138% of GAAP net income) in stock-based compensation to calculate its adjusted EBITDA and non-GAAP net income. In 2014, the company removed just over $5 million in stock-based compensation, which was nearly double GAAP net income. By removing this large expense, SPS Commerce reports non-GAAP metrics that are much better than economic earnings. Adjusted EBITDA grew from $5 million in 2010 to $23 million in 2015, or 34% compounded annually. Non-GAAP net income grew from $4 million in 2010 to $14 million in 2015, or 32% compounded annually. Meanwhile economic earnings declined from $2 million in 2010 to -$4 million in 2015, per Figure 2.

Figure 2: SPS Commerce’s Misleading Non-GAAP Income

Sources: New Constructs, LLC and company filings

Low Profitability In A Competitive Market

The electronic data interchange (EDI) or integration brokerage industry is highly fragmented with many competing services. Two of the most prominent competitors include Sterling Commerce (owned by IBM (IBM)) and GXS (owned by OpenText (OTEX)). At the same time, Hewlett Packard Enterprises (HPE) offers supply chain management software in addition to other providers such as Covalent Works, Edicom, Covisint, DiCentral, and Liaison Technologies.

Per Figure 3, SPS Commerce has a lower NOPAT margin and ROIC than both IBM and OTEX. Such low profitability leaves SPSC with a competitive disadvantage in regards to pricing power. Also, IBM and OTEX’s other profitable business lines not only allow for greater cross-selling, but allow them to pursue only the highest value customers, leaving the less profitable firms for other competitors. Sacrificing margins to boost revenue growth may work in the short-term, but over the long haul, depressed margins leave SPSC vulnerable to competitors who control the “playing-field.”

Figure 3: SPSC’s Profitability Lags Largest Competitors

Sources: New Constructs, LLC and company filings

Bull Hopes Imply Competition Still Lags

Bulls will make the case that SPSC is sacrificing profits to grow its user base and gain market share. Despite strong revenue growth, the first mover advantage SPSC hoped to obtain, by simplifying the traditional on-site EDI services and moving to the cloud, has quickly eroded. Larger competitors have moved into cloud EDI by creating their own products that allow on-premise offerings, cloud offerings, or a mix of both. As these other competing services have come to market, SPSC has seen its margins cut in half. Now, SPSC is facing competition that not only offers a similar, if not more robust, product suite, but does so with more scale, per Figure 4.

Figure 4: Competitor Business Connections/Trade Partners

*Reported prior to being acquired by Open Text in 2014.

Sources: New Constructs, LLC and company filings/press releases

Post acquisition of GXS, Open Text’s CEO noted that the combined platform would connect over 600,000 businesses. Additionally, Di Central notes it processes transactions for over 30,000 organizations worldwide and Edicom is the EDI provider for over 14,000 businesses, including Carrefour and Toys R Us.

The many firms, with robust partner networks and similar offerings, only increase the likelihood of the service becoming commoditized and price being the primary differentiator.

Expense Growth Exceeds Revenue Growth & Puts Valuation In the Cloud

Further casting doubt on SPSC’s ability to meet the expectations baked into its stock price is the firm’s aggressive spending, which continues to prevent revenue growth from translating into profits. Since 2010, while revenue has grown 29% compounded annually, cost of revenue and R&D have grown 32% and 33% compounded annually respectively. Over the same time, sales & marketing and general & administrative costs have grown 27% and 25% compounded annually respectively.

Making matters worse, each year since 2012, the year-over-year (”YoY”) growth in cost of revenues has been faster than YoY revenue growth. At the same time, in three of the past four years, YoY growth in R&D expense has outpaced revenue growth. In order to grow the top line at rates that meet market expectations, SPSC is sacrificing the bottom line and masking that sacrifice behind misleading non-GAAP metrics.

Apart from fundamentals, the valuation of the stock also presents an issue. The current share price implies that SPSC is and will be highly profitable for many years into the future. Given the litany of competition, SPSC’s low profitability, and the spending required to maintain top-line growth, it’s hard to make a case for SPSC meeting the high expectations already baked into the share price.

The largest risk to the bear case is what we call “stupid money risk”, which is higher in today’s low growth (organic) environment. Another firm could step in and acquire SPSC at a value that is much higher than the current market price. However, only in the event a firm is willing to destroy shareholder value is SPSC worth more than its current share price.

