This position was closed due to acquisition on December 24, 2019. Details in the Position Update report here.

Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life.

This firm was once at the forefront of a new industry, but commoditization of its core product and lack of innovation has resulted in management’s attempt to re-invent the company through acquisitions. Profit growth expectations embedded in the stock price are likely unfeasible in light of current financial performance and formidable competitive challenges.

We think execution risk is high and the probability of upside to already high expectations is low. The firm lacks a clear competitive advantage amidst a sea of well-established rivals. Carbonite, Inc. (CARB, $19/share) is this week’s Danger Zone pick.

Carbonite Background

Carbonite Inc. (CARB) offers cloud-based data storage and back-up solutions to businesses and consumers. CARB was among the first to offer cloud back-up services to the masses and went public in 2011 at $10/share. Since the IPO, the proliferation of cloud storage options and lack of timely innovation has resulted in the loss of first mover advantage and a deteriorating competitive position.

CARB’s legacy consumer data back-up business is in decline. The company is now repositioning itself through acquisitions to target the business continuity and disaster recovery markets. The two original founders remain on the Board of Directors, but their focus appears to be on outside endeavors. The duo has raised capital for a cloud data storage start-up, called Wasabi, to compete directly against Amazon Web Services (AWS).

Slowing Growth Gives Way to M&A

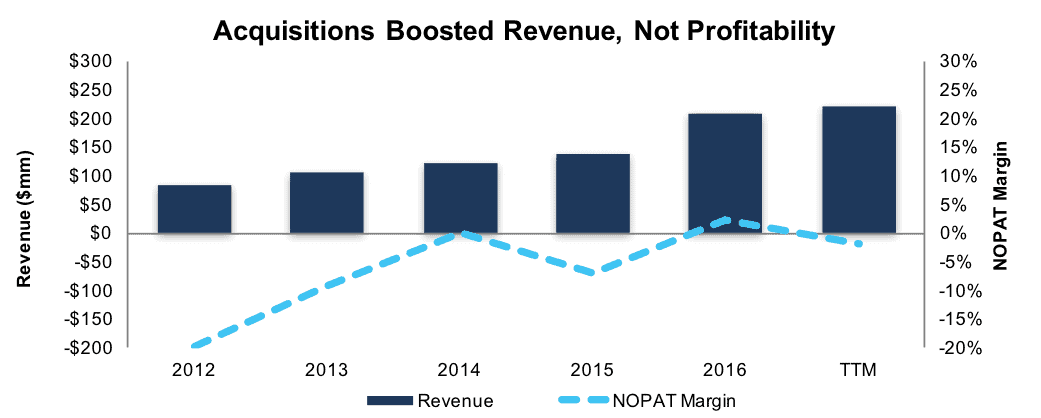

CARB has grown revenue 24% compounded annually since 2012. Over 60% of this growth (in dollar terms) has come since the end of 2015 by way of two acquisitions, which totaled $80 million in deal value. Revenue growth had slowed to 11% in 2015 before jumping to 52% in 2016 and 29% over the trailing twelve months (TTM).

Most recently, revenue growth slowed to 10% in 2Q17 vs. 2Q16. This increase was mainly driven by the recent Double-Take Software acquisition. Without this acquisition’s $5-$6 million quarterly revenue contribution (per company guidance), it appears CARB generated little-to-no organic revenue growth over the TTM.

Figure 1: CARB’s Revenue Growth & NOPAT Margins

Sources: New Constructs, LLC and company filings

Profits Remains Illusive

CARB has not achieved consistent profitability since going public. The company posted a break-even 0% NOPAT margin in 2014. Profitability then swung between -7% and +2% NOPAT margins over the next two years. CARB’s current NOPAT margin has dipped to -2% (TTM) due to expense growth. 2Q17 total expenses increased 23% vs. 2Q16 while 2Q17 revenue increased only 10% vs. 2Q16.

In addition, free cash flow (FCF) swung to -$76 million TTM from $10 million in 2016 due to the decline in NOPAT and capital investment in acquisitions.

