We closed this position on May 24, 2018. A copy of the associated Position Update report is here.

Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life.

This company operates a niche business that lacks the market breadth, scale and resources to effectively compete against well-established e-commerce giants. The future profit expectations embedded in the stock price exceed what the company can reasonably be expected to achieve. Further, the company’s enterprise value exceeds what a potential buyer could reasonably be expected to pay for the business. Each of these factors create an unbalanced risk/reward trade-off that is not in investors’ favor. Etsy, Inc. (ETSY, $16/share) is this week’s Danger Zone pick.

ETSY Background

Etsy Inc. (ETSY), a global e-commerce platform for handmade artisan goods, was 2015’s worst performing IPO. ETSY priced at $16/share, quickly rose to $31/share, and then dropped sharply to end the year at $8/share. The stock has traded like a “tech start-up” at some points and a “retailer” at others. ETSY has also received a reputation as a playground for profligate Brooklyn bohemians not focused on creating shareholder value.

In May 2017, ETSY changed CEOs and took a hatchet to the workforce. The changes sparked investor optimism that ETSY can boost profitability by reining in expenses without negatively impacting already slowing revenue growth. ETSY has also drawn activist investors, at least one of which intends to push for a sale of the company. Due to these events, rather than fundamentals, ETSY is once again trading near its IPO price.

Growth is Clearly Slowing

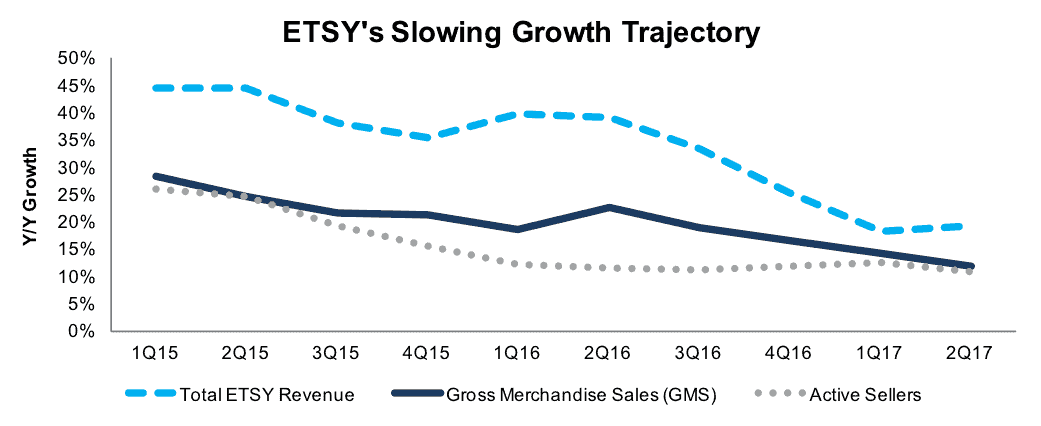

ETSY’s revenue has grown 39% compounded annually since 2013 and grew 33% in 2016. In February 2017, the company guided to 20-22% revenue growth and 15-17% gross merchandise sales (GMS) growth in 2017. In early August, guidance was lowered to 18-20% revenue growth and 12-14% GMS growth.

Per Figure 1, revenue grew 19% and GMS grew 12% in 2Q17 vs. 2Q16. 2Q17 growth was roughly half as strong as the growth experienced in 2Q16, when revenue grew 39% and GMS grew 23% compared to 2Q15. Notably, 2Q16 growth reflected a minimal slowdown compared to the 44% revenue growth and 25% GMS growth experienced in 2Q15 vs. 2Q14.

