Despite underperforming the market for several years, this long-time Long Idea has all the tools for a successful turnaround and holds significant upside potential.

This report red flags the firms with the most underfunded pensions and the most aggressive assumptions for returns they expect to earn on the pension assets.

Pension underfunding remains dangerously high for many firms, and some companies use unusual assumptions for expected return on plan assets to mislead investors.

Tune into CNBC on Wednesday, July 12 at 3:40pm EST. New Constructs CEO, David Trainer, will discuss airline stock’s valuation and the implied market expectations across the industry.

The search for quality stocks only gets harder as companies use a growing array of tricks to deceive investors. Our research has always focused on cutting through the noise. We

Smart investors consider more than just the dividend of a stock. They also consider the principal risk. If the principal risk is greater than the dividend yield then the dividend is of no real value. I see the principal risk of this stock at more than 15% with a fair value closer to $50 – after adjusting for the pension accounting shenanigans.

Yesterday, Goldman Sach's initiated on Delta Airlines (DAL) with a Sell Rating. This stock call comes two months after my note to clients recommending shorting DAL.

As I wrote in “Don’t Be Fooled: Get Short Now”, the euro is not that different from Enron, WorldCom or the Madoff fund. All of these organizations were able to pretend they were profitable or solvent long after they were insolvent.

Now markets are finally acknowledging the intractability of the Euro debacle.

Listen in on my 15 minute interview describing the rigorous diligence New Constructs applies to every rating on the stocks, ETFs and mutual funds we cover.

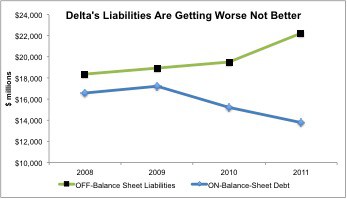

In his weekly column, The Trader, Vito Racanelli features my in-depth work on the funky accounting Delta Airlines' (DAL) uses to mask $26 billion on off-balance sheet liabilities.

Mr. Racanelli agrees

I do not think S&P's analysts are aware of Delta's staggering $22.3 billion in off-balance sheet liabilities, which include $14.1 billion in underfunded pensions and $8.2 in operating leases.

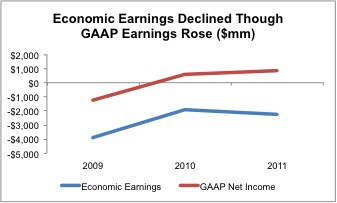

I recommend investors avoid Delta Airlines (DAL). I think the stock could see significant downward pressure as more investors realize how the company is propping up its earnings with relatively aggressive accounting for its pension and postretirement plan (“pensions”), which are already seriously underfunded.