Three new stocks make November’s Exec Comp Aligned with ROIC Model Portfolio, available to members as of November 15, 2019.

Recap from October’s Picks

Our Exec Comp Aligned with ROIC Model Portfolio (+3.8%) outperformed the S&P 500 (+3.6%) from October 16, 2019 through November 13, 2019. The best performing stock in the portfolio was up 10%. Overall, nine out of the 15 Exec Comp Aligned with ROIC Stocks outperformed the S&P from October 16, 2019 through November 13, 2019.

Only our research utilizes the superior data and earnings adjustments featured by the HBS & MIT Sloan paper, "Core Earnings: New Data and Evidence.” The success of this Model Portfolio highlights the value of our Robo-Analyst technology[1], which scales our forensic accounting expertise (featured in Barron’s) across thousands of stocks.

This Model Portfolio only includes stocks that earn an Attractive or Very Attractive rating and align executive compensation with improving ROIC. We think this combination provides a uniquely well-screened list of long ideas because return on invested capital (ROIC) is the primary driver of shareholder value creation.[2]

New Stock Feature for November: Cracker Barrel Old Country Store (CBRL: $160/share)

Cracker Barrel (CBRL) is the featured stock in November’s Exec Comp Aligned with ROIC Model Portfolio.

We made CBRL a Long Idea in March 2017 and closed the position in June 2018. However, CBRL’s fundamentals have improved since then, and its stock now looks undervalued.

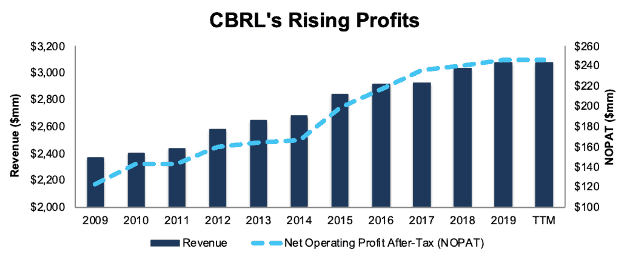

Over the past decade, CBRL has grown revenue by 3% compounded annually and after-tax operating profit (NOPAT) by 7% compounded annually. Profit growth has been driven by NOPAT margin rising from 5% in 2009 to 8% in 2019.

Figure 1: CBRL’s Revenue & NOPAT Since 2009

Sources: New Constructs, LLC and company filings

Executive Compensation Plan Helps Drive Shareholder Value Creation

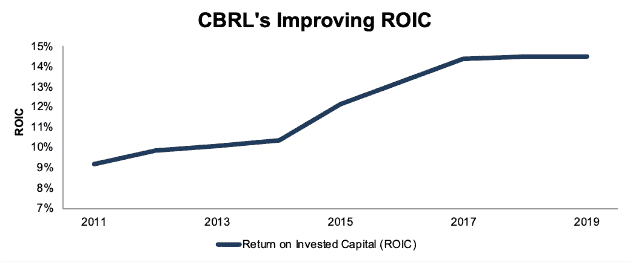

CBRL has included ROIC as a performance metric in its executive compensation plan since 2011. Last year, 50% of CBRL’s long-term incentive program plan was tied to the achievement of a target ROIC.

The focus on return on invested capital helps ensure intelligent capital allocation. CBRL has improved its ROIC from 9% since adding ROIC to its compensation plan in 2011 to 15% in 2019. CBRL’s executive compensation plan lowers the risk of investing in the company’s stock because we know executives’ interests are tied to shareholders’ interests.

Figure 2: CBRL’s ROIC Since 2011

Sources: New Constructs, LLC and company filings

CBRL is Undervalued

At its current price of $160/share, CBRL has a price-to-economic book value (PEBV) ratio of 0.8. This ratio means the market expects CBRL’s NOPAT to permanently decline by 20%. This expectation seems pessimistic given that CBRL has grown NOPAT by 8% compounded annually over the past five years and 7% compounded annually over the past decade.

If CBRL can maintain 2019 NOPAT margins (8%) and grow NOPAT by just 3% compounded annually for the next decade, the stock is worth $253/share today – a 58% upside. See the math behind this reverse DCF scenario.

Critical Details Found in Financial Filings by Our Robo-Analyst Technology

As investors focus more on fundamental research, research automation technology is needed to analyze all the critical financial details in financial filings as shown in the Harvard Business School and MIT Sloan paper, "Core Earnings: New Data and Evidence”.

Below are specifics on the adjustments we make based on Robo-Analyst findings in Cracker Barrel’s 2019 10-K:

Income Statement: we made $77 million of adjustments, with a net effect of removing $23 million in non-operating expense (1% of revenue). You can see all the adjustments made to CBRL’s income statement here.

Balance Sheet: we made $615 million of adjustments to calculate invested capital with a net increase of $497 million. One of the largest adjustments was $460 million due to operating leases. This adjustment represented 39% of reported net assets. You can see all the adjustments made to CBRL’s balance sheet here.

Valuation: we made $904 million of adjustments with a net effect of decreasing shareholder value by $904 million. Apart from total debt, which includes the operating leases noted above, one of the largest adjustments to shareholder value was $44 million in deferred tax liability. This adjustment represents 1% of CBRL’s market cap. See all adjustments to CBRL’s valuation here.

This article originally published on November 21, 2019.

Disclosure: David Trainer, Kyle Guske II, and Sam McBride receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] Harvard Business School features the powerful impact of our research automation technology in the case New Constructs: Disrupting Fundamental Analysis with Robo-Analysts.

[2] This paper compares our analytics on a mega cap company to other major providers. The Appendix details exactly how we stack up.