Figure 1: ETSY’s Growth in Revenue, Merchandise Sales and Active Sellers

Sources: New Constructs, LLC and company filings

Profits Have Been Meager to Date

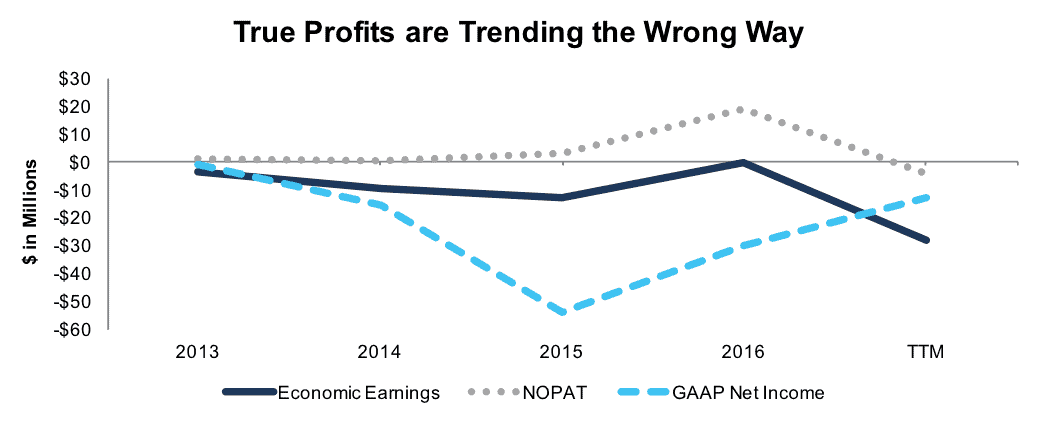

ETSY generated a cumulative $5 million of after-tax profits (NOPAT) from 2013-2015 while earning an average NOPAT margin of 1%. ETSY experienced its most profitable year in 2016 with NOPAT of $19 million. This profit increase was driven by an improvement in NOPAT margin to 5% in 2016 from 1% in 2015.

More recently, this progress has been reversed due to increased competition and lack of expense discipline. Expense growth began accelerating in 2H16, just as the revenue growth slowdown took hold. This expense growth drove a decline in NOPAT margin to -1% and a $4 million operating loss over the trailing twelve months (TTM), per Figure 2.

Figure 2: NOPAT and Economic Profits vs. GAAP Net Income

Sources: New Constructs, LLC and company filings

Further, negative free cash flow (FCF) totaled -$63 million TTM vs. -$43 million for all of 2016. In addition to lower NOPAT, the TTM period includes a 33% increase in invested capital. Since 2013, ETSY has burned a cumulative $213 million of FCF (11% of market cap). The company’s $282 million in cash currently on the books would only support the TTM cash burn rate for another four years.

Poor Return on Invested Capital

ETSY’s return on invested capital (ROIC) has averaged 3% over the past three years, while the current (TTM) ROIC of -2% is in the bottom quintile of our coverage universe. The TTM loss could be short lived due to the new-found focus on profitability. However, for ETSY to earn an adequate ROIC above the cost of capital, the company would need to earn a 7% NOPAT margin on current revenue without growing invested capital.

ETSY has proven to be margin challenged, but balance sheet efficiency and capital turnover are relatively efficient compared to the Consumer Discretionary sector as a whole. ETSY’s ratio of revenue/invested capital, or capital turnover, is 1.6 compared to 0.9 for the Consumer Discretionary sector. This ratio has been trending lower, however, as invested capital growth has outstripped revenue growth over the past few years.

Executive Comp Aligned with Misleading Metrics

We know from numerous case studies that changes in ROIC are directly correlated to changes in market value. Accordingly, we favor compensation plans that use ROIC to measure performance to ensure executives’ interests are aligned with shareholders’ interests. Revenue and non-GAAP performance targets can be an incentive to sacrifice profitability for volume, or worse, engage in acquisitions that destroy shareholder value.

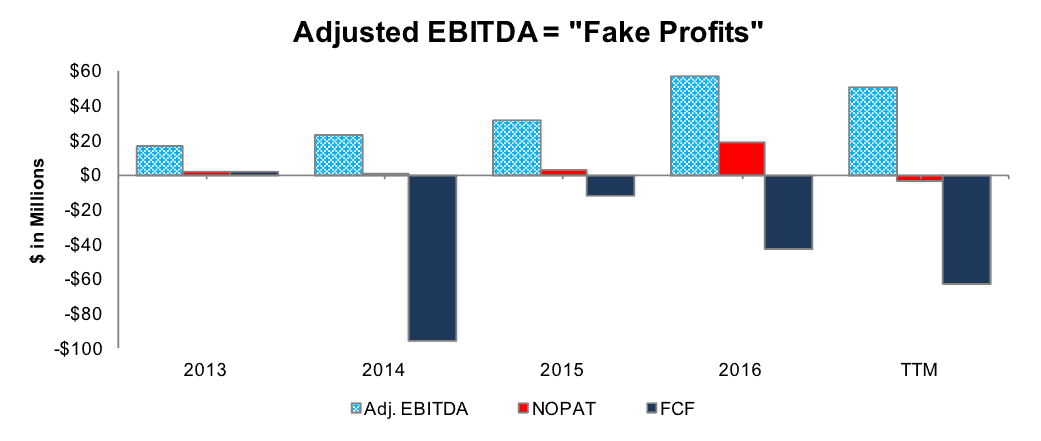

ETSY’s executive compensation is structured as 20% base salary, 20% annual cash incentive and 60% long-term equity incentives. The weighting towards long-term incentives is the mechanism the board uses to align executives’ interests with shareholders. However, the intent is offset by the use of revenue growth and “adjusted EBITDA” targets as the hurdles for short-term, variable incentive comp.