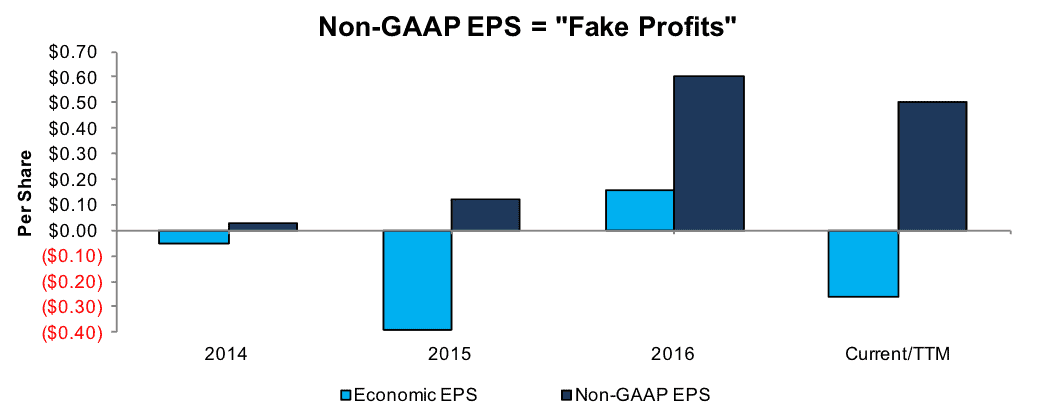

Per Figure 2 below, management’s focus on non-GAAP metrics creates an illusion of profitability. Specifically, management’s definition of ‘non-GAAP net income per share’ allows for the exclusion of: purchase accounting adjustments, stock-based compensation, litigation expenses, acquisition expenses, intangible amortization, non-cash convertible debt interest expense, and the tax effect of non-GAAP adjustments at a 13% effective rate.

Removing so many expenses relevant to the operations of the business, especially with the new acquisition-driven strategy, is suspect.

Figure 2: Non-GAAP EPS vs. Economic EPS

Sources: New Constructs, LLC and company filings

Poor Return on Invested Capital

CARB’s return on invested capital (ROIC) has averaged -5% over the past two years. The current ROIC of -9% (TTM) is in the bottom quintile of our coverage universe and well below the median 5% ROIC generated by 230 companies in the software and services sector.

The main impediment to higher ROIC is NOPAT margin as the balance sheet is relatively efficient. CARB’s capital turnover ratio (revenue divided by invested capital) is 2.6 compared to an average of 1.3 for the software and services sector. For the company to earn an adequate ROIC above the cost of capital, it would need to earn a 3% NOPAT margin on TTM revenue without growing invested capital.

This hurdle appears manageable given the software sector’s median 5% NOPAT margin. However, a low single-digit profit margin provides little room to maneuver, while invested capital seems more likely to balloon than remain flat given the investment in new business lines and acquisition-driven strategy.

Executive Comp Aligned with Misleading Metrics

We know from numerous case studies that changes in ROIC are directly correlated to changes in market value. Accordingly, we favor compensation plans that use ROIC to measure performance to ensure executives’ interests are aligned with shareholders’ interests. Revenue and non-GAAP performance targets can be an incentive to sacrifice profitability for volume, or worse, engage in acquisitions that destroy shareholder value.

CARB management focusses exclusively on non-GAAP in their presentation of company performance and to determine executive compensation. CARB’s compensation structure consists of base salary (~20%), incentive cash bonus (~30%) and equity incentives (~50%).

Incentive cash bonuses are based on non-GAAP metrics such new bookings (50%), renewal bookings (25%) and adjusted free cash flow (25%). Equity incentives are intended to align executive’s interest with shareholders, but the shares vest based solely on stock price performance.

While the stock has done fine during the tech stock bull market, the company has generated -$38 million of economic profits over the past five years. Until CARB aligns its compensation plans with financial goals that actually constitute profits, we are not optimistic that shareholder value destruction will come to an end on its own.

