To demonstrate the difference our proprietary Adjusted Fundamental data makes, we continue our series of reports that show how our Credit Ratings are more reliable than legacy firms’ ratings. This report explains how our “Adjusted” EBITDA to Debt ratio is better than the “Traditional” ratio because the Traditional ratio is based on unscrubbed financial data. EBITDA to Debt is one of the 5 ratios that drives our Credit Ratings. Get explanations and comparisons for the other four metrics here.

No Bias, More Coverage, and Better Analytics: A New Paradigm for Credit Ratings

Though legacy providers, e.g. Moody’s, S&P, and Fitch, have dominated the credit ratings industry for some time, our Credit Ratings offer these advantages:

- more coverage: ~2,700 companies vs. ~1,500 for S&P

- more frequent updates: we update all ~2,700 of our credit ratings quarterly while S&P updates ratings for ~400 companies per year

- free of conflicts of interest that continue to taint legacy ratings.

Most importantly, superior fundamental data drives material differences in our Credit Ratings and research compared to legacy firms’ research and ratings. This report will show how EBITDA to Debt ratings for 14% of S&P 500 companies are misleading because they rely on unscrubbed data.

We also detail the differences that better data makes at the aggregate[1], i.e. S&P 500[2], level and the individual company level (see Appendix) so readers can easily quantify the benefits of our superior data.

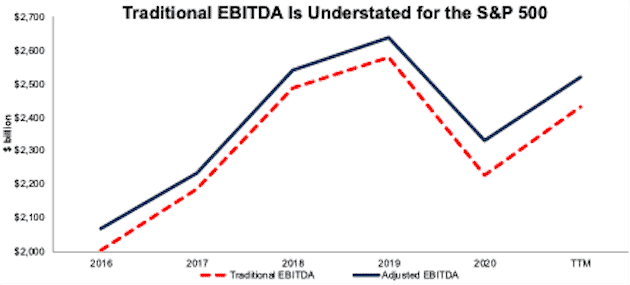

Unscrubbed EBITDA Is Understated for the S&P 500

We use EBITDA as the numerator for the EBITDA to Debt ratio. Figure 1 shows the difference between Traditional EBITDA and our Adjusted EBITDA since 2016. Over the trailing twelve months (TTM), Traditional EBITDA understates our Adjusted EBITDA by -$87 billion, or -4% of Traditional EBITDA.

Figure 1: Traditional Vs. Adjusted EBITDA for S&P 500

Sources: New Constructs, LLC and company filings.

The main drivers of the difference between Traditional and Adjusted EBITDA are hidden unusual gains and losses. Sometimes, these gains and losses cancel out at both the aggregate and individual company level. More often at the individual company level, however, they do not cancel out and Traditional EBITDAs differ greatly from Adjusted EBITDAs. See the Appendix for an example of when they do not cancel out.

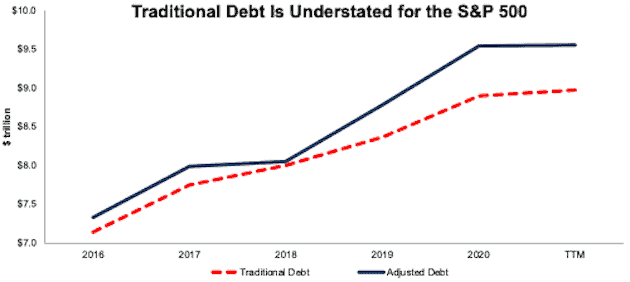

Unscrubbed Total Debt Is Understated for the S&P 500

We use total debt as the denominator for the EBITDA to Debt ratio. Our Adjusted Total Debt provides a more complete view of the fair value of a firm’s total short-term, long-term, and off-balance sheet debt. Over the TTM, Traditional Total Debt is understated by $587 billion, or 7% of Traditional Total Debt.

Figure 2: Traditional Vs. Adjusted Debt for S&P 500

Sources: New Constructs, LLC and company filings.

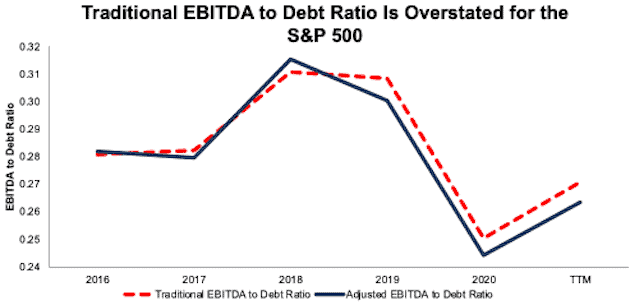

Traditional And Adjusted EBITDA to Debt Ratios Are Similar at the Aggregate Level

At the aggregate level, understated Traditional EBITDA and understated Traditional Total Debt largely offset to provide a Traditional EBITDA to Debt ratio of 0.27 that is slightly higher than the Adjusted EBITDA to Debt ratio of 0.26 over the TTM.

Figure 3: Traditional Vs. Adjusted EBITDA to Debt Ratio for S&P 500

Sources: New Constructs, LLC and company filings.

