We closed this Danger Zone pick on September 24, 2024. A copy of the associated Position Close report is here.

Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life.

After nearly 30 years of operating in a relatively stable industry, this firm’s profits, ROIC, and margins have all fallen in recent years as competition has flooded the market. However, the stock’s valuation has not adjusted to reflect new competitive pressures or the rapidly deteriorating fundamentals. This week’s Danger Zone pick is Pegasystems Inc. (PEGA: $50/share).

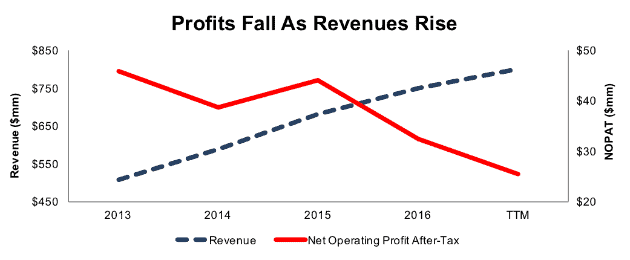

Strong Revenue Growth Obscures Falling Profits

Since 2013, PEGA’s revenue has grown 14% compounded annually. Over the same time, its after-tax profit (NOPAT) has fallen 11% compounded annually to $33 million in 2016 and $25 million over the last twelve months (TTM), per Figure 1. The disconnect between revenue and profits comes from rapidly declining margins. The company’s NOPAT margin fell from 9% in 2013 to 3% TTM. Declining margins and inefficient capital use have knocked PEGA’s return on invested capital (ROIC) down from a once impressive 22% in 2013 to 9% TTM.

Figure 1: PEGA’s NOPAT & Revenue Since 2013

Sources: New Constructs, LLC and company filings

Compensation Plan Allows Execs to Get Paid While Destroying Shareholder Value

Pegasystems’ executive compensation plan fails to properly align executives’ interests with shareholders’ interests. The misalignment helps drives the profit decline shown in Figure 1 and enables executives to earn large bonuses while shareholder value is destroyed. Executives’ annual bonuses are tied to many different metrics, most of which fail to measure shareholder value creation. The metrics used include revenue, license signings or bookings, operating income, and qualitative goals approved by the board of directors. Long-term equity incentives are awarded via stock options and restricted stock units. Equity awards are given within the context of each executive’s total compensation based on the value associated with their job.

The bottom line is that executives are incentivized to achieve revenue growth, at any cost, and as they earn nice bonuses, PEGA’s economic earnings have fallen from $32 million in 2013 to $5 million TTM.

We’ve demonstrated through numerous case studies that ROIC, not revenue, bookings, or license signings, is the primary driver of shareholder value creation. A recent white paper published by Ernst & Young also validates the importance of ROIC (see here: Getting ROIC Right) and the superiority of our data analytics. Without major changes to this compensation plan (e.g. emphasizing ROIC), investors should expect further value destruction.

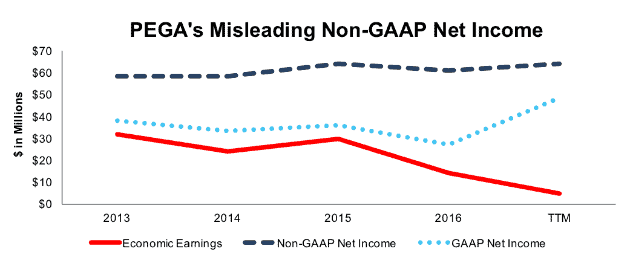

Non-GAAP Metrics Hide Falling Profitability

Pegasystems is among a long list of firms that use non-GAAP metrics, such as non-GAAP revenue and non-GAAP net income, to present rising “profits” while economic earnings decline. Our research digs deeper so our clients see through the illusory numbers. Below are some of the items Pegasystems removes to calculate its non-GAAP net income:

- Stock-based compensation

- Amortization of intangible assets

- Acquisition related costs

- Restructuring costs

These adjustments have a large impact on the disparity between GAAP net income, non-GAAP net income, and economic earnings. Over the TTM period and 2016, PEGA removed $50 million (over 100% of TTM GAAP net income) and $41 million (over 150% of 2016 GAAP net income), respectively, in stock-based compensation expense to calculate non-GAAP net income. Combined with other adjustments, PEGA reported TTM non-GAAP net income of $64 million. Per Figure 2, GAAP net income was $49 million and economic earnings were $5 million TTM.

Figure 2: PEGA’s Non-GAAP Metrics Mask Declining Economic Earnings

Sources: New Constructs, LLC and company filings

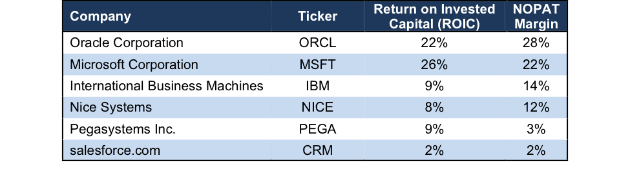

Lagging Margins are Troublesome in A Highly Competitive & Fragmented Industry

Pegasystems operates in the highly competitive industry of customer relationship management, or CRM. Its software provides marketing, sales, services, and operational applications to businesses. This industry consists of a few large providers, and numerous smaller firms competing in niche areas. The biggest competition comes from household names such as salesforce (CRM), SAP, Microsoft (MSFT), Oracle (ORCL), and International Business Machines (IBM). Other competitors include Infor, NetSuite (acquired by Oracle in 2016), SugarCRM, Insightly, and Zoho.

One defining characteristic of the large competitors (excluding salesforce) is high ROIC and NOPAT margins. Per Figure 3, PEGA’s ROIC and NOPAT margin rank near the bottom of this group. The only competitor with lower margins is Salesforce, a previous Danger Zone pick, which has taken the “Amazon approach” and foregone profitability to grow market share. With lower margins and less resources to subsidize losses, Pegasystems is at a competitive disadvantage.

The firms at the top of Figure 3 have the ability to pour large amounts of capital into their CRM systems and remain profitable via their other cash generating business lines. PEGA’s late transition from traditional licensing deals to more recent “software-as-a-service” deals gave competition a leg up that will be difficult to overcome.

Figure 3: Pegasystems’ NOPAT Margin Lags Peers

Sources: New Constructs, LLC and company filings

Bull Case Ignores PEGA’s Weak Competitive Position and Uphill Battle to Match Competition

Any bull of PEGA must believe it can achieve what numerous other software companies have been unable to do: transition from a perpetual license/maintenance business model into a subscription/recurring revenue model. Unfortunately for investors, PEGA’s transition coincides with the falling profits noted in Figure 1 above. Since 2013, term licenses and cloud revenue have increased from 15% of revenue to 23% in 2016. The growth in these areas has come at the expense of perpetual licenses and services and training.

Figure 4: PEGA’s Expenses Outpacing Revenue Growth

Sources: New Constructs, LLC and company filings

As the transition continues, PEGA must differentiate itself from the litany of large CRM providers, which Forrester notes, “can just about tick every box” when it comes to features. Furthermore, PEGA’s is attacking the industry from a smaller market share than the four main providers. Per IDC, Salesforce’s market share sits at nearly 18%, Oracle around 9%, and SAP around 7%. Older reports from Gartner list Microsoft as the fourth largest CRM provider, Adobe fifth, and IBM sixth.

The challenges in gaining market share, particularly in an industry led by Salesforce (serial acquirer, willing to operate at a loss) are the heavy spending required to advertise, promote, and convince clients of the value of your platform. Such spending can be seen in PEGA’s operating expense growth. Per Figure 4 above, research & development, general & administrative, selling & marketing, and cost of revenues have all grown faster than revenue since 2013. Despite heavy spending, Forrester noted in its analysis in late 2016 that Pegasystems customers complained about a lack of trained resources and Gartner found in 2017 that it “remains a challenge to integrate Pegasystems with real-time data sources.”

Perhaps most alarming to any bull case is that PEGA’s valuation doesn’t reflect the challenges the company will face moving forward. Instead, the expectations embedded in the current stock price imply that PEGA will immediately begin growing profits and for many years into the future.

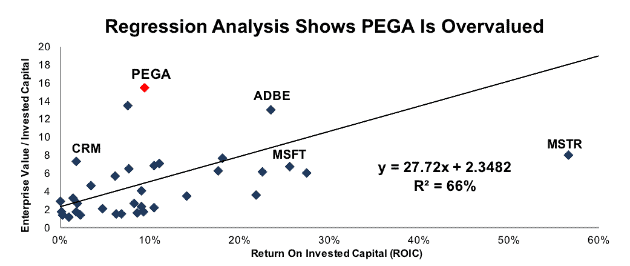

PEGA’s Valuation Implies Overly Optimistic Profit Growth

PEGA has risen 41% year-to-date, while the S&P is up 18% over the same time. Shares have fallen 10% in the past month though as earnings missed both top and bottom line expectations. This recent drop could be just the beginning as investors realize the disconnect between the company’s current financial performance and the significantly higher profits implied by the stock price.

Figure 5 shows PEGA and its application software peers compared on the basis of ROIC and enterprise value divided by invested capital (a cleaner version of price to book). As you can see, ROIC explains 66% of the changes in valuation for PEGA’s peers.

Figure 5: ROIC Explains 66% of Valuation for Application Software Peers

Sources: New Constructs, LLC and company filings

PEGA stands out as an outlier in Figure 5 and trades at a significant premium to its peers. If the stock were to trade a parity with the peer group, it would be $15/share – 69% below the current stock price. Given the firm’s subpar and declining fundamentals, it should be clear PEGA does not deserve such a premium valuation.

Our discounted cash flow model quantifies the expectations baked into that premium valuation. To justify its current price of $50/share, PEGA must achieve 6% NOPAT margins (double the 3% TTM margin) and grow NOPAT by 20% compounded annually for the next 15 years. This scenario seems overly optimistic given that PEGA’s NOPAT has fallen 11% compounded annually over the past four years.

Even if we assume PEGA can slow expense growth and achieve a 6% NOPAT margin and grow NOPAT by 14% compounded annually for the next decade, the stock is still worth only $17/share today – a 66% downside.

Each of these scenarios also assumes PEGA is able to grow revenue, NOPAT and FCF without increasing working capital or investing in fixed assets. This assumption is unlikely but allows us to create optimistic scenarios that demonstrate just how high expectations embedded in the current valuation really are. For reference, PEGA’s invested capital has grown $22 million on average (3% of 2016 revenue) each year for the past five years.

Is PEGA Worth Acquiring?

The largest risk to any bear thesis is what we call “stupid money risk”, which means an acquirer comes in and pays for PEGA at the current, or higher, share price despite the stock being overvalued. Pegasystems’ CEO’s disinterest in being acquired would make a takeover less likely.

He noted in 2010 he would “rather eat sand” when asked whether he would entertain a takeover by a large vendor like IBM. Then in late 2016, via leaked emails, it was released that Salesforce could be interested in acquiring Pegasystems. Via a public announcement and other comments, the CEO noted that Pegasystems is “not remotely interested.” A spokeswoman noted that Pegasystems aims to grow the company “on our own terms” as well.

Given the CEO’s stance, his position as majority shareholder, and PEGA’s lofty valuation, competitors would be better suited to use their competitive advantage to out compete PEGA rather than imprudently allocate capital and destroy substantial shareholder value in an acquisition.

However, we can still model just how expensive PEGA remains even after assuming an acquirer can achieve significant synergies.

Walking Through the Acquisition Value Math

To begin, Pegasystems has liabilities of which investors may not be aware that make it more expensive than the accounting numbers suggest.

- $147million in outstanding employee stock options (4% of market cap)

- $65 million in off-balance-sheet operating leases (2% of market cap)

After adjusting for these liabilities, we can model multiple purchase price scenarios. Even in the most optimistic of scenarios, PEGA is worth less than its current share price.

Figures 6 and 7 show what we think Microsoft (MSFT) should pay for PEGA to ensure it does not destroy shareholder value. MSFT competes with PEGA with its Microsoft Dynamics platform and purchasing PEGA could not only eliminate a smaller competitor but also bring new technologies, such as PEGA’s predictive engagement, in house. However, there are limits on how much MSFT would pay for PEGA to earn a proper return, given the NOPAT or free cash flows (or lack thereof) being acquired.

Each implied price is based on a ‘goal ROIC’ assuming different levels of revenue growth. In both scenarios, the estimated revenue growth rate is 8% in year one and 10% in year two, which is the consensus estimate of PEGA’s revenue growth for the next two years. For the subsequent years, we use 10% in scenario one because it represents a continuation of next year’s expectations. We use 15% in scenario two because it assumes a merger with MSFT would create revenue synergies thorough increased exposure to MSFT’s larger market share.

We conservatively assume that MSFT can grow PEGA’s revenue and NOPAT without spending anything on working capital or fixed assets beyond the original purchase price. We also assume PEGA immediately achieves a 12.5% NOPAT margin, which is the average of MSFT’s and PEGA’s current NOPAT margin. For reference, PEGA’s TTM NOPAT margin is 3%, so this assumption implies immediate improvement and allows the creation of a truly best-case scenario.

Figure 6: Implied Acquisition Prices for MSFT To Achieve 7% ROIC

Sources: New Constructs, LLC and company filings.

Figure 6 shows the ‘goal ROIC’ for MSFT as its weighted average cost of capital (WACC) or 7%. Even if PEGA can grow revenue by 13% compounded annually with a 12.5% NOPAT margin for the next five years, the firm is worth much less than its current price of $50/share. It’s worth noting that any deal that only achieves a 7% ROIC would be only value neutral and not accretive, as the return on the deal would equal MSFT’s WACC.

Figure 7: Implied Acquisition Prices for MSFT To Achieve 26% ROIC

Sources: New Constructs, LLC and company filings.

Figure 7 shows the next ‘goal ROIC’ of 26%, which is MSFT’s current ROIC. Acquisitions completed at these prices would be truly accretive to MSFT shareholders. Even in the best-case growth scenario, the most MSFT should pay for PEGA is $8/share (85% downside to current valuation). Even assuming this best-case scenario, MSFT would destroy over $3 billion by purchasing PEGA at its current valuation. Any scenario assuming less than 13% compound annual growth in revenue would result in further capital destruction for MSFT.

Another Earnings Disappointment Could Send Shares Lower

Expectations for PEGA’s earnings have been significantly cut throughout 2017. 2017 EPS expectations have fallen 34% since the beginning of the year. Similarly, 2018 EPS expectations have fallen 45% since the end of 2016. Despite the cuts in consensus estimates, PEGA continues to miss lowered expectations while the stock rises. The company has reported EPS below consensus in three of the past four quarters. In two of those quarters, the stock reacted as one would expect.

- 2Q17 – missed top and bottom line expectations. PEGA fell 11% the following day

- 3Q17 – missed top and bottom line expectations. PEGA fell 9% the week of earnings

While expectations have been lowered, the stock still reflects overly optimistic profit growth, as highlighted above. If PEGA fails to meet a lowered bar again, the stock could fall, as investors realize the company’s software is struggling to gain market share in a highly competitive market. Competitor success could also weigh on Pegasystems shares. If Microsoft, Oracle, or even Salesforce continue to report impressive gains in their CRM business, investors could rotate out of PEGA and into more “growth oriented” tech names.

While we don’t attempt to predict exactly when the market will recognize the disconnect between expectations and reality, we know the impact of failing to meet expectations can be dangerous to investors’ portfolios. After a large rise in price throughout 2017, PEGA represents an unfavorable risk/reward tradeoff.

Insider Trading is Minimal While Short Interest is Rising

Over the past 12 months, five thousand insider shares have been purchased and 360 thousand have been sold for a net effect of 355 thousand insider shares sold. These sales represent less than 1% of shares outstanding.

Short interest is currently 1.5 million shares, which equates to 2% of shares outstanding and two days to cover. There has been a jump in short interest this year, as the number of shares sold short has nearly doubled since June 2017. Growing short interest would seem to imply we’re not the only ones who recognize the issues facing PEGA and its lofty valuation.

Auditable Impact of Footnotes & Forensic Accounting Adjustments[1]

Our Robo-Analyst technology enables us to perform forensic accounting with scale and provide the research needed to fulfill fiduciary duties. In order to derive the true recurring cash flows, an accurate invested capital, and an accurate shareholder value, we made the following adjustments to Pegasystems 2016 10-K:

Income Statement: we made $23 million of adjustments with a net effect of removing $5 million in non-operating expense (1% of revenue). We removed $14 million related to non-operating expenses and $9 million related to non-operating income. See all the adjustments made to PEGA’s income statement here.

Balance Sheet: we made $288 million of adjustments to calculate invested capital with a net decrease of $110 million. The most notable adjustment was $70 million (19% of reported net assets) related to deferred tax assets. See all adjustments to PEGA’s balance sheet here.

Valuation: we made $366 million of adjustments with a net effect of decreasing shareholder value by $58 million. The largest adjustment to shareholder value was $147 million in outstanding employee stock options. This adjustment represents 4% of PEGA’s market cap.

Unattractive Funds That Hold PEGA

The following funds receive our Unattractive-or-worse rating and allocate significantly to Pegasystems.