Nine new stocks make March’s Exec Comp Aligned with ROIC Model Portfolio, available to members as of March 12, 2021.

Recap from February’s Picks

Our Exec Comp Aligned with ROIC Model Portfolio (+1.8%) outperformed the S&P 500 (-0.8%) from February 12, 2021 through March 10, 2021. The best performing stock in the portfolio was up 14%. Overall, nine out of the 15 Exec Comp Aligned with ROIC Stocks outperformed the S&P from February 12, 2021 through March 10, 2021.

More reliable & proprietary fundamental data, proven in The Journal of Financial Economics, drives our research. Our proprietary Robo-Analyst technology[1] scales our forensic accounting expertise (featured in Barron’s) across thousands of stocks[2] to produce an unrivaled database of fundamental data.

This Model Portfolio only includes stocks that earn an Attractive or Very Attractive rating and align executive compensation with improving ROIC. We think this combination provides a uniquely well-screened list of long ideas because return on invested capital (ROIC) is the primary driver of shareholder value creation.

New Stock Feature for March: Johnson Outdoors Inc. (JOUT: $149/share)

Johnson Outdoors (JOUT) is the featured stock in March’s Exec Comp Aligned with ROIC Model Portfolio.

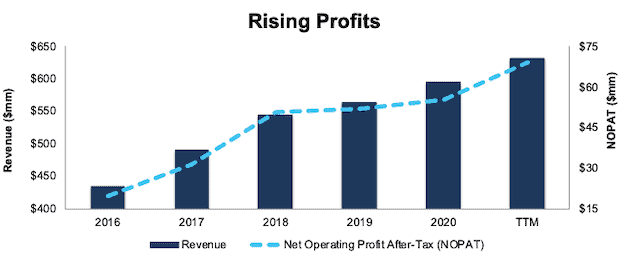

Johnson Outdoors has grown revenue by 8% compounded annually and net operating profit after tax (NOPAT) by 29% compounded annually since fiscal 2016, per Figure 1. NOPAT margin increased from 5% in fiscal 2016 to 11% over the trailing twelve-month period (TTM).

Figure 1: Johnson Outdoors’ NOPAT Growth: 2016–TTM

Sources: New Constructs, LLC and company filings

Performance-Based Pay Properly Incentivizes Executives

Johnson Outdoors’ executive compensation plan aligns executives’ interests with shareholder’s interests by tying compensation to return on invested capital (ROIC). Apart from base salaries and annual cash incentives, Johnson Outdoors’ executives receive long-term compensation in the form of performance-based restricted stock units which can be reduced if the business does not meet a minimum average ROIC target.

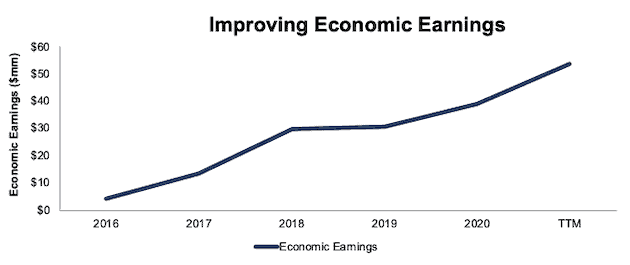

Johnson Outdoors’ inclusion of ROIC as an executive compensation metric has helped drive shareholder value creation and economic earnings, per Figure 2. Johnson Outdoors’ ROIC has improved from 6% in fiscal 2016 to 19% TTM while its economic earnings grew significantly from $4 million to $54 million over the same time.

Figure 2: Johnson Outdoors’ Economic Earnings: 2016–TTM

Sources: New Constructs, LLC and company filings

JOUT Is Undervalued

At its current price of $149/share, JOUT has a price-to-economic book value (PEBV) ratio of 0.8. This ratio means that the market expects Johnson Outdoors’ NOPAT to permanently decline by 20%. This expectation seems overly pessimistic for a firm that has grown NOPAT by 22% compounded annually over the past decade.

Even if Johnson Outdoors’ NOPAT margin falls to 7% (six-year average, compared to 11% in TTM) and the firm grows revenue by 7% (equal to its five-year CAGR from fiscal 2015-2020) compounded annually over the next 10 years, the stock is worth $191/share today – a 28% upside. See the math behind this reverse DCF scenario. In this scenario, Johnson Outdoors’ NOPAT would grow just 4% compounded annually over the next decade, or well below the NOPAT growth achieved during the prior decade.

Critical Details Found in Financial Filings by Our Robo-Analyst Technology

Fact: we provide more reliable fundamental data and earnings models – unrivaled in the world.

Proof: Core Earnings: New Data & Evidence, forthcoming in The Journal of Financial Economics.

Below are specifics on the adjustments we make based on Robo-Analyst findings in Johnson Outdoors’ 10-K and 10-Q:

Income Statement: we made $6 million of adjustments, with a net effect of removing $70 thousand in non-operating expenses (<1% of revenue).You can see all the adjustments made to Johnson Outdoors’ 2020 income statement here.

Balance Sheet: we made $358 million of adjustments to calculate 2020 invested capital with a net decrease of $104 million. One of the largest adjustments was $183 million (41% of reported net assets) in excess cash. You can see all the adjustments made to Johnson Outdoors’ balance sheet here.

Valuation: we made $206 million of adjustments with a net effect of increasing shareholder value by $124 million. Apart from total debt, and excess cash noted above, the most notable adjustment to shareholder value was $3 million in deferred compensation. This adjustment represents <1% of Johnson Outdoors’ market cap. See all adjustments to Johnson Outdoors’ valuation here.

This article originally published on March 15 2021.

Disclosure: David Trainer, Kyle Guske II, Alex Sword, and Matt Shuler receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] Harvard Business School features our research automation technology in the case Disrupting Fundamental Analysis with Robo-Analysts.

[2] See how our models overcome flaws in Bloomberg and Capital IQ’s (SPGI) analytics in the detailed appendix of this paper.