Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life.

Competitors are quickly encroaching on this tech stock’s market share, despite its impressive top-line growth. Now, through acquisitions and majority control, one competitor controls nearly half the market and has the ability to cut this firm’s market share. Risk of losing market share, when coupled with highly negative margins, unsustainable cash burn, and a soaring stock price mean Nutanix Inc. (NTNX: $32/share) is this week’s Danger Zone pick.

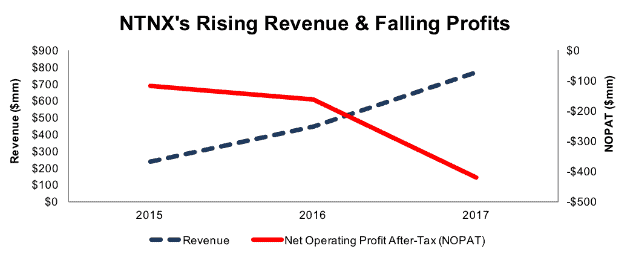

Rapidly Rising Revenue Leads to Rapidly Falling Profits

Since fiscal 2015, NTNX’s revenue has grown an impressive 78% compounded annually. At the same time, NTNX’s after-tax profit (NOPAT) has fallen from -$117 million to -$421 million, per Figure 1. The rapid deterioration in NOPAT comes from negative and declining margins. The company’s NOPAT margin fell from -48% in fiscal 2015 to -55% in fiscal 2017. Declining margins and inefficient capital use have dropped NTNX’s return on invested capital (ROIC) down from -65% in fiscal 2015 to -135%.

Figure 1: NTNX’s Revenue & NOPAT Since 2015

Sources: New Constructs, LLC and company filings

Compensation Plan Rewards Execs While Destroying Shareholder Value

We’ve previously warned of the limited and hidden disclosure red flags in IPOs, particularly with “emerging growth companies” such as Nutanix. These limited disclosures extend beyond the IPO date and allow firms to avoid disclosure of key executive compensation information.

Rather than provide specific and detailed metrics for performance bonuses and stock awards, NTNX provides a long list of metrics that could be used. Some of the metrics include attainment of research & development milestones, billings, earnings (which can include any calculation of earnings), growth in “stockholder value”, new product invention, revenue, and individual objectives such as peer reviews. Why not be more transparent?

While we cannot determine the exact metrics, we do not see ROIC or economic earnings, and we do see that execs receive bonuses despite destroying shareholder value. In fiscal 2016 and 2017, the three named executives in Nutanix’s proxy statement received upwards of $13 million in option and stock awards and $770,000 in bonuses under the executive bonus plan. Over this time, economic earnings, the true cash flows of the business, fell from -$184 million to -$458 million.

We’ve demonstrated through numerous case studies that ROIC, not revenue, EBIT, or individual objectives, is the primary driver of shareholder value creation. A recent white paper published by Ernst & Young also validates the importance of ROIC (see here: Getting ROIC Right) and the superiority of our data analytics. Without greater disclosures and changes to this compensation plan (e.g. emphasizing ROIC), investors should expect further value destruction.

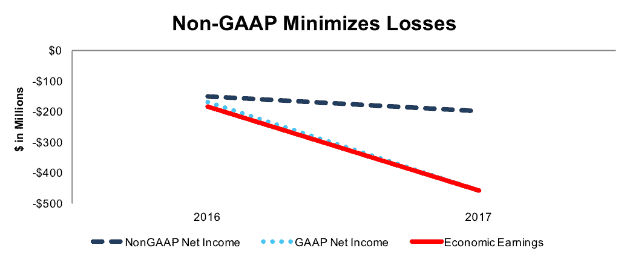

Non-GAAP Metrics Obscure Large Losses

Nutanix is yet another new technology firm that uses a multitude of non-GAAP metrics, such as non-GAAP gross margin, non-GAAP operating expenses, non-GAAP free cash flow, and non-GAAP net income to present adjusted metrics that distract from the true economics of the business. Our research digs deeper so our clients see through these misleading financial metrics. Below are some of the items Nutanix removes for its non-GAAP net income:

- Stock-based compensation expense

- Intangibles amortization expense

- Acquisition related costs

These adjustments have a large impact on the disparity between GAAP net income, non-GAAP net income, and economic earnings. In fiscal 2016, NTNX removed $20 million (4% of 2016 revenue) in stock-based compensation expense. In fiscal 2017, the company removed $231 million (30% of revenue) in stock-based compensation expense to calculate non-GAAP net income. Combined with other adjustments, NTNX reported fiscal 2017 non-GAAP net income of -$199 million. Per Figure 2, GAAP net income and economic earnings were -$458 million and declining at a much faster pace than non-GAAP net income.

Figure 2: NTNX’s Non-GAAP Metrics Minimize Declining Economic Earnings

Sources: New Constructs, LLC and company filings

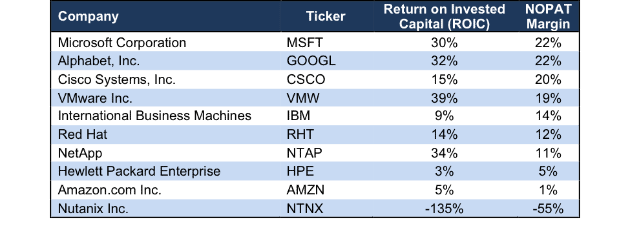

Negative Margins and Cash Flow Create Issues in a Competitive Industry

Nutanix provides enterprise cloud software that combines traditional servers, virtualization, and networking hardware/software into one integrated solution, also known as hyperconverged infrastructure (HCI). This market, along with the larger enterprise software market, is highly competitive. Nutanix’s main competitors include VMware (VMW), Cisco (CSCO), Dell/EMC, Red Hat (RHT), NetApp (NTAP), Hewlett Packard Enterprise (HPE), as well as public cloud providers Amazon (AMZN) and Google (GOOGL).

Despite ranking at or near the top in market share (market share is debated based on OEM hardware vs. software), Nutanix’s ROIC and NOPAT margin rank well below all competitors.

Figure 3: Nutanix’s NOPAT Margin Ranks Bottom of Competition

Sources: New Constructs, LLC and company filings

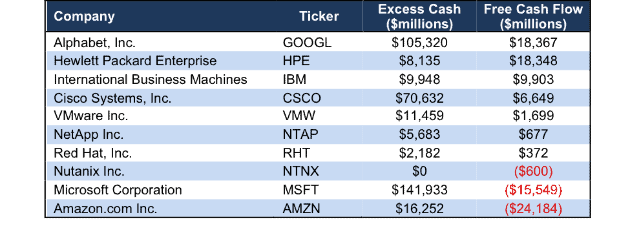

Beyond profit margins, Nutanix lacks the capital and the operational flexibility of its competition. Per Figure 4, Nutanix ranks near the bottom in regards to free cash flow, and dead last in terms of excess cash. While MSFT and AMZN have negative free cash flow, they also have loads of excess cash to support the business.

In a market characterized by rapid innovation and new technology, the ability to invest capital into product development can be the difference between having the best product offering and being left behind. Most alarming, and most detrimental to shareholders, is the fact that Nutanix cannot continue its cash burn much longer. Without the recently announced debt offering, Nutanix’s cash on the books would have supported the 2017 cash burn rate for just over six months. If cash burn continues at such a rapid pace, investors shouldn’t be surprised to see another debt offering and/or a shareholder dilution to raise additional capital in the next 18 months.