As shown in Figure 3, ETSY has managed to show a generally improving trend in adjusted EBITDA, while achieving no such consistent improvement in true profit measures such as NOPAT or FCF. Further, the company has generated cumulative economic losses of -$54 million since 2013, with the TTM performance being the worst period. Until the company aligns its compensation plans with financial goals that actually constitute profits, we are not optimistic that shareholder value destruction will come to an end on its own.

Figure 3: ETSY’s Misleading Non-GAAP Metrics

Sources: New Constructs, LLC and company filings

Formidable Competition Forces Change

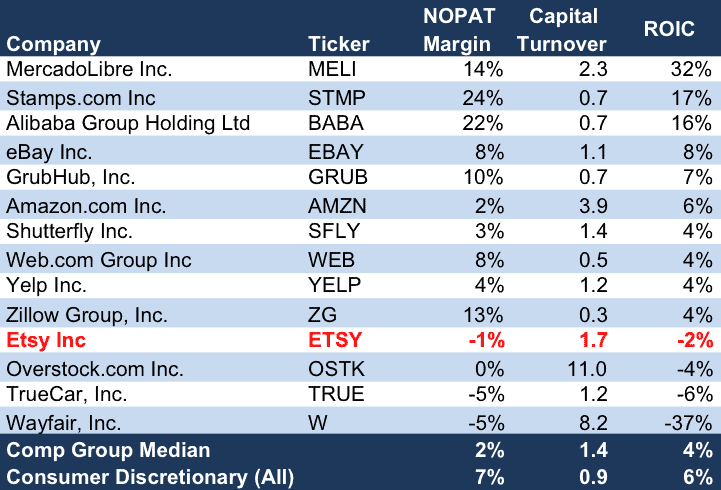

ETSY is the leader in an e-commerce market it largely created, but its first mover advantage is threatened by formidable competition. Ebay (EBAY) and Alibaba (BABA) are the more similar ecommerce platforms, but Amazon (AMZN) is ETSY’s most dangerous competitor. AMZN launched “Handmade at Amazon” in October 2015 in direct competition with ETSY. About a year later, AMZN’s presence began to impact ETSY’s financials.

ETSY reacted by cutting over 20% of the workforce and making $35 million (annualized) of targeted cost reductions the focal point. We also expect the internal shift to cause cultural issues with the employee base. It was just last year that ETSY moved from a 106,000 square foot headquarters into a new two-building, 200,000 square foot headquarters that is reportedly among the most luxurious and celebrated in the world.

An abrupt growth slowdown followed by an expense reduction initiative is a sign that ETSY’s niche platform is not a sustainable competitive advantage in the cutthroat world of e-commerce. This conclusion is supported by ETSY’s poor margins relative to direct competitors and other similar business models. Per Figure 4 above, ETSY’s -1% NOPAT margin (TTM) is well below EBAY, BABA, notoriously low-margin AMZN and a number of other e-commerce platforms that ETSY itself offers up as comps in its proxy statement.

We also find it telling that Michaels (MIK), an arts and crafts retailer with a brick-and-mortar footprint and almost no e-commerce presence, is able to generate results far superior to ETSY. On a TTM basis, MIK has earned a 10% NOPAT margin and 18% ROIC.

Figure 4: Competitive Advantage Not Apparent for ETSY

Sources: New Constructs, LLC and company filings

Countering the Bull Case

Aside from an activist investor forcing a sale at a premium price, the Bull Case for ETSY is based on expectations that the company can maintain a strong revenue growth trajectory while reining in expenses.

Expense initiatives will boost near-term financial performance, but few companies cut their way to prosperity. ETSY’s strategy to offset slowing ‘Marketplace’ segment revenue has been to focus on developing new products in the ‘Seller Services’ segment. Seller Services has already been a major factor for some time, however. Seller Services accounted for 58% of total revenue in 2Q17 vs. 41% for Marketplace. Two years ago, the revenue split was nearly 50/50.

