On August 27th, I met with my fellow members of the FASB’s Investor Advisory Committee (IAC) to discuss the proposed treatment of operating leases on the balance sheet by the Financial Accounting Standards Board (FASB).

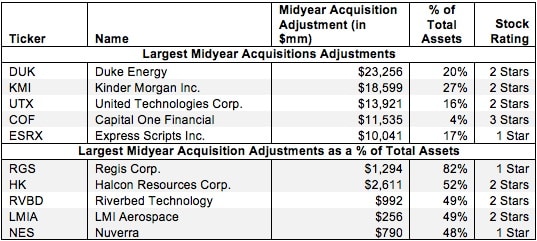

When a company makes an acquisition, the entire purchase price is added to the company’s balance sheet in the year of the acquisition along with any assumed debts or other long-term liabilities. However, the only income added to the income statement is that which occurs after the acquisition closes. In other words, the balance sheet is charged with the full price of the acquisition while the income statement only gets partially impacted.

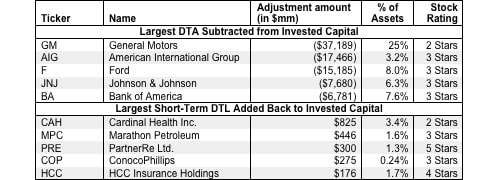

DTAs artificially raise reported assets and do not help generate operating profit while DTLs are like a source of interest-free financing. We remove the impact of DTAs and DTLs from our calculation of invested capital to ensure the more accurate measure of a firm’s return on invested capital (ROIC).

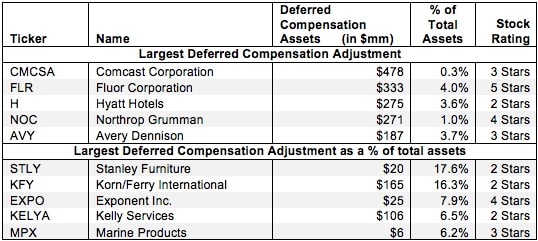

Deferred compensation plans delay employee compensation until a later date. The assets held for these plans are used to compensate employees in the future, not to generate profits for the company. As such, they should not be factored into the calculation of a company’s return on invested capital (ROIC).

We applaud the Financial Accounting Standards Board's (FASB) latest proposal to change the way leases are reported. The new rules would make only the shortest-term operating leases exempt from being recorded on the balance sheet.

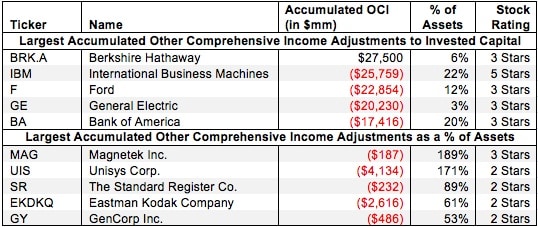

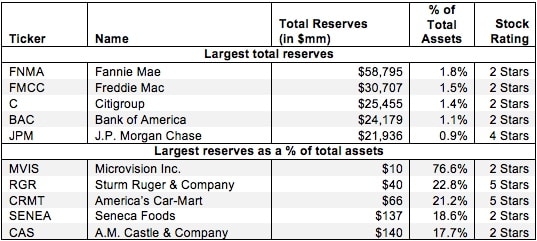

Reported assets don’t tell the whole story of the capital invested in a business. Accounting rules provide numerous loopholes that companies can exploit to hide balance sheet issues and obscure the true amount of capital invested in a business.

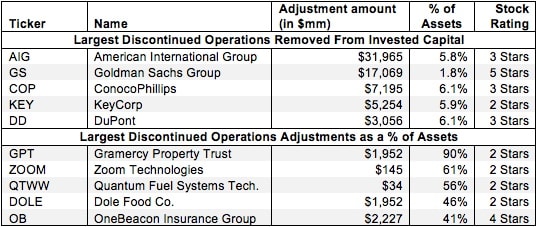

Most investors would never know that discontinued operations distort GAAP numbers by over-stating assets on balance sheets and distorting the picture of a company’s ability to generate a return on that capital.

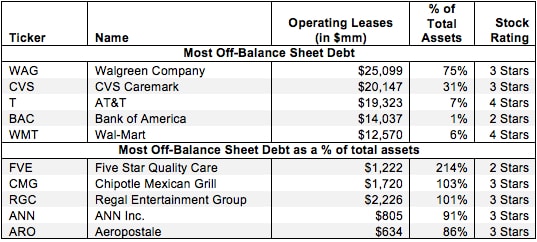

Investors who ignore off-balance sheet debt are not holding companies accountable for all of the capital invested in their business. By adding back off-balance sheet debt to invested capital, one can get a true picture of the value that management is creating for shareholders. Diligence pays.

Reported assets don’t tell the whole story of the capital invested in a business. Accounting rules provide numerous loopholes that companies can exploit to hide issues and obscure the true amount of capital invested in a business over its life.

This article details the uniquely rigorous diligence behind each of our ratings on 3000 stocks, 7000 mutual funds and 400 ETFs. It contains reports on all the adjustments we make to convert GAAP data to economic earnings and derive true shareholder value in a discounted cash flow model.

This report summarizes our series of reports on how to convert GAAP data to economic earnings and derive true shareholder value in a discounted cash flow model as well as more accurate measures of economic

Our Company Valuation models are very sophisticated discounted cash flow and earnings quality models.

An enormous amount of works goes into every model. I wish I could offer a short-cut (beyond our ratings and reports) for understanding our models.

Is VHC the next Google? The market’s current valuation seems to suggest it is that and much more.

Very few times in the last 15 years have I found a stock as expensive as VHC. The only comparable situation that comes to mind is Google (GOOG) at its IPO.

HIDDEN GEMS:

1. Our discounted cash flow analysis shows that DFS’s current valuation (stock price of $21.80) implies that the company’s profits will decline by 40% and never grow again.

2. Economic earnings are growing faster that reported accounting earnings.

3. Free cash flow of $2.8bn or 24% of its enterprise value during the last fiscal year.

HIDDEN GEM: ABT's current stock price (~$45 per share) implies the company’s profits will permanently decline by 20%. In other words, the market is not only giving no credit for future profit growth, it is predicting a significant (20%) decline in profits.

HIDDEN GEMS:

1. Our discounted cash flow analysis shows that APOL’s current valuation (stock price of $42.31) implies that the company’s profits will decline by 60% and never grow again.

2. Economic earnings are higher than reported accounting earnings.

3. Excess cash of $1,201mm or about 20% of its market cap