Would A Competitor Acquire SPSC?

The biggest risk to our thesis is that an outside firm acquires SPSC at a value at or above today’s price. A chance for acquisition may have passed, as SPSC’s stock price has increased 60% since February. While a firm may have seen SPSC as a deal then, the stock is certainly not a bargain now. If the deterioration of operations is not enough, we’ll show below that SPSC is not an attractive acquisition target unless a buyer is willing to destroy significant shareholder value.

To begin, SPSC has liabilities of which investors may not be aware that make it more expensive than the accounting numbers suggest.

- $21 million in outstanding employee stock options (2% of market cap)

- $13 million in off-balance-sheet operating leases (1% of market cap)

After adjusting for these liabilities we can model multiple purchase price scenarios. Even in the most optimistic of scenarios, SPSC is worth less than the current share price.

Figures 5 and 6 show what we think Oracle (ORCL) should pay for SPSC to ensure it does not destroy shareholder value. Oracle, as a leading software and application provider, has been ramping up its cloud offerings in recent years. At the same time, SPS Commerce can already be integrated with Oracle’s supply chain management application. However, it begs the question whether Oracle receives any additional benefit from taking on SPSC, or if it makes more sense to simply allow integration between the two companies. Regardless, there are limits on how much ORCL would pay for SPSC to earn a proper return, given the NOPAT or free cash flows being acquired.

Each implied price is based on a ‘goal ROIC’ assuming different levels of revenue growth. In each scenario, the estimated revenue growth rate in year one equals the consensus estimate for 2016 (22%). For the subsequent years, we use 22% in scenario one because it represents a continuation of 2016 expectations. We use 28% in scenario two because it assumes a merger with Oracle could create additional cross-selling opportunities.

We conservatively assume that Oracle can grow SPSC’s revenue and NOPAT without spending on working capital or fixed assets. We also assume SPSC achieves an 11.6% NOPAT margin, which is the average positive NOPAT margin of the 47 Software Application companies under coverage and well above 7%, which is the highest margin ever achieved by SPSC in 2010. For reference, SPSC’s TTM NOPAT margin is 3%, so this assumption implies drastic and immediate improvement and allows the creation of a truly best case scenario.

Figure 5: Implied Acquisition Prices For ORCL To Achieve 7% ROIC

Sources: New Constructs, LLC and company filings.

Figure 5 shows the ‘goal ROIC’ for ORCL as its weighted average cost of capital (WACC) or 7%. Even if SPS Commerce can grow revenue by 27% compounded annually with a nearly 12% NOPAT margin for the next five years, the firm is not worth more than its current price of $66/share. Assuming the 27% scenario is a best-case view, Oracle would destroy over $50 million by purchasing SPSC at its current valuation. It’s also worth noting that any deal that only achieves a 7% ROIC would be only value neutral and not accretive, as the return on the deal would equal ORCL’s WACC. We’ve previously covered how Oracle could increase its value by $65 billion simply by focusing on ROIC. Undergoing value neutral deals such as the above would run counter to this analysis.

Figure 6: Implied Acquisition Prices For ORCL To Achieve 23% ROIC

Sources: New Constructs, LLC and company filings.

Figure 6 shows the next ‘goal ROIC’ of 23%, which is ORCL’s current ROIC. Acquisitions completed at these prices would be truly accretive to ORCL shareholders. Even in the best-case growth scenario, the most ORCL should pay for SPSC is $21/share (68% downside). Even assuming this best-case scenario, Oracle would destroy $675 million by purchasing SPSC at its current valuation. Any scenario below 27% CAGR would result in further capital destruction. Furthermore, any deal above $21/share would lower ORCL’s ROIC, thereby destroying shareholder value.

On It’s Own, Valuation Implies Significant Profit Growth

SPSC is up over 60% from its February lows and over 200% over the past five years. Such price appreciation has come without any improvement in the fundamentals of the business, which leaves shares greatly overvalued. To justify the current price of $66/share, SPSC must achieve 7% NOPAT margins (highest ever achieved in 2010, compared to 3% TTM) and grow NOPAT by 34% compounded annually for the next 11 years. This scenario assumes SPSC can grow revenue by 25% each year, above consensus estimates, which further highlights the lofty expectations embedded in the stock price. Because of the large jump in NOPAT margin, NOPAT growth outpaces revenue growth on a compounded annual basis.