While the Traditional and Adjusted EBITDA to Debt ratios are similar at the aggregate level, they are not at the individual company level.

Big Differences Emerge at the Individual Company Level

When analyzing individual companies, we see very large differences in Traditional and Adjusted EBITDA, Traditional and Adjusted Total Debt, and Traditional and Adjusted EBITDA to debt ratios.

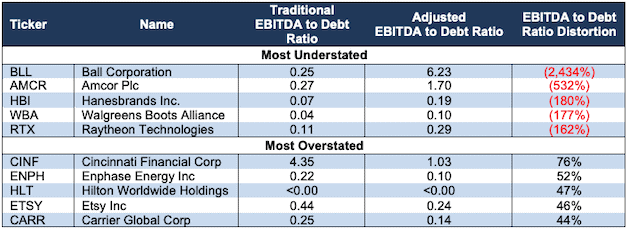

Figure 4 lists ten S&P 500 companies with the most understated and overstated EBITDA to Debt ratios, by EBITDA to Debt Ratio distortion[3], over the TTM.

Note: we detail the data and disclosures that drive the differences in Traditional versus Adjusted EBITDA and Debt for Walgreens Boots Alliance (WBA) in the Appendix to this report.

Figure 4: Companies with Under/Overstated EBITDA to Debt Ratio: TTM

Sources: New Constructs, LLC and company filings.

Ratings Based on Traditional Ratios Are Misleading

Not surprisingly, differences between Traditional and Adjusted ratios drive differences in the Credit Ratings we derive for EBITDA to Debt.

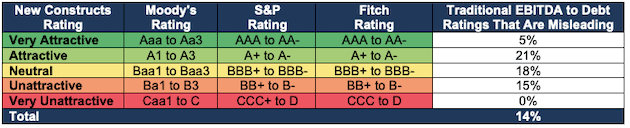

Figure 5 shows how our Credit Ratings align with legacy firms’ ratings systems and the percentage of Traditional EBITDA to Debt ratings that are different from ratings based on Adjusted ratios for companies in the S&P 500. Overall, 14% of the Traditional EBITDA to Debt ratings are different from our Adjusted EBITDA to Debt rating because they rely on unscrubbed data.

As we explain in our Credit Ratings methodology, we set the EBITDA to Debt ratio thresholds so that the distribution of our ratings is comparable to the distribution of ratings for legacy firms. We use the Traditional version of the EBITDA to Debt ratio to set thresholds so that the difference in our ratings comes from the difference in our data.

Figure 5: S&P 500: Percent of Traditional EBITDA to Debt Ratings that Are Misleading

Sources: New Constructs, LLC and company filings.

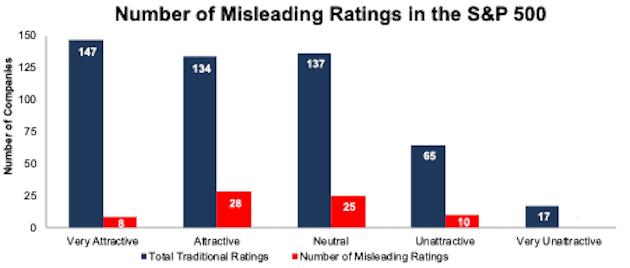

Figure 6 provides more details on the number of companies whose Traditional EBITDA to Debt ratings are different from the rating based on Adjusted EBITDA to Debt ratios.

For example, 28 out of 134 (21%) companies that earn an Attractive EBITDA to Debt rating based on the Traditional ratio earn a different rating based on the Adjusted ratio.

Figure 6: S&P 500: Number of Misleading Traditional EBITDA to Debt Ratings

Sources: New Constructs, LLC and company filings.

We dedicate the Appendix of this report to showing readers exactly how our Adjusted values for EBITDA and total debt are different and better than the unscrubbed versions.

This article originally published on June 24, 2021.

Disclosure: David Trainer, Kyle Guske II, Alex Sword, and Matt Shuler receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

Appendix: Auditing the Differences in Traditional Vs. Adjusted Values

This Appendix will show exactly how our Adjusted values for EBITDA and debt differ from the Traditional versions for Walgreens Boots Alliance.

Walgreens: The Difference in Traditional Vs. Adjusted Values

Figure 7 shows the differences between the two components of the EBITDA to Debt ratio, EBITDA and total debt for Walgreens. The difference between Walgreens’ Traditional EBITDA and Adjusted EBITDA is -$2.8 billion, or -193% of Traditional EBITDA. The difference between Traditional Total Debt and Adjusted Total Debt is -$2.4 billion, or -6% of Traditional Total Debt.

Figure 7: Walgreens: Traditional Vs. Adjusted EBITDA to Debt Components[4]

Sources: New Constructs, LLC and company filings.

