We found interesting footnote disclosures in the filings of Fidelity National Information Services and other companies last week during The Real Earnings Season.

This report red flags the firms with the most underfunded pensions and the most aggressive assumptions for returns they expect to earn on the pension assets.

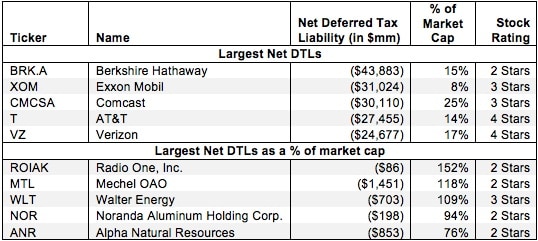

Most public companies should benefit from the new tax law and some of the biggest winners will be companies with large deferred tax liabilities (DTLs).

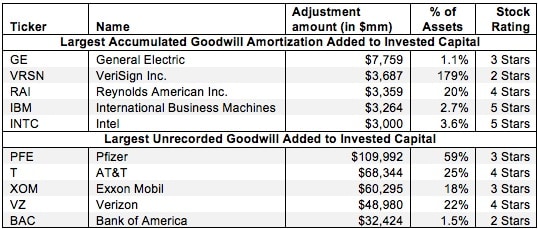

We calculate invested capital in two mathematically equivalent ways: financing and operating approach. Figure 1 shows the basic calculations. On page 2, we share the complete calculations for specific companies.

At the beginning of the third quarter of 2015, only the Consumer Staples sector earns an Attractive-or-better rating. Sector ratings are based on the aggregation of our fund ratings for every ETF and mutual fund in each sector.

The Dow Jones Industrial Average has a deserved reputation of only housing the best-of-the-best blue chip stocks. Only the oldest, largest, and most profitable companies are included in the index,

The Energy sector ranks seventh out of the 10 sectors this month and receives our Dangerous rating. The Energy sector as a whole greatly underperformed the S&P 500 in 2014, returning -10% to the S&P’s 12%.

Value investing is a tried and tested approach that has worked wonders for investors in the past. However, in today's world, executing this strategy can be a daunting task, given the complexity of the annual reports that companies file. Even professional investors have a tough time understanding the profitability and valuation of companies due to the lengthy and convoluted filings they receive. With stocks becoming more volatile and earnings estimates less precise, investors could be misled into thinking they're making a wise investment when, in fact, there's another side to the coin they've not seen.

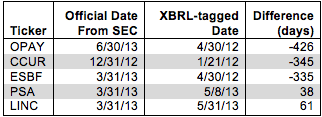

The potential utility of XBRL as a tool for regulators to fight fraud and investors to better analyze companies makes its numerous flaws that much more of a shame. I can only hope that the SEC realizes the value of XBRL and makes a commitment to ensuring the accuracy and validity of XBRL data.

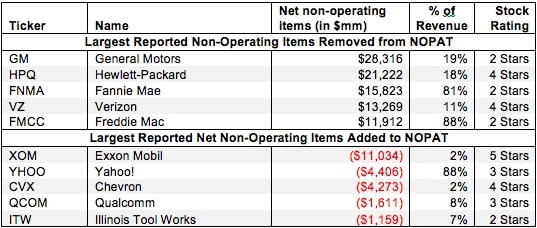

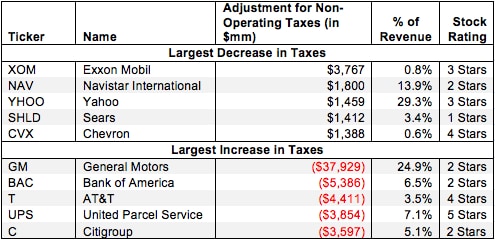

Income statement adjustments include financing items like interest expense/income, preferred dividends and minority interest income. These items are related to the financing of a company’s operations, not the operations themselves. We always calculate NOPAT on an unlevered basis.

We subtract net deferred tax liabilities (DTLs minus DTAs) from our calculation of shareholder value as they are real future cash obligations that limit the amount of money available for distribution to shareholders.

Reported earnings don’t tell the whole story of a company’s profits. They are based on accounting rules designed for debt investors, not equity investors, and are manipulated by companies to manage earnings. Only economic earnings provide a complete and unadulterated measure of profitability.

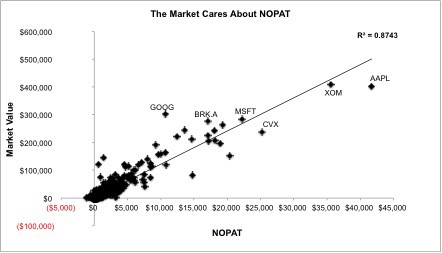

This article provides some empirical evidence behind my putting Apple (AAPL) in the Danger Zone last week because its return on invested capital (ROIC) is outrageously high. That fact underscores why valuing this company or any other with the expectation that such a high ROIC was sustainable would be a mistake.