Figure 4: Nutanix Lacks Capital Resources to Compete Long-Term

Sources: New Constructs, LLC and company filings

Bull Case Ignores Competitors’ Market Share Gains and NTNX’s Troubling Cost Issues

Nutanix bulls will point to the firm’s growing market share and rapid revenue growth as reason to invest in the company. Many will also argue that with just a few cost controls/cuts, Nutanix could be a profitable firm. Each of these viewpoints not only ignores changes in the competitive landscape, but also the fact that revenue growth is slowing and projected to slow further, while costs continue to soar.

It’s important to note that market share can be difficult to track in the HCI market, as software can be installed on another firm’s hardware. To shed more light on this important topic, Aaron Rakers, a senior analyst at Wells Fargo, analyzed the IDC data not freely available to the public to provide more accurate market share values. His analysis provided key takeaways that could impact NTNX’s future:

- Nutanix is the market share leader when including Dell products running its software, with 34% of the market in 2017, up from 33% in 2016.

- VMware is quickly increasing its market share, which grew from 23% in 2016 to 32% in 2017.

- Dell EMC alone (not including products running Nutanix’s software) has a 17% market share, up from 16% the prior year.

This detailed market share analysis reveals that, while Nutanix is the market leader, Dell, because of its ownership of VMware, holds the majority of power in the industry.

When Dell, EMC, and VMware market shares are combined, and hardware running NTNX software is excluded, they control 49% of the HCI market. More troubling for NTNX bulls, since Dell bought VMware in 2016, VMWare’s market share has increased at a much faster pace than Nutanix.

With a controlling (and financial) interest in VMware, Dell could limit Nutanix’s growth potential by promoting its own VMware product in favor of Nutanix’s software. Such a decision would instantly impact NTNX’s top-line, as Dell accounted for 10% of NTNX billings in fiscal 2016 and 2017. More importantly, Dell could inhibit NTNX’s potential market share, which, when excluding Dell hardware, was just 21% in 2017, down from 22% in 2016.

Market share risk aside, Nutanix is seeing revenue growth slow despite spending heavily to enhance and promote its products. In fiscal 2017, revenue grew 72% year-over-year (YoY), which is down from 84% YoY in fiscal 2016. Fiscal 2018 revenue is expected to grow 45% YoY. Given the strength of its competition and market share threats, Nutanix is not in a position to cut costs and become profitable in the near future.

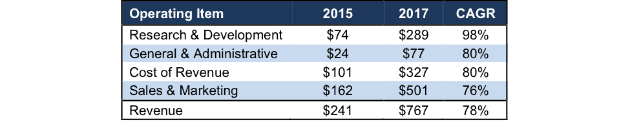

Per Figure 5, Nutanix’s research & development, general & administrative, and sales & marketing costs grew 98%, 80%, and 76% compounded annually from fiscal 2015-2017. Cost of revenue grew 80% compounded annually while revenue grew 78% compounded annually over the same time. Worse yet, Nutanix’s operating costs make up an increasingly larger percentage of revenue. In fiscal 2017, operating expenses were 113% of revenue, which is up from 107% of revenue in 2015.

Figure 5: NTNX’s Operating Expenses Growing Faster Than Revenue

Sources: New Constructs, LLC and company filings

Whatever you think about market share risk and costs growing faster than revenue, it’s hard to stomach Nutanix’s valuation. The expectations baked into NTNX’s price imply that Nutanix will immediately achieve profitability and increase its market share to nearly 100%. Details below.

NTNX’s Valuation Implies Beyond Optimistic Profit Growth

NTNX shares are up over 110% since their May 2017 lows while the S&P is up 18%. This rapid price appreciation has pushed NTNX to a level where the expectations baked into the stock price are not rooted in reality.

To justify its current price of $32/share, NTNX must immediately achieve NOPAT margins of 10% (slightly below the competitors’ average, which is boosted by other business lines) and grow revenue by 27% compounded annually for the next 12 years. Keep in mind, NTNX’s current NOPAT margin is -55%.

In this scenario, Nutanix generates nearly $13 billion in revenue 12 years from now. For reference, Grand View Research, a business intelligence market research provider, projects the entire HCI market will be $14 billion in 2024. So, the current valuation of NTNX implies it will have nearly 100% market share. This scenario also seems unlikely given that analysts estimate NTNX will grow revenue 15% in 2019, well below the 27% compounded annual rate assumed over a dozen years in this scenario.

Even if we assume NTNX can achieve a 10% NOPAT margin and grow revenue by 20% compounded annually for the next decade, the stock is worth only $15/share today – a 53% downside. This scenario assumes revenue grows at consensus estimates for the next five years and 14% each year thereafter. Each of these scenarios also assumes NTNX is able to grow revenue, NOPAT and FCF without increasing working capital or fixed assets. This assumption is unlikely but allows us to create best-case scenarios that demonstrate how high expectations embedded in the current valuation are. For reference, NTNX’s invested capital has grown on average $112 million (15% of 2017 revenue) over the past two years.

Is NTNX Worth Acquiring?

The largest risk to any bear thesis is what we call “stupid money risk”, which means an acquirer comes in and pays for NTNX at the current, or higher, share price despite the stock being overvalued. An acquisition could come from a larger tech firm looking to immediately expand its footprint in the HCI market. However, these firms would be better suited to develop their own software and out compete NTNX rather than imprudently allocate capital and destroy substantial shareholder value in an acquisition.

We show below how expensive NTNX remains even after assuming an acquirer can achieve significant synergies.

Walking Through the Acquisition Value Math

To begin, Nutanix has liabilities of which investors may not be aware that make it more expensive than the accounting numbers suggest.

- $495 million in outstanding employee stock options (10% of market cap)

- $52 million in off-balance-sheet operating leases (1% of market cap)

After adjusting for these liabilities, we can model multiple purchase price scenarios. Even in the most optimistic of scenarios, NTNX is worth less than its current share price.

Figures 6 and 7 show what we think Cisco (CSCO) should pay for NTNX to ensure it does not destroy shareholder value. In December 2017, CSCO ranked third in terms of market share in the HCI market, with NTNX having three times as large a share of the market. Acquiring NTNX would immediately boost CSCO’s presence in the HCI market and enable it to grow its software business while diversifying away from its legacy hardware business. However, there are limits on how much CSCO would pay for NTNX to earn a proper return, given the NOPAT or free cash flows (or lack thereof) being acquired.

Each implied price is based on a ‘goal ROIC’ assuming different levels of revenue growth. In both scenarios, the estimated revenue growth rate is 45% in year one and 15% in year two, which is the consensus estimate of NTNX’s revenue growth for the next two years. For the subsequent years, we use 15% in scenario one because it represents a continuation of next year’s expectations. We use 20% in scenario two because it assumes a merger with CSCO would create additional revenue opportunities through increased exposure to Cisco’s enterprise clients.

We conservatively assume that CSCO can grow NTNX’s revenue and NOPAT without spending anything on working capital or fixed assets beyond the original purchase price. We also assume NTNX immediately achieves a 14% NOPAT margin, which is the average of competitors in Figure 3. For reference, NTNX’s TTM NOPAT margin is -55%, so this assumption implies immediate improvement and allows the creation of a truly best-case scenario.

Figure 6: Implied Acquisition Prices for CSCO to Achieve 6% ROIC

Sources: New Constructs, LLC and company filings.

Figure 6 shows the ‘goal ROIC’ for CSCO as its weighted average cost of capital (WACC) or 6%. Even if NTNX can grow revenue by 23% compounded annually with a 14% NOPAT margin for the next five years, the firm is worth less than its current price of $32/share. It’s worth noting that any deal that only achieves a 6% ROIC would only be value neutral and not accretive, as the return on the deal would equal CSCO’s WACC.

Figure 7: Implied Acquisition Prices for CSCO to Achieve 15% ROIC

Sources: New Constructs, LLC and company filings.

Figure 7 shows the next ‘goal ROIC’ of 15%, which is CSCO’s current ROIC. Acquisitions completed at these prices would be truly accretive to CSCO shareholders. Even in the best-case growth scenario, the most CSCO should pay for NTNX is $10/share (70% downside to current valuation). Even assuming this best-case scenario, CSCO would destroy over $4 billion by purchasing NTNX at its current valuation. Any scenario assuming less than 23% compound annual growth in revenue would result in further capital destruction for CSCO.

Earnings and Guidance Miss Could Send Shares Lower

After IPO in September 2016, NTNX has met or beat top and bottom line expectations for five consecutive quarters. Earnings expectations have fluctuated wildly during this time. Consensus expectations for fiscal 2017 EPS ranged anywhere from -$1.38/share to -$1.49/share throughout calendar 2017. Similarly, expectations for fiscal 2018 have jumped from -$1.35/share to -$0.74/share over the past 12 months.

Company guidance has had more of a negative impact on the stock price than earnings beats. Despite beating top and bottom line expectations, NTNX provided below expected outlook in fiscal 2Q17 and the stock fell 26% in one day. In total, NTNX fell 53% in the two months following the earnings release.

Given the heightened competition and growing market share of firms like VMware and Dell/EMC, another disappointing guidance or earnings miss could be near. Should such a miss occur, shares could see a fall similar to fiscal 2Q17. While we don’t attempt to predict exactly when the market will recognize the disconnect between expectations and reality, the ensuing share collapse could hurt investors’ portfolios.

Insider Trading is Minimal While Short Interest is Rising

Over the past 12 months, 55.5 million insider shares have been purchased and 52.7 million have been sold for a net effect of 2.8 million insider shares purchased. These sales represent 2% of shares outstanding.

Short interest is currently 7.9 million shares, which equates to 5% of shares outstanding and 2.8 days to cover. Short interest has grown nearly 48% since February 2017, which would seem to imply we’re not the only ones who recognize the issues facing NTNX and its lofty valuation.

Auditable Impact of Footnotes & Forensic Accounting Adjustments[1]

Our Robo-Analyst technology enables us to perform forensic accounting with scale and provide the research needed to fulfill fiduciary duties. In order to derive the true recurring cash flows, an accurate invested capital, and an accurate shareholder value, we made the following adjustments to Nutanix’s 2017 10-K:

Income Statement: we made $37 million of adjustments, with a net effect of removing $37 million in non-operating expense (5% of revenue). We made no non-operating income adjustments and $37 million in non-operating expenses. You can see all the adjustments made to NTNX’s income statement here.

Balance Sheet: we made $130 million of adjustments to calculate invested capital with a net decrease of $24 million. One of the largest adjustments was $52 million in off balance sheet operating leases. This adjustment represented 15% of reported net assets. You can see all the adjustments made to NTNX’s balance sheet here.

Valuation: we made $547 million of adjustments with a net effect of decreasing shareholder value by $547 million. There were no adjustments that increased shareholder value. The largest adjustment to shareholder value was $495 million in outstanding employee stock options. This adjustment represents 10% of NTNX’s market cap.

Unattractive Funds That Hold NTNX

The following funds receive our Unattractive-or-worse rating and allocate significantly to Nutanix Inc.

- Professionally Managed Hodges Fund (HDPIX) – 4.1% allocation and Very Unattractive rating

- Professionally Managed Hodges Small Cap Fund (HDSIX) – 2.0% allocation and Very Unattractive rating

- Linde Hansen Contrarian Value Fund (LHVAX) – 3.1% allocation and Very Unattractive rating

This article originally published on February 5, 2018.

Disclosure: David Trainer and Kyle Guske II receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] Ernst & Young’s recent white paper, “Getting ROIC Right”, proves the superiority of our research and analytics.

Click here to download a PDF of this report.

Photo Credit: Manuel (Pexels)