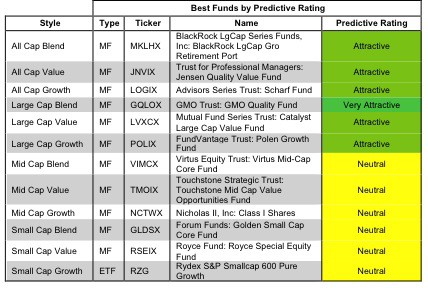

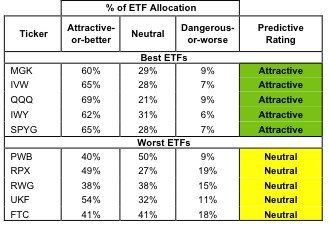

Best & Worst ETFs and Mutual Funds July 2012: Large-cap Growth Style

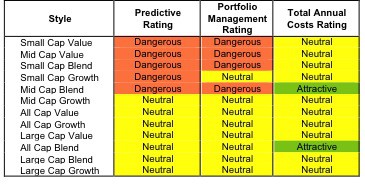

The large-cap growth style ranks the best out of the twelve fund styles as detailed in my style roadmap. It gets my Neutral rating, which is based on aggregation of ratings of 26 ETFs and 724 mutual funds in the large-cap growth style as of July 16, 2012.