Thirteen new stocks made March’s Dividend Growth Stocks Model Portfolio, which was made available to members on March 29, 2023.

Recap from February’s Picks

On a price return basis, our Dividend Growth Stocks Model Portfolio (-4.7%) underperformed the S&P 500 (+0.1%) by 4.8% from February 28, 2023 through March 27, 2023. On a total return basis, the Model Portfolio (-4.5%) underperformed the S&P 500 (+0.4%) by 4.9% over the same time. The best performing stock was up 5%. Overall, nine out of 30 Dividend Growth stocks outperformed their respective benchmarks (S&P 500 and Russell 2000) from February 28, 2023 through March 27, 2023.

This report leverages our cutting-edge Robo-Analyst technology to deliver proven-superior[1] fundamental research and support more cost-effective fulfillment of the fiduciary duty of care.

This Model Portfolio mimics an “All Cap Blend” style with a focus on dividend growth. Selected stocks earn an Attractive or Very Attractive rating, generate positive free cash flow (FCF) and economic earnings, offer a current dividend yield >1%, and have a 5+ year track record of consecutive dividend growth. This Model Portfolio is designed for investors who favor long-term capital appreciation over current income, but still appreciate the power of growing dividends.

Featured Stock for February: Snap-On Inc. (SNA: $237/share)

Snap-On (SNA) is the featured stock in March’s Dividend Growth Stocks Model Portfolio. We first made Snap-On a Long Idea in February 2018 and the stock is up 51% while the S&P 500 is up 52% since then.

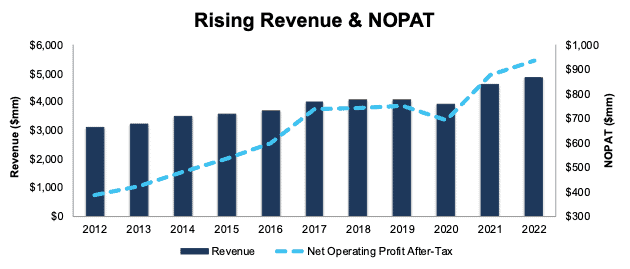

Snap-On has grown revenue by 5% compounded annually and net operating profit after tax (NOPAT) by 9% compounded annually over the past decade. The company’s NOPAT margin has increased from 12% in 2012 to 19% in 2022. Even though invested capital turns fell slightly during that period, NOPAT margins increased enough to drive return on invested capital (ROIC) from 11% in 2012 to 16% in 2022.

Figure 1: Snap-On’s Revenue & NOPAT Since 2012

Sources: New Constructs, LLC and company filings

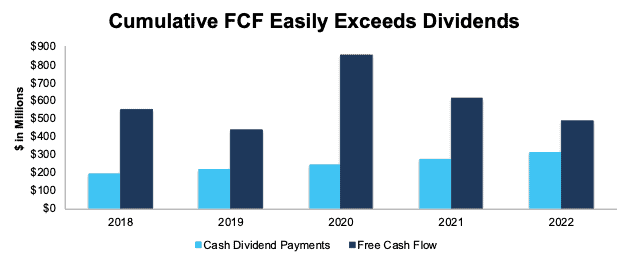

Free Cash Flow Supports Regular Dividend Payments

Snap-On has increased its regular dividend from $3.41/share in 2018 to $5.88/share in 2022, or 15% compounded annually. The current quarterly dividend, when annualized, equals $6.48/share and provides a 2.7% dividend yield.

More importantly, Snap-On’s free cash flow (FCF) easily exceeds its regular dividend payments. From 2018 through 2022, Snap-On generated $2.9 billion (22% of current enterprise value) in FCF while paying $1.2 billion in dividends. See Figure 2.

Figure 2: Snap-On’s FCF vs. Regular Dividends Since 2018

Sources: New Constructs, LLC and company filings

Companies with FCF well above dividend payments provide higher-quality dividend growth opportunities. On the other hand, dividends that exceed FCF cannot be trusted to grow or even be maintained.

SNA Is Undervalued

At its current price of $237/share, Snap-On has a price-to-economic book value (PEBV) ratio of 1.1. This ratio means the market expects Snap-On’s NOPAT to increase just 10% from 2022 levels over the life of the company. This expectation seems overly pessimistic given that Snap-On has grown NOPAT by 9% compounded annually over the past decade and 12% compounded annually over the past two decades.

Even if Snap-On maintains its 2022 NOPAT margin of 19% and grows revenue by just 4% compounded annually over the next decade, the stock would be worth $285/share today – a 20% upside. In this scenario, Snap-On’s NOPAT would grow just 4% compounded annually through 2032. Should the company’s NOPAT grow more in line with historical growth rates, the stock has even more upside.

Add in Snap-On’s 2.7% dividend yield and a history of dividend growth, and it’s clear why this stock is in March’s Dividend Growth Stocks Model Portfolio.

Critical Details Found in Financial Filings by Our Robo-Analyst Technology

Below are specifics on the adjustments we make based on Robo-Analyst findings in Snap-On’s 10-K:

Income Statement: we made $134 million in adjustments with a net effect of removing $26 million in non-operating expenses (<1% of revenue). Clients can see all adjustments made to Snap-On’s income statement on the GAAP Reconciliation tab on the Ratings page on our website.

Balance Sheet: we made $1.8 billion in adjustments to calculate invested capital with a net decrease of $168 million. The most notable adjustment was $528 million (9% of reported net assets) in other comprehensive income. See all adjustments made to Snap-On’s balance sheet on the GAAP Reconciliation tab on the Ratings page on our website.

Valuation: we made $1.9 billion in adjustments, with a net decrease of $605 million in shareholder value. Apart from total debt, one of the most notable adjustments to shareholder value was $660 million in excess cash. This adjustment represents 5% of Snap-On’s market value. See all adjustments to Snap-On’s valuation on the GAAP Reconciliation tab on the Ratings page on our website.

This article was originally published on April 5, 2023.

Disclosure: David Trainer, Kyle Guske II, and Italo Mendonça receive no compensation to write about any specific stock, style, or theme.

Questions on this report or others? Join our Society of Intelligent Investors and connect with us directly.

[1] Our research utilizes our Core Earnings, a more reliable measure of profits, as proven in Core Earnings: New Data & Evidence, written by professors at Harvard Business School (HBS) & MIT Sloan and published in The Journal of Financial Economics.