We think investors’ expectation for the fiduciary standard is here to stay no matter what the official rules say -- and those investors will increasingly demand that their advisers apply to their non-retirement accounts too.

The All Cap Value style ranks fifth out of the twelve fund styles as detailed in our 4Q16 Style Ratings for ETFs and Mutual Funds report. Last quarter, the All Cap Value style ranked fifth as well.

At the beginning of the third quarter of 2016, only the Large Cap Blend style earns an Attractive-or-better rating. Our style ratings are based on the aggregation of our fund ratings for every ETF and mutual fund in each style.

The big banks still have significant advantages. Their brand names, financial capital, advisor networks, and large client bases give them the opportunity to leverage the innovations of startups and become the biggest winners in this new wealth management model.

We calculate invested capital in two mathematically equivalent ways: financing and operating approach. Figure 1 shows the basic calculations. On page 2, we share the complete calculations for specific companies.

Thesis: Management can boost the market value of American Express in the amounts below[1] by aligning the firm’s strategy and performance compensation with real cash flows or what we call return on invested capital (ROIC).

It’s incredible that corporate executives and the market as a whole continue to depend on such flawed numbers when we already have a measure that is clearly linked with value creation: return on invested capital (ROIC).

In the search for safe investments in today’s volatile markets, investors should focus on companies that have a history of creating shareholder value, the ability to earn quality returns on capital, and an undervalued stock. This week’s Long Idea, Wells Fargo & Company (WFC) not only fits the description of a safe investment, but its shares are also greatly undervalued.

The Dow Jones Industrial Average has a deserved reputation of only housing the best-of-the-best blue chip stocks. Only the oldest, largest, and most profitable companies are included in the index,

Trading stocks sometimes feels like a very modern phenomenon, so it’s easy to forget that some of the companies we’re investing in go back a century or more.

Value investing is a tried and tested approach that has worked wonders for investors in the past. However, in today's world, executing this strategy can be a daunting task, given the complexity of the annual reports that companies file. Even professional investors have a tough time understanding the profitability and valuation of companies due to the lengthy and convoluted filings they receive. With stocks becoming more volatile and earnings estimates less precise, investors could be misled into thinking they're making a wise investment when, in fact, there's another side to the coin they've not seen.

As regulators dole out punishments that fit the crimes, they are finally closing many of the illegal trading loopholes that have driven so much of Wall Street profits over the past decade.

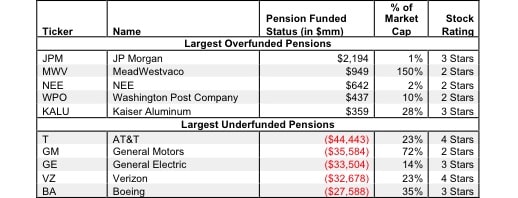

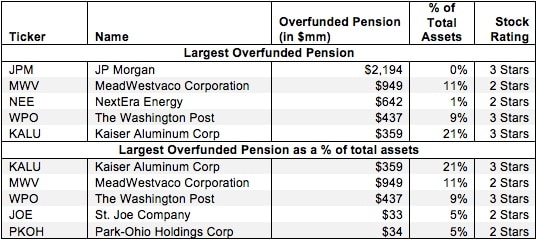

Companies with underfunded pensions will likely need to divert a greater amount of future cash flows away from shareholders to make up the funding gap. An accurate analysis of shareholder value should include the net funded status of pensions.

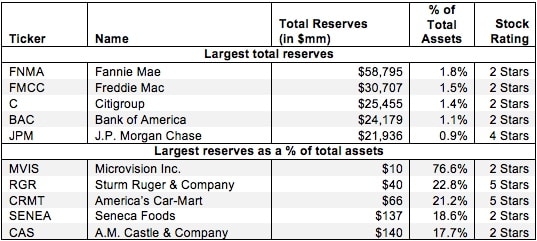

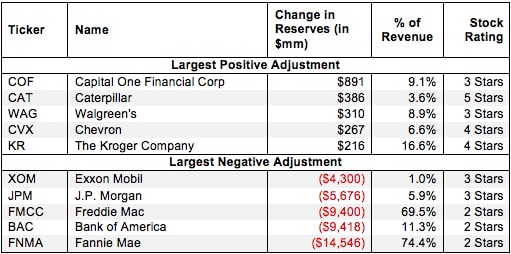

Reported assets don’t tell the whole story of the capital invested in a business. Accounting rules provide numerous loopholes that companies can exploit to hide issues and obscure the true amount of capital invested in a business over its life.

Reported earnings don’t tell the whole story of a company’s profits. They are based on accounting rules designed for debt investors, not equity investors, and are manipulated by companies to manage earnings. Only economic earnings provide a complete and unadulterated measure of profitability.

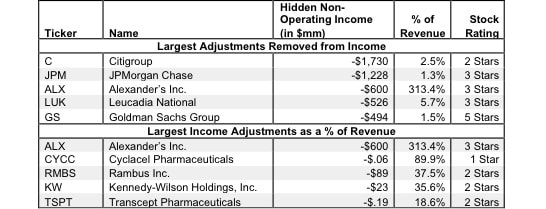

Non-operating items in operating income are unusual gains that don’t appear on the income statement because they are bundled in other line items. Without careful footnotes research, investors would never know that these non-recurring income items distort GAAP numbers by artificially raising operating earnings.

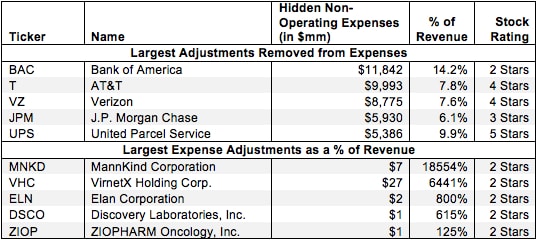

Non-operating expenses are unusual charges that don’t appear on the income statement because they are bundled in other line items. Without careful footnotes research, investors would never know that these non-recurring expenses distort GAAP numbers by lowering operating earnings.