We published an update on GME on April 25, 2022. A copy of the associated update report is here.

One-year after the reckless meme-stock rally of late January 2021, the valuation of some of the most popular meme-stocks, especially GameStop (GME: $109/share) and AMC Entertainment (AMC), remain untethered from reality. Looking back, here are key takeaways:

- The meme-stock trade grabs fewer headlines than a year ago, but it still affects the stock market today.

- Investing in meme stocks carries reckless and unnecessary risk, which puts an investor’s portfolio in danger of potentially devastating declines.

- We don’t have a problem paying a premium for a company producing strong profits, but that isn’t the case with any of the meme stocks.

- Investors need reliable fundamental research to assess corporate profits, more than ever, as the market rotates away from high-flying growth names to more stable cash generators

- The stock market decline so far in 2022 suggests investors are paying much closer attention to profits valuations than they did in 2021.

- A narrowing gap between valuations and fundamentals is not good news for meme-stock investors, who tend to completely ignore due diligence.

- Meme-stocks like GameStop (GME) and AMC Entertainment (AMC) remain dangerously overvalued and don’t generate anywhere near the profits necessary to justify their current valuations.

Below we highlight how, despite falling significantly from its peak in 2021, GME remains a dangerous stock. We do the math to show how the business must perform to justify its current price. We also look at more realistic scenarios, which show that GME could have upwards of 59% downside.

Meme-Stock Rally Stagnated And Has Farther To Fall

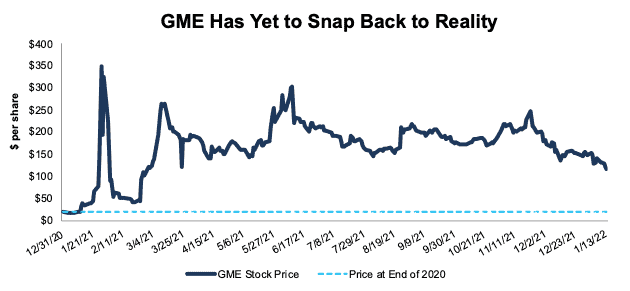

Meme-traders (or self-proclaimed “apes”) threw caution to the wind and piled into GameStop in January 2021, sending the stock soaring to as high as $347/share (based on closing prices). Even after falling 68% from this peak, GME still trades nearly 500% higher than it did at the end of 2020, per Figure 1.

Figure 1: GME Remains 500% Above 2020 Closing Price

Sources: New Constructs, LLC

GME has yet to trade in-line with its actual business fundamentals. This phenomenon remains in place for other popular meme-stocks, such as AMC Entertainment (AMC) and Express (EXPR). Even Koss Inc. (KOSS), which trades 85% below its meme-stock peak, is still nearly 200% higher than its 2020 closing price.

Given that these stocks still trade so much higher than is warranted by their fundamentals, it’s clear that investors and apes alike continue to ignore fundamental research and are taking unnecessary risks with their investments.

Changes Haven’t Fixed a Broken Business

Despite boardroom and executive changes, GameStop remains a lagging brick-and-mortar retailer in an increasingly online world. While the stock got a bump recently from reports that it is entering the NFT and crypto market (a similar playbook to meme-stock companion AMC), these headlines do little to change the underlying fundamentals of the business.

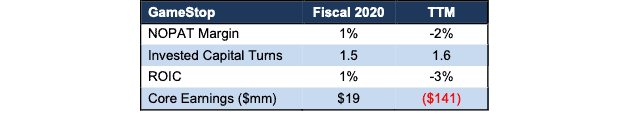

In fiscal 2020 (year ended 2/1/20), before the meme-stock run, the firm’s net operating profit after-tax (NOPAT) margin was 1% and its invested capital turns, a measure of balance sheet efficiency, sat at 1.5, which drove a return on invested capital (ROIC) of just 1%. Over the trailing twelve months (TTM), GameStop’s NOPAT margin has fallen to -2% while its ROIC has fallen to -3% TTM.

Core Earnings[1], a more accurate measure than reported earnings, have fallen from $19 million in fiscal 2020 to -$141 million over the TTM. Despite the clear deterioration of the business, GameStop’s stock price continues to trade as if fundamentals will never matter.

Figure 2: GameStop’s Fundamentals Pre-and-Post Meme-Stock Rally

Sources: New Constructs, LLC and company filings

Quality Research Helps Measure Risk More Clearly

While shorting GME could be a losing proposition, we think it is important to understand the high risk in owning the stock by quantifying the future cash flow expectations in the current stock price.

It’s clear meme-traders have ignored such due diligence, but we’re making it easy for them to have it.

GME is Priced to Generate 150% the Revenue of Activision Blizzard

We use our reverse discounted cash flow (DCF) model to analyze the expectations for future profit growth implied by GameStop’s stock price. In doing so, we find that at $109/share, GameStop is priced as if it will immediately reverse falling margins and grow revenue at an unrealistic rate for an extended period of time.

Specifically, to justify its current price GameStop must:

- improve its NOPAT margin to 3% (equals its three-year average prior to COVID-19, compared to -2% TTM) and

- grow revenue by 15% compounded annually through fiscal 2028 (1.5x the projected video game industry growth through 2027)

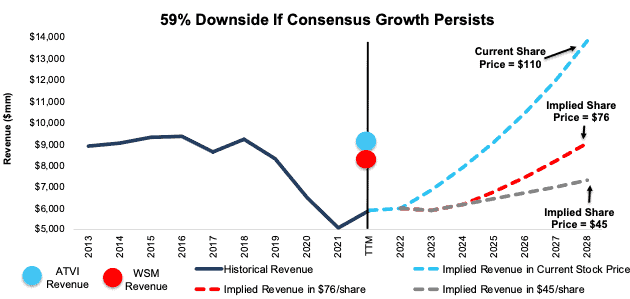

In this scenario, GameStop earns over $13.5 billion in revenue in fiscal 2028 or 150% the trailing-twelve-months revenue of Activision Blizzard (ATVI) and 168% the revenue of successful hybrid brick-and-mortar & e-commerce retailer Williams-Sonoma (WSM). For reference, GameStop’s revenue fell by 1% annually from fiscal 2009 to fiscal 2019.

There is a 31%+ Downside If Consensus is Right: In this scenario, GameStop’s:

- NOPAT margin improves to 3%,

- revenue grows at consensus rates in fiscal 2022, 2023, and 2024, and

- revenue grows 10% a year from fiscal 2025 through fiscal 2028 (equal to projected industry growth rate through 2027), then

the stock is worth just $76/share today – a 31% downside to the current price. If GameStop’s growth continues to slow, or its turnaround stalls completely, the downside risk in the stock is even higher, as we show below.

There is a 59%+ Downside If Growth Slows to Achievable Rates: In this scenario, GameStop’s

- NOPAT margin improves to 2% (5-year average),

- revenue grows at consensus rates in fiscal 2022, 2023, and 2024, and

- revenue grows 4.4% a year from fiscal 2025 through fiscal 2028 (continuation of fiscal 2024 consensus), then

the stock is worth just $45/share today – a 59% downside to the current price.

Figure 3 compares the firm’s historical revenue and implied revenue for the three scenarios we presented to illustrate just how high the expectations baked into GameStop’s stock price remain. For reference, we also include the TTM revenue of Activision Blizzard and Williams-Sonoma.

Figure 3: GameStop’s Historical Revenue vs. DCF Implied Revenue

Sources: New Constructs, LLC and company filings

Fundamentals Provide Clarity in Frothy Markets

Wall Street isn’t in the business of warning investors of the dangers in risky stocks because they make too much money from their trading volume and underwriting of debt and equity sales.

With a better grasp on fundamentals[2], investors have a better sense of when to buy and sell – and – know how much risk they take when they own a stock at certain levels. Without reliable fundamental research, investors have no way of gauging whether a stock is expensive or cheap. Without a reliable measure of valuation, investors have little choice but to gamble if they want to own stocks.

Only independent firms are free to provide unconflicted research and navigate Wall Street conflicts and analyst biases. With new technology to cut through the deluge of data in financial filings and overcome the flaws in Wall Street research, self-directed investors are better positioned than ever to make informed decisions.

This article originally published on January 20, 2022.

Disclosure: David Trainer, Kyle Guske II, and Matt Shuler receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] Only Core Earnings enable investors to overcome the flaws in legacy fundamental data and research, as proven in Core Earnings: New Data & Evidence, written by professors at Harvard Business School (HBS) & MIT Sloan for The Journal of Financial Economics.

[2] Our research utilizes our Core Earnings, a more reliable measure of profits, as proven in Core Earnings: New Data & Evidence, written by professors at Harvard Business School (HBS) & MIT Sloan and published in The Journal of Financial Economics.