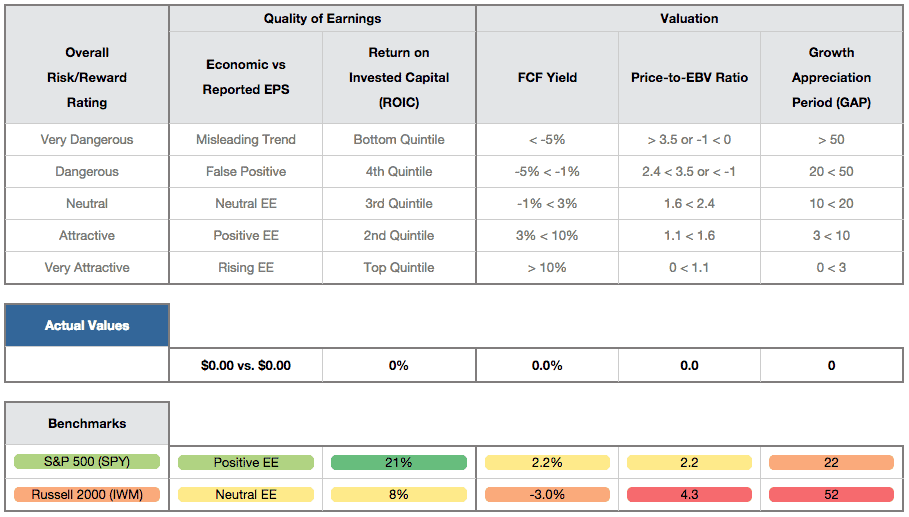

New Constructs assigns a rating to every stock under coverage according to what we believe are the 5 most important criteria for assessing the risk versus reward of stocks. New Constructs’ stock ratings are regularly featured as among the best by Barron’s.

The Portfolio Management Rating of a fund is based on the aggregated ratings of the securities it holds as well as its overall Asset Allocation. When analyzing equity funds, we use New Constructs’ stock ratings, which are regularly featured as among the best by Barron’s over the past three years.

As one financial scandal follows another, it seems the good guys are having a tougher time catching the bad guys. Recent revelations about MF Global’s ponzi scheme are another reminder of how our regulatory and oversight systems seem to let whales pass through their net.

Two of the three stocks added to our large/mid cap Most Dangerous stocks list for November are from the energy sector. Those stocks are Energy XXI (Bermuda) Ltd. (EXXI) and Superior Energy Services (SPN) – both get my very dangerous rating as do all of the Most Dangerous stocks.

All of the energy sector ETFs get a dangerous rating, which means you should sell them.

Here is a free copy of our report on AAPL for Ask Matt readers.

AAPL gets our "Very Attractive" rating because its economic earnings are positive and rising, it has one of the highest returns on invested capital (ROIC) in the world. At the same time, it's stock price reflects very low expectations for future earnings growth.

High dividend yields are NOT enough to warrant investing in the utilities sector.

Too many investors put their hard-earned money in utility stocks with the assumption that relatively high-yielding dividends from stable business make a good investment.

The real question that investors in any equity security must ask is: does my expected return from a stock justify the risk of investing in it?

As an adult, Halloween tends not to be that scary for me usually.

But after last week’s stock market rally in the face of the deteriorating situation in Europe and the rest of the world, I am afraid…for the stock market and am reminded of fall/winter 1999.

Total Annual Costs used to rate a fund's expenses reflects the all-in cost of a minimum investment in each fund assuming a 3-yr holding period, the average holding period for mutual funds.

This rating reflects all expenses, loads, fees and transaction costs in a single value that is comparable across all funds.

Our goal is to give investors as accurate a measure as possible of the cost of investing in every fund to determine whether this cost of active management is worth paying.

The Fund Asset Allocation Rating informs investors of each fund's level of allocation to cash (non-equities) as well as how that level compares to other equity mutual funds.

We assume investors in equity funds prefer those funds to be maximally invested in equities given that investors can much more cheaply invest in cash on their own. We do not believe that most investors want to pay the high fees associated with equity funds to invest in cash.

Here is a free copy of our report on DeVry (DV) for Ask Matt readers. This report provides details behind Matt’s analysis of DV in his recent article in USA Today.

Mr. Bogle, an invaluable voice of reason for investors over many years, suggests that there is too much speculation in our equity markets.