While growth in Seller Services has softened the slowdown in Marketplace growth, it is not sustainable longer term and has already begun to slow. Seller Services revenue grew 25% Y/Y in 2Q17, compared to 58% in 2Q16 and 79% in 2Q15. Ultimately, Seller Services revenue is tied back to growth in GMS and Active Sellers. ETSY can only consume so much of the Active Seller base’s profits from the sale of goods with fees from Seller Services products, no matter how convenient and user-friendly they are.

The current growth trajectory being exhibited in GMS and Active Sellers is not supportive of the consensus outlook for ETSY to generate 18% revenue growth through 2018. Based on the ratio of GMS growth to revenue growth over the past year (1.5), a slowdown in GMS to 8-10% Y/Y implies 12-15% Y/Y revenue growth. Even assuming no slowdown, ETSY is already priced to perfection, as we’ll show below.

High Expectations Embedded in Valuation

ETSY has risen 33% YTD and 14% over the last year to outperform the S&P 500. This performance has occurred despite NOPAT declining over the past few quarters, as well as forward revenue and EPS expectations being lower now than one year ago. This move in the stock has widened the chasm between the company’s current financial performance and the significantly higher profits implied by the stock’s market value.

To justify its current price of $16/share, ETSY must grow NOPAT by 10% compounded annually for over 50 years. This scenario assumes an immediate improvement in NOPAT margin to 10% (from -1% TTM) and compound annual revenue growth of 8%. In this scenario, ETSY would be over twice as large as EBAY with $21 billion of annual revenue. This scenario is not a bet we are inclined to make given the recent slowdown in revenue growth, ETSY’s meager three-year average NOPAT margin of 1.4% and, most importantly, the deteriorating competitive position of the company.

Even if we assume ETSY can grow NOPAT by 25% compounded annually for the next decade, the stock is still worth only $11 today – a 31% downside risk. This scenario assumes ETSY grows revenue to $1.2 billion in ten years from $396 million (TTM), or 12% compounded annually. This scenario also assumes ETSY gradually improves NOPAT margin to 15% over the next five years.

Each of these scenarios also assumes ETSY is able to grow revenue, NOPAT and FCF without increasing working capital or investing in fixed assets. This assumption is unlikely but allows us to create optimistic scenarios that demonstrate just how high expectations embedded in the current valuation really are. For reference, ETSY has increased invested capital from $53 million in 2013 to $260 million TTM, or 57% compounded annually.

Could ETSY Fetch a Premium?

ETSY’s tumultuous run since the IPO has attracted the attention of activist investors such as TPG Capital, Dragoneer and Black-and-White Capital, which has said it would push for a sale. ETSY’s proprietary value is questionable given that the company has yet to develop unique, disruptive technology or generate consistent free cash flow. Bulls may argue for the value in the brand loyalty of its niche customer base. However, we see little value in niche retail customer bases that ultimately can be lured away from a value proposition based on “experience” by a true value proposition based on economics.

The largest risk to any bear thesis is what we call “stupid money risk”, which means an acquirer comes in and pays for ETSY at the current, or higher, share price despite the stock being overvalued. Amazon’s existing presence in the market, via its “Handmade at Amazon” makes an acquisition unlikely. It would make little sense to acquire Etsy given that Amazon already possesses a marketplace platform and distribution centers, which means Etsy’s proprietary value would be its sellers and buyers.

eBay (EBAY) seems to be a better fit, as the two firms could create clear synergies since both operate an individual seller online marketplace. However, as we’ll show below, we see an acquisition as possible only if an acquiring firm is willing to ignore prudent stewardship of capital and destroy substantial shareholder value. We show below how expensive ETSY remains even after assuming an acquirer can achieve significant synergies.

Walking Through the Acquisition Value Math

To begin, Etsy has liabilities of which investors may not be aware that make it more expensive than the accounting numbers suggest.

- $79 million in outstanding employee stock options (4% of market cap)

- $65 million in deferred tax liabilities (3% of market cap)

- $22 million in off-balance-sheet operating leases (1% of market cap)

After adjusting for these liabilities, we can model multiple purchase price scenarios. Even in the most optimistic of scenarios, Etsy is worth less than its current share price.

Figures 5 and 6 show what we think EBAY should pay for ETSY to ensure it does not destroy shareholder value. eBay could immediately boost its slowing revenue growth while integrating Etsy’s marketplace into its larger sales platform. Additionally, Etsy sellers would be introduced to an entirely new market of potential buyers. However, there are limits on how much EBAY would pay for ETSY to earn a proper return, given the NOPAT and free cash flows (or lack thereof) being acquired.