Competitive Landscape is Daunting

There are at least 50 competitors within the consumer data back-up and protection market. These companies fall into two main categories: a) the cloud services of industry giants such as Amazon (AWS), Apple (iCloud), Google (GoogleDrive) and Microsoft (OneDrive); and b) significantly smaller independent companies seeking to differentiate themselves through product customization and customer service. The largest and most visible of these independent competitors include: Backblaze, Box, CrashPlan, DropBox, iDrive, Mozy and SOS. Each of these competitors offers products comparable to CARB in terms of capability and pricing.

Competition for consumer business among smaller firms, where discounted promotions are the norm, is fierce. CARB currently offers computer back-up plans from $59.99/year. BackBlaze offers computer back-up plans for $5/month. iDrive currently offers the first-year of computer back-up plans for 90% off, or $6.95. iDrive has won PC Magazine editor’s choice award in the category for three consecutive years. iDrive currently receives a 4.5 out of 5 (Excellent) rating compared to 3.5 (Good) for Carbonite.

The industry giants’ integrated cloud services have commoditized the consumer market to the point where firms such as CARB have been forced to adapt by developing enterprise service platforms. We believe CARB has been slow to adapt to this new competitive reality. Competitors such as Box, Inc. (BOX) are far ahead CARB in the enterprise market despite the two firms being founded in the same year. BOX has business relationships with 64% of Fortune 500 companies and a co-selling agreement with Microsoft. Competing directly against Amazon is already a lost cause in light of AWS’s rapid growth to $12 billion in revenue.

Disaster recovery and business continuity seem to be maturing into distinct markets, but they remain difficult to quantify and separate from the $50 billion expected to be spent by 2018 in the overall Cloud Professional Services market. According to one study, the disaster recovery as service market (DRaaS) is estimated to grow to $12 billion in 2020 from $1.4 billion in 2015. While there is demand to fuel growth in this market, there is no shortage of well-established competitors, such as: International Business Machines (IBM), Iron Mountain (IRM), Vmware (VMW), Equinix (EQIX), FTI Consulting (FCN) and Sungard Systems (private).

CARB lacks a clear competitive advantage at either the consumer or enterprise end of the cloud services market. The company has all but ceded the consumer data back-up segment (~50% of revenue) to competitors. This consumer surrender is evident in guidance for -10%-0% growth in consumer segment revenue and recent acquisitions which are entirely enterprise focused. This re-positioning effort is likely to require investment that will prevent near-term improvement in lagging profitability metrics.

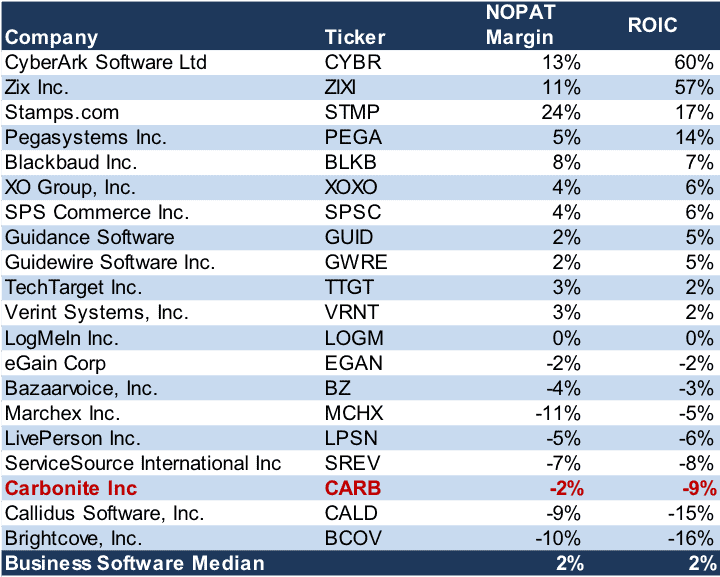

Per Figure 3 below, CARB’s NOPAT margin and ROIC rank near the bottom of a peer group that comes mostly from CARB’s annual Proxy statement. These thin margins give CARB little margin of safety against adverse business conditions or capacity to invest for future growth with diluting investors with outside capital.