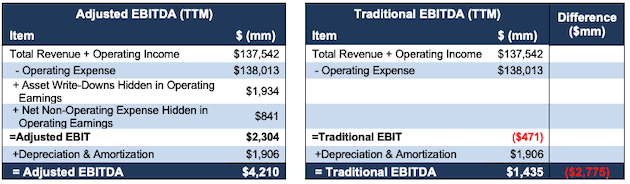

Reconciling Walgreens’ Traditional and Adjusted EBITDA

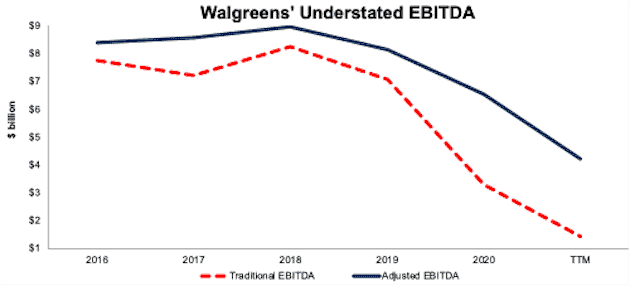

The primary driver of Walgreens understated EBITDA to Debt ratio is understated EBITDA. Figure 8 shows the firm’s Traditional EBITDA has been understated since 2016.

Figure 8: Walgreens: Traditional Vs. Adjusted EBITDA: 2016-TTM

Sources: New Constructs, LLC and company filings.

The differences between Traditional EBITDA and Adjusted EBITDA are driven by non-operating expense(income) hidden in operating earnings. For Walgreens, those differences amount to:

- $1.9 billion in asset write-downs hidden in operating earnings

- $841 million in net non-operating expense hidden in operating earnings.

Figure 9 reconciles Walgreens’ Traditional EBITDA and Adjusted EBITDA and details each of the adjustments listed above.

Figure 9: Walgreens: Adjusted Vs. Traditional EBITDA Detailed Comparison

Sources: New Constructs, LLC and company filings.

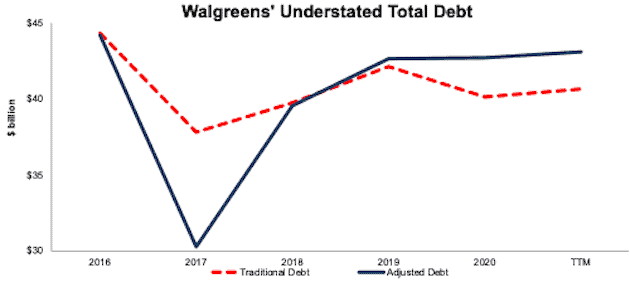

Reconciling Walgreens’ Traditional and Adjusted Total Debt

Figure 10 compares Walgreens’ Traditional Debt and Adjusted Debt since 2016. The difference between non-current operating liabilities and the difference between the fair value of debt and the carrying value of debt explain most Walgreens’ -$2.4 billion in understated Total Debt.

Figure 10: Walgreens: Traditional Vs. Adjusted Total Debt: 2016-TTM

Sources: New Constructs, LLC and company filings.

Figure 11 reconciles Walgreens’ Traditional Total Debt and Adjusted Total Debt and details each of the differences noted above.

Figure 11: Walgreens: Adjusted Vs. Traditional Total Debt Detailed Comparison[5][6]

Sources: New Constructs, LLC and company filings.

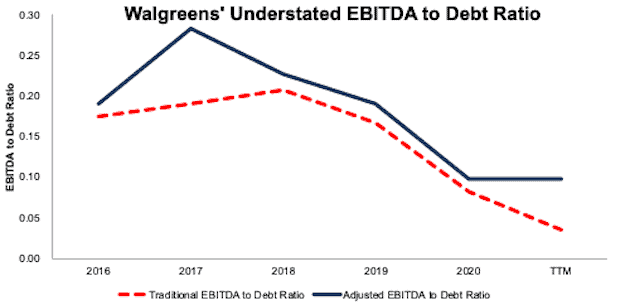

Walgreens’ EBITDA to Debt Ratio Is Understated

With understated Traditional EBITDA and Traditional total debt, Walgreens’ EBITDA to Debt ratio has one of the largest differences between Traditional and Adjusted of all companies in the S&P 500. Per Figure 12, Walgreens’ EBITDA to Debt has been understated since 2016.

Figure 12: Walgreens: Traditional Vs. Adjusted EBITDA to Debt Ratio: 2016-TTM

Sources: New Constructs, LLC and company filings.

[1] We calculate the S&P 500 Traditional and Adjusted EBITDA by aggregating the results for all current members of the S&P 500.

[2] In this analysis, we use the 494 companies for which we have data back to 2016 and are currently in the S&P 500.

[3] EBITDA to Debt Ratio Distortion equals (Traditional EBITDA to Debt ratio - Adjusted EBITDA to Debt ratio) / Traditional EBITDA to Debt ratio.

[4] This number is the EBITDA to Debt Ratio Distortion, which equals (Traditional EBITDA to Debt ratio - Adjusted EBITDA to Debt ratio) / Traditional EBITDA to Debt ratio.

[5] We use a standardized discount rate across all companies under coverage to calculate the Adjusted NPV of Operating Leases to ensure comparability and remove management discretion in calculating operating lease liabilities. Find more details on how we treat operating leases here.

[6] Traditional NPV of Operating Leases equals the operating lease obligation reported in the firm’s 2Q20 10-Q.