Each implied price is based on a ‘goal ROIC’ assuming different levels of revenue growth. In both scenarios, the estimated revenue growth rate in year one equals 20% and in year two equals 18%, which is the consensus estimate of revenue growth for the next two years. For the subsequent years, we use 18% in scenario one because it represents a continuation of next year’s expectations. We use 23% in scenario two because it assumes a merger with EBAY would create revenue synergies thorough increased exposure on EBay’s larger online marketplace.

We conservatively assume that eBay can grow Etsy’s revenue and NOPAT without spending anything on working capital or fixed assets beyond the original purchase price. We also assume Etsy immediately achieves a 3% NOPAT margin, which is the average of eBay’s and Etsy’s current NOPAT margin. For reference, Etsy’s TTM NOPAT margin is -1%, so this assumption implies immediate improvement and allows the creation of a truly best-case scenario.

Figure 5 Implied Acquisition Prices For EBAY To Achieve 6% ROIC

Sources: New Constructs, LLC and company filings.

Figure 5 shows the ‘goal ROIC’ for EBAY as its weighted average cost of capital (WACC) or 6%. Even if ETSY can grow revenue by 21% compounded annually with a 3% NOPAT margin for the next five years, the firm is worth less than its current price of $16/share. It’s worth noting that any deal that only achieves a 6% ROIC would be only value neutral and not accretive, as the return on the deal would equal EBAY’s WACC.

Figure 6: Implied Acquisition Prices For EBAY To Achieve 8% ROIC

Sources: New Constructs, LLC and company filings.

Figure 6 shows the next ‘goal ROIC’ of 8%, which is eBay’s current ROIC. Acquisitions completed at these prices would be truly accretive to EBAY shareholders. Even in the best-case growth scenario, the most EBAY should pay for ETSY is $4/share (78% downside to current valuation). Even assuming this best-case scenario, EBAY would destroy over $1.2 billion by purchasing ETSY at its current valuation. Any scenario assuming less than 21% compound annual growth in revenue would result in further capital destruction for EBAY.

ETSY Offers No Shareholder Yield

ETSY does not currently pay a cash dividend nor have a buyback program in place. As such, the stock offers none of the downside protection that a solid shareholder yield can provide. Given the level of risk we see in the valuation and forward expectations, this downside protection could be sorely missed.

Insider Trading and Short Interest

Insiders own just 1% of outstanding shares. This strikes us as low for a relatively young company less than three years removed from its IPO, albeit one who has jettisoned its original founder and the subsequent CEO. The new CEO Silverman, who joined Etsy’s board in November, recently bought 64,000 shares at $15.67 per share (just over $1 million) in the open market. Aside from Silverman’s purchase, which was symbolically necessary if not financially prudent, insider activity has been universally on the sell side for the past two years.

Short interest is currently 6.6 million shares, equating to 6% of the float and 3 days to cover. There has been significant short covering since the management change and cost cutting plans were announced. The number of shares sold short has declined 43% from its recent high of 11.4 million shares in May 2017. In our opinion, the short covering was largely due to short sellers taking profits or insulating themselves from “stupid money” risk given the presence of activist investors.

Footnotes Adjustments and Forensic Accounting

Our Robo-Analyst technology enables us to perform forensic accounting with scale and provide the research needed to fulfill fiduciary duties. In order to derive the true recurring cash flows, an accurate invested capital, and an accurate shareholder value, we made the following adjustments to Etsy Inc.’s 2016 10-K:

Income Statement: we made $52 million of adjustments with a net effect of removing $49 million in non-operating expense (12% of revenue). We removed $50 million related to non-operating expenses and $2 million related to non-operating income. See all the adjustments made to ETSY’s income statement here.

Balance Sheet: we made $432 million of adjustments to calculate invested capital with a net decrease of $305 million. Aside from $264 million of excess cash, the most notable adjustment was $51 million (10% of reported net assets) related to deferred tax liabilities. See all adjustments to ETSY’s balance sheet here.

Valuation: we made $709 million of adjustments with a net effect of increasing shareholder value by $25 million. Cumulative decrease adjustments for total debt, deferred tax liabilities and outstanding options were offset by the increase adjustment for excess cash. This excess cash adjustment represents 14% of ETSY’s market cap.

Unattractive Funds That Hold ETSY

There are no funds receive our Unattractive-or-worse rating and allocate significantly to ETSY.

This article originally published on August 14, 2017.

Disclosure: David Trainer, Kenneth James, and Kyle Guske II receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.