Figure 3: Competitive Advantage Not Apparent for CARB

Sources: New Constructs, LLC and company filings

Considering the Bull Case

The bull case depends on CARB successfully repositioning from providing consumer cloud backup to providing disaster recovery and business continuity solutions to small/medium-sized businesses.

To establish an enterprise services presence, CARB purchased EVault assets from Seagate Technology (STX) and Double-Take Software from Vision Solutions (private). EVault assets were purchased from STX for just $14 million. Double-Take’s $65 purchase price was 73% less than the $242 million Vision Solutions paid in 2010. Developing these relatively small investments in discarded assets into an edge over well-established competitors strikes us as a longshot. The current stock price implies it’s a high likelihood.

Bulls assume that synergies from recent acquisitions will cause revenue to accelerate while expense growth moderates. It is far from certain that recent acquisitions will bring the advertised revenue synergies. We also believe the competitive landscape will prove too challenging for CARB to back off expenses. CARB is more likely to be forced to spend aggressively in the near term to integrate acquisitions and pursue revenue opportunities. Under this scenario, reaching the profitability levels implied by current market expectations seems very unlikely.

Potential Catalysts

As noted above, we believe the near-term investment required for CARB to reposition from consumer to enterprise is likely to prolong the current period of losses. As such, we believe that earnings expectations for next year (currently $1.00/share) are far too high and likely to be revised lower as actual earnings are reported.

Market participants have shown themselves to be more than willing to fund operational losses that drive high revenue growth rates, however. Revenue growth, however, is where we believe CARB will truly disappoint investors.

As noted previously, we argue that CARB’s organic revenue growth in 2Q17 vs. 2Q16 fell to near 0% excluding the revenue contribution of Double-Take Software. If the consumer segment was operating within negative 10% to 0% growth guidance and the enterprise segment was growing in line with “bookings” growth of 20%-30%, then CARB’s organic revenue growth (excluding Double-Take) should have been 5%-15% in 2Q17, not 0%.

Given the intense competition on the consumer side and the company’s too-little-too-late entry into enterprise services, we believe that revenue growth is a high risk of disappointing over the coming year.

High Expectations Embedded in Stock Price

CARB shares have risen 16% YTD and 46% over the past year to outperform the S&P 500 (+9% YTD, +13% 1Y). This appreciation occurred, despite the steep YTD decline in NOPAT, due to speculation that the company can successfully re-invent itself. Market expectations for 2017 profits (i.e. “consensus EPS”) have increased 33% over the past year to $0.75/per share. However, this estimate reflects company-defined “non-GAAP EPS” which excludes a host of real costs. For comparison, “non-GAAP EPS” has totaled $0.50 over the trailing twelve months compared to economic EPS of -$0.26.

To justify its current price of $19/share, CARB must grow NOPAT by 11% compounded annually for the next 19 years. This scenario assumes CARB grows revenue to $910 million (from $220 million TTM) or 8% compounded annually. This scenario also assumes the NOPAT margin improves to the sector median of 5% (-2% TTM). Achieving this scenario seems highly unlikely given that the consumer half of the revenue base is in decline while the enterprise half has yet to display evidence of sustainable growth at levels consistent with investor expectations.

Even if we assume CARB can grow NOPAT 18% compounded annually over the next decade, the stock is still worth only $13.50 today – a 29% downside risk. This scenario assumes CARB grows revenue to $533 million, or 10% compounded annually. This scenario also assumes an improvement in NOPAT margin to 5%.

Each of these scenarios assumes CARB is able to grow revenue, NOPAT and FCF without increasing working capital or investing in fixed assets. This assumption is unlikely but allows us to create optimistic scenarios that demonstrate just how high expectations embedded in the current valuation really are. For reference, invested capital increased from $39 million in 2012 to $86 million TTM, or 19% compounded annually.

Assessing Acquisition Risk

The largest risk to any bear thesis is what we call “stupid money risk”, which means a strategic buyer acquires CARB at a higher price despite the stock already being overvalued. In our view, CARB is not currently an attractive acquisition target due to its questionable competitive position and lack of consistent free cash flow.

We begin assessing acquisition value by adjusting for liabilities that would make an acquisition more expensive than accounting numbers suggest. For CARB, these liabilities equal 7% of market cap:

- $24 million in off-balance-sheet operating leases

- $15 million in outstanding stock options.

After adjusting for hidden liabilities, and baking in meaningful revenue growth and margin synergies, CARB is worth less than its current share price even in the most optimistic scenario. As shown below, an acquisition of CARB above the current price is possible only if the acquirer is willing to destroy shareholder value.

Figure 5 assumes an acquirer’s ROIC hurdle in an acquisition of CARB is equal to the software sector’s 6% weighted average cost of capital (WACC). Even if an acquirer can grow CARB’s revenue 20% compounded annually and operate at a 5% NOPAT margin over the next five years, the stock is currently overvalued by 18%. Any deal that only achieves a 6% ROIC would likely be value neutral and not accretive given the software sector’s average WACC of 6%.

Figure 4: Implied Acquisition Prices to Achieve 6% ROIC

Sources: New Constructs, LLC and company filings.

Figure 5 assumes an acquirer’s ROIC hurdle in an acquisition of CARB is 8%, or the software sector’s WAAC plus a 2% economic profit margin. An acquisition of CARB at these prices could be accretive to a firm with a 6% WACC, assuming the revenue and margin synergies come to pass. Even in the best-case scenario, an acquirer would destroy $240 million in shareholder value purchasing CARB at its current valuation. The most an acquirer should pay for CARB is $11/share (41% downside).

Figure 5: Implied Acquisition Prices to Achieve 8% ROIC

Sources: New Constructs, LLC and company filings.

CARB Offers Minimal Shareholder Yield

CARB does not pay a cash dividend. The company does have a repurchase authorization in place through May 2018 with $5.2 million of the original $30 million authorization remaining. No shares were repurchased in 2Q17 following the repurchase of 767,000 shares for $15 million in 1Q17. At the current price of $19/share, the remaining authorization amounts to 1% of outstanding shares and a 1% potential shareholder yield.

While heavy 1Q17 repurchase activity appeared to lift the stock, going forward CARB offers little of the downside protection that a solid shareholder yield can provide. Given the level of risk we see in the valuation and forward expectations, this protection could be sorely missed.

Insider Trading and Short Interest

Insiders own 16% of outstanding shares. Insider activity has been universally on the sell side over the past year. The last significant insider buying occurred in early 2016 when the stock was trading at $6-$7/share. Short interest is currently 2.9 million shares, equating to 13% of the float and 7 days to cover. The number of shares sold short has increased significantly from 1.2 million shares at year end and 320,000 shares a year ago.

Footnotes Adjustments and Forensic Accounting

Our Robo-Analyst technology enables us to perform forensic accounting with scale and provide the research needed to fulfill fiduciary duties. In order to derive the true recurring cash flows, an accurate invested capital, and an accurate shareholder value, we made the following adjustments to Carbonite’s 2016 10-K:

Income Statement: we made $10 million of adjustments with a net effect of removing $9 in non-operating expense (4% of revenue). We removed $9 million related to non-operating expenses and $1 million related to non-operating income. See all the adjustments made to CARB’s income statement here.

Balance Sheet: we made $89 million of adjustments to calculate invested capital with a net decrease of $19 million. The most notable adjustment was $24 million (73% of reported net assets) related to off-balance sheet operating leases. See all adjustments to CARB’s balance sheet here.

Valuation: we made $262 million of adjustments with a net effect of decreasing shareholder value by $34 million. We made $148 million of decrease adjustments for total debt and outstanding options which were partially offset by a $114 million increase adjustment for excess cash. The -$34 million net valuation adjustment represents 6% of CARB’s market cap.

Unattractive Funds That Hold CARB

The following funds receive our Unattractive-or-worse rating and allocate significantly to CARB.

- Riley Diversified Equity Fund (BRDZX) – 4% allocation and Very Unattractive rating.

- Saratoga Small Capitalization Portfolio (SSCCX) – 2% allocation and Unattractive rating.

This article originally published on August 29, 2017.

Disclosure: David Trainer, Kenneth James, and Kyle Guske II receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.