Also in this scenario, SPSC would be generating nearly $2 billion in revenue 11 years from now, which is half the estimated total addressable market. Essentially, the expectations already baked into SPSC imply the firm taking nearly 50% market share while its margins currently lag the competition.

Even if we assume SPSC can achieve that 7% NOPAT margin and grow NOPAT by 29% compounded annually for the next decade, the stock is only worth $39/share today – a 41% downside. This scenario assumes SPSC can grow revenue at consensus rates in EY1 and EY2 and that the EY2 estimate continues indefinitely. Once again, because of the improvement in NOPAT margin, NOPAT growth outpaces revenue growth.

Each of these scenarios also assumes the company is able to grow revenue and NOPAT without spending on working capital or fixed assets, an assumption that is unlikely, but allows us to create a very optimistic scenario. For reference, SPSC’s invested capital has grown on average $19 million yearly (12% of 2015 revenue) over the past five years.

Catalyst: SPSC’s Revenue Can’t Mask Losses Forever

The market is filled with cloud companies operating on the cutting edge of numerous industries. We covered a few of them above, and others have been in the Danger Zone before. One of the common trends with such companies is the market is only willing to overlook losses for so long. Non-GAAP metrics can take the focus off losses in the interim, but ultimately, the market allocates capital to those firms that create shareholder value.

As competition grows and is able to further penetrate the market, with higher margins and increased resources, SPSC may see its revenue growth curtailed. In this case, the revenue growth that the market has hung its hat on will no longer exist to prop up shares, and investors could be in for a rude awakening. We’ve previously seen the stock fall 40%, in the first week’s of February, only to rebound over the next six months. Considering the profit growth expectations already baked into SPSC, any lapse in top line growth or margin erosion could cause a repeat of early February.

Adding uncertainty to SPSC’S continued revenue growth is the firm’s heavy reliance on the retail industry. While retailers recognize the importance of an omni-channel presence, they may be unwilling to undergo any investment if the retail landscape were to weaken. Any prolonged decline in consumer spending could lead retailers to forego technology changes until market conditions improved, which could cause a slowdown in SPSC’S revenue growth.

Insider Action and Short Interest Is Low

Over the past 12 months 54 thousand insider shares have been purchased and 107 thousand have been sold for a net effect of 53 thousand insider shares sold. These sales represent <1% of shares outstanding. Additionally, there are 397 thousand shares sold short, or just over 2% of shares outstanding.

Impact of Footnotes Adjustments and Forensic Accounting

In order to derive the true recurring cash flows, an accurate invested capital, and a real shareholder value, we made the following adjustments to SPSC’s 2015 10-K:

Income Statement: we made less than $2 million of adjustments with a net effect of removing less than $1 million in non-operating expenses (<1% of revenue). We removed $1 million related to non-operating expenses and less than $1 million related to non-operating income. See the adjustments made to SPSC’s income statement here.

Balance Sheet: we made $168 million of adjustments to calculate invested capital with a net decrease of $134 million. One notable adjustment was $13 million (6% of net assets) related to off-balance sheet operating leases. See all adjustments to SPSC’s balance sheet here.

Valuation: we made $161 million of adjustments with a net effect of increasing shareholder value by $92 million. The largest adjustment was the addition of $127 million (11% of market cap) due to excess cash. Despite increasing shareholder value, SPSC remains overvalued.

Dangerous Funds That Hold SPSC

The following funds receive our Dangerous-or-worse rating and allocate significantly to SPS Commerce.

- Columbia Acorn Select Fund (LTFAX) – 2.2% allocation and Dangerous rating.

- Geneva Advisors Small Cap Opportunity Fund (GNORX) – 2.2% allocation and Dangerous rating.

- Alger Small Cap Focus Fund (AOFAX) – 2.0% allocation and Very Dangerous rating.

- Alger Small Cap Focus Fund (AOFCX) – 2.0% allocation and Dangerous rating.

This article originally published here on August 29, 2016.

Disclosure: David Trainer and Kyle Guske II receive no compensation to write about any specific stock, style, or theme.

1 Response to "Danger Zone: SPS Commerce (SPSC)"

SPSC falls 18% after 4Q earnings. Now down 19% since Danger Zone report was published while the S&P 500 is up 5% over the same time.