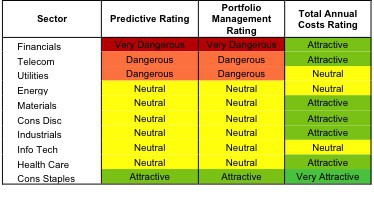

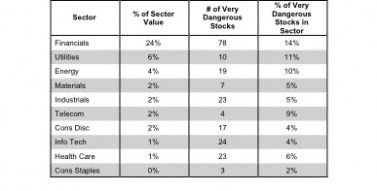

For the second quarter of 2014, only three sectors manage to even earn a Neutral rating. My sector ratings are based on the aggregation of my fund ratings for every ETF and mutual fund in each sector.

Any brick and mortar retailer carries some risk in this environment, but investors who really want exposure to this sector should look for higher quality companies than TUES. Other retailers have superior profitability metrics, better branding and e-commerce capabilities, and a cheaper valuation. The only reason to touch TUES is to short it.

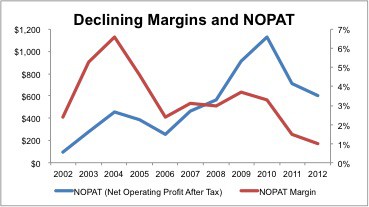

Amazon (AMZN: $356/share) filed its annual Form 10-K last week. Our analysts have picked through the financial footnotes and fine print. 2013 results reinforce my bearish thesis from May of 2013 that AMZN’s valuation implies a more unrealistic level of growth and profitability than investors realize.

Check out my sector overview on Reuters Insider here.

The Consumer Staples sector ranks first out of the ten sectors as detailed in my Sector Rankings for ETFs and Mutual Funds

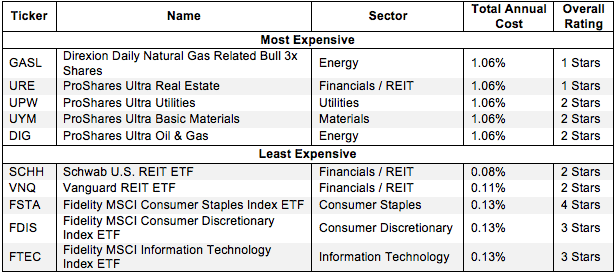

Picking from the multitude of sector ETFs is a daunting task. In any given sector there may be as many as 44 different ETFs, and there are at least 183 ETFs across all sectors.

At the beginning of the fourth quarter of 2013, only the Consumer Staples sector earns an Attractive rating. My sector ratings are based on the aggregation of my fund ratings for every ETF and mutual fund in each sector.

RAD is up against the ropes right now. The company has to contend with larger, more efficient competitors, significant debt, and declining sales. Don’t be fooled by the 150% growth in the share price this year. RAD is much worse off than its stock suggests.

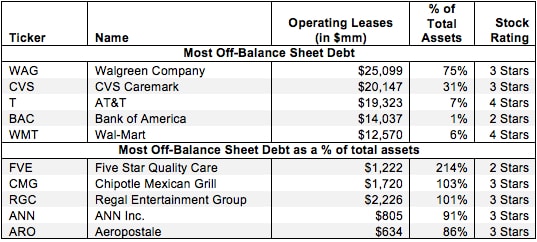

Investors who ignore off-balance sheet debt are not holding companies accountable for all of the capital invested in their business. By adding back off-balance sheet debt to invested capital, one can get a true picture of the value that management is creating for shareholders. Diligence pays.

The belief that Internet retail is or will be more profitable than traditional retail is untrue. Amazon is in a competitive, low margin business that cannot justify the profit growth implied in its valuation.

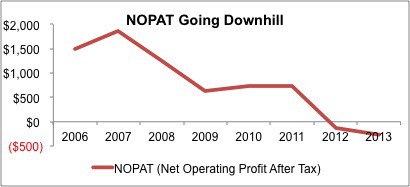

SHLD combines three themes that I have discussed in recent Danger Zone posts: overvaluation due to expectations of a construction rebound, hidden liabilities undermining a company’s financial strength, and online retailing making bricks-and-mortar stores obsolete.

At the outset of the second quarter of 2013, only a single sector earns an Attractive rating. My sector ratings are based on the aggregation of my fund ratings for every ETF and mutual fund in each sector.

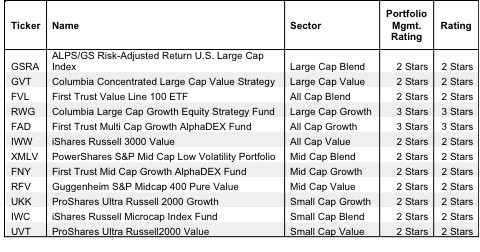

The large-cap blend style ranks second out of the twelve fund styles as detailed in my style roadmap. It gets my Neutral rating, which is based on aggregation of ratings of 40 ETFs and 1127 mutual funds in the large-cap blend style as of July 17, 2012.

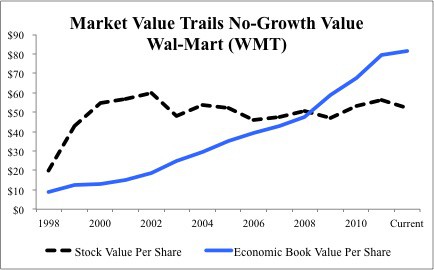

The difference between the stock price and Economic Book Value (EBV) of s stock measures the difference between the market's expectation for future profits and the no-growth value of the stock.

Only one sector, Consumer Staples, earns my Attractive rating. See Figure 1 for my ranking of all ten sectors. My sector ratings are based on the aggregation of my fund ratings for every ETF and mutual fund in each each sector.

When I ran across the recent article "270,033 pages later, a chance to catch our breath…", I could not help but admire footnoted.org's marketing moxy.

The article provides a count of the number of pages of 10-K filings that have poured in during the real earnings season. It also highlight a couple of the largest filings. At first glance, it is easy for one to assume that all of the 270,033 pages were also analyzed.

For those investors interested in rigorous research, I offer my roadmap to the best stocks and funds in the market by sector. The full sector roadmap is here.