Elanco Animal Health (ELAN: $24/share), the premier animal health company being spun out of Eli Lilly (LLY), is expected to begin trading on Thursday, September 20. At a price of $24 per share, the company plans to raise up to $1.7 billion with an expected market cap of ~$7.7 billion. At the IPO price, ELAN currently earns our Unattractive rating.

Elanco enters the public market with significant revenue ($2.9 billion in 2017) but falling after-tax profit (NOPAT), and negative GAAP net income. As with any healthcare firm, the valuation of ELAN is based less on its current profitability and more on the strength of its product/vaccine portfolio (and their patents) and its success in researching & developing (or acquiring) new animal health products.

This report aims to help investors sort through Elanco’s financial filings to understand the fundamentals and valuation of this IPO.

Profits Are Not as Bad as They Appear

ELAN earns revenues through the sale of animal health products in categories such as flea and tick, vaccines, osteoarthritis and pain, animal only-antibiotics, probiotics, and food animal products. The company notes they are the fourth largest animal health company in the world, based on revenue in 2017. Globally, Elanco is #1, #2, and #3 in medicinal, poultry, and cattle feed additives respectively based on 2017 revenue.

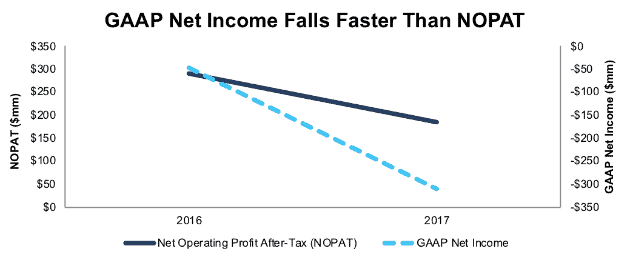

At first glance, ELAN’s GAAP net loss ballooned from -$48 million in 2016 to -$311 million in 2017, an over 500% decline. NOPAT, while positive, also fell, from $289 million in 2016 to $184 million in 2017. NOPAT fell 36% year-over-year, which is much slower than GAAP net income’s decline.

Figure 1: ELAN GAAP Net Income and NOPAT Over Past Two Years

Sources: New Constructs, LLC and company filings

Reported non-operating items overstated ELAN’s GAAP losses in both 2016 and 2017, which caused the greater decline in accounting results versus NOPAT. We remove both non-operating income and expense when calculating NOPAT to get at the true recurring profits of the business.

Our Robo-Analyst[1] uncovered non-operating items in 2017, such as:

- $375 million (13% of revenue) in asset impairment, restructuring, and other special charges

- $43 million (1% of revenue) in cost of sales due to the write-up of inventory

- $33 million (1% of revenue) in provisional benefits due to re-measurement of deferred taxes

- $6 million (1% of revenue) in change in total reserves

After all adjustments, we removed a net $495 million in non-operating expenses in 2017, which resulted in positive NOPAT compared to negative GAAP net income.

With only two years of history, it’s hard to draw any firm conclusions about the long-term trend in profitability for ELAN, but our adjustments show that NOPAT is falling, but at slower a rate than GAAP would indicate.

Red Flags for Capital Allocation

As we wrote in our Long Idea on PetMed Express (PETS), we see significant growth in the animal care market for the foreseeable future. Investors in ELAN must believe that it can capitalize on this growth while controlling costs to improve profitability. However, costly acquisitions have hampered Elanco’s ability to grow profits and create true shareholder value, even in a growing market.

Over the past three years, ELAN has spent over $6.2 billion on acquisitions. Most recently, in 2017, Elanco acquired Boehringer Ingelheim Vetmedica’s U.S. feline, canine and rabies vaccine portfolio for $882 million. In total, invested capital grew 7% in 2017, while NOPAT fell 36%. NOPAT margin fell from 10% in 2016 to 6% in 2017. This increase in invested capital, without a similar increase in profits led to ELAN’s return on invested capital (ROIC) falling from an already low 4% to 2% over the same time.

Traditional Metrics Obscure Expensive Valuation

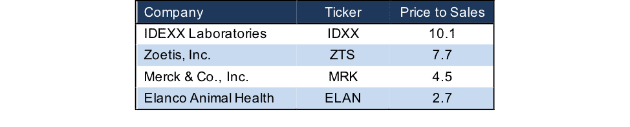

Figure 2 shows ELAN’s price-to-sales ratio is actually below its publicly-traded competitors, as named in ELAN’s S-1. However, it is worth noting that each of these firms looks vastly overvalued relative to the overall market (S&P 500), which has a price-to-sales ratio of 2.3. It’s also worth noting that, from a profitability standpoint, Elanco earns the least NOPAT and has the lowest NOPAT margin of the four companies in Figure 2.

Figure 2: Valuations for Animal Health Competitors

Sources: New Constructs, LLC and company filings

Our Discounted Cash Flow Model Reveals How Overvalued ELAN is

When we use our dynamic DCF model to analyze the future cash flow expectations baked into the stock price, we find that ELAN is overvalued at the IPO price, despite what traditional metrics show.

To justify the IPO price of $24/share, ELAN must immediately achieve 12% NOPAT margins (slightly below the 15% average of peers in Figure 2) and grow NOPAT by 10% compounded annually for the next 15 years. See the math behind this dynamic DCF scenario. This scenario implies immediate and drastic improvements in profitability.

Even if we assume ELAN can earn a 10% NOPAT margin (achieved in 2016), the stock still holds significant downside. If we assume ELAN achieves a 10% NOPAT margin and grows NOPAT by 5% compounded annually for the next decade, the stock is worth just $10/share today – a 58% downside from the IPO price. See the math behind this dynamic DCF scenario.

Each of these scenarios assumes ELAN can grow revenue by 5% compounded annually, which is the estimated growth rate of the industry through 2023 according to Vetnosis, and noted in ELAN’s S-1. For comparison, ELAN’s revenue has declined ~1% compounded annually since 2015.

IPO Investors Get No Say

Immediately following the completion of ELAN’s IPO, Eli Lilly will own 82.3% of the outstanding stock in the company (80.2% if underwriters exercise their option to purchase additional shares). While this ownership is different from dual class structures we’ve seen in recent IPOs (Snap Inc. (SNAP) or Dropbox (DBX) for instance) the effect on voting rights is the same: IPO investors get virtually no vote.

Post IPO, Eli Lilly will control the majority of voting power and the outcome of any actions requiring shareholder approval. Furthermore, LLY will be entitled to designate or nominate the number of board members proportionate to its ownership of voting shares. As long as LLY owns at least a majority of ELAN’s voting shares, LLY will be entitled to designate the chairman of the board and a majority of the members on the board.

While Ely Lilly has indicated that it plans to divest its interest in ELAN over time, it is under no obligation to do so. We’ve certainly seen worse corporate governance when it comes to voting rights (such as one person holding all the rights), but ELAN’s structure still give investors no say in corporate matters until LLY divests majority of its interest in the company.

Critical Details Found in Financial Filings by Our Robo-Analyst Technology

As investors focus more on fundamental research, research automation technology is needed to analyze all the critical financial details in financial filings. Below are specifics on the adjustments[2] we make based on Robo-Analyst findings in Elanco Animal Health’s S-1:

Income Statement: we made $513 million of adjustments, with a net effect of removing $495 million in non-operating expense (17% of revenue). You can see all the adjustments made to ELAN’s income statement here.

Balance Sheet: we made $1.3 billion of adjustments to calculate invested capital with a net increase of $405 million. The most notable adjustment was $358 million in deferred tax assets. This adjustment represented 4% of reported net assets. You can see all the adjustments made to ELAN’s balance sheet here.

Valuation: we made $515 million of adjustments with a net effect of decreasing shareholder value by $133 million. Apart from $191 million in excess cash, the largest adjustment to shareholder value was $127 million in underfunded pensions. This pension adjustment represents 2% of ELAN’s proposed market cap.

This article originally published on September 19, 2018.

Disclosure: David Trainer, Kyle Guske II, and Sam McBride receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] Harvard Business School features the powerful impact of research automation in the case New Constructs: Disrupting Fundamental Analysis with Robo-Analysts.

[2] Ernst & Young’s recent white paper “Getting ROIC Right” demonstrates the link between an accurate calculation of ROIC and shareholder value.