His comments jibe entirely with my post, Rise of the Speculative Movement.

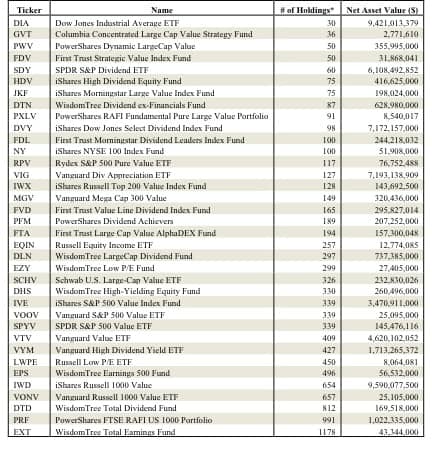

There are 25 financial sector ETFs. Per Figure 1, these 25 ETFs have drastically different stock holdings and, therefore, allocations. The lowest number of holdings is 24 while the highest is 496.

For starters, investors interested in the financial sector cannot expect many good investment options given that the sector gets my “dangerous” rating and ranks ninth out of the ten sectors that make up the economy. Details are in our sector roadmap report.

There are 36 “large cap value” ETFs. Per Figure 1, these 36 ETFs have drastically different stock holdings and, therefore, allocations. The lowest number of holdings is 30 while the highest is 1178.

How do investors pick the ETF that will deliver the best performance?

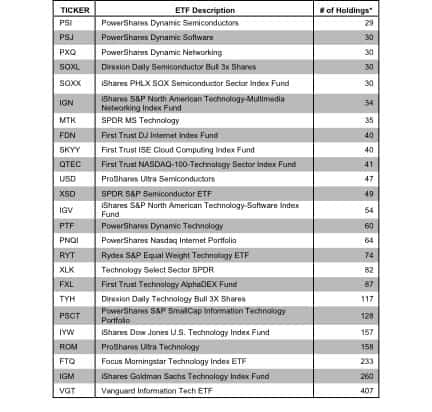

Having too many choices can be intimidating. And there are definitely lots of choices when it comes to ETFs. For example, in the equity market alone, there 30+ technology sector ETFs, or 35 ‘large cap value’ and 20 financial ETFs. A very healthy selection abounds for every category of ETF.

The problem is that these ETFs are not made the same even though they may be in the same category. There are major differences in methodologies between funds, which results in drastically different holdings even within a given sector. See Figure 1.

Similar to my prior interviews on SBUX, I found it easy to make the bear case for a stock that is as expensive as Starbucks (SBUX). As my regular readers know, when I say "expensive", I back that up with details such as: to justify its $40 stock price (closing price from prior day), SBUX had to grow profits at 10% compounded annually for more than 25 years.

In addition to my stock-brawl interview on Thursday (9/29/11), I have commented to the media on Starbucks (SBUX) many times. Below is a list (with links) to my past opinions/comments on SBUX.

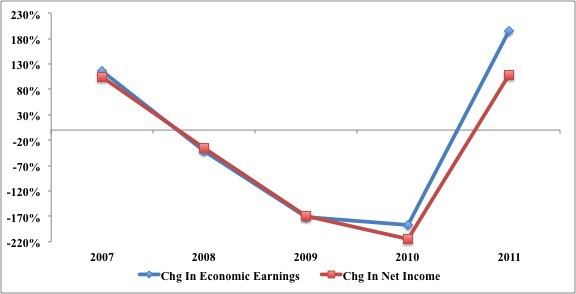

Most of my research and publishing tends to focus on companies manipulating accounting rules to make their reported earnings look better than the real economic cash flows of their business.

It is unfortunately rare that I find a company whose economic earnings are outpacing the reported accounting results and whose stock is cheap.

One such company is Lam Research (LRCX – very attractive rating). One of September’s most attractive stocks, LRCX offers investors hidden value.

Here is a free copy of our report on GE for Ask Matt readers. This report provides details behind Matt’s analysis of GE in his recent article in USA Today. Click here for our report: General Electric (GE) Neutral Risk/Reward Rating.

MarketWatch's Chuck Jaffe feature's New Constructs mutual fund rating system, which has a "neutral" rating on the Magellan fund.

Our fund rating system is the same as our stock rating system, which has received many accolades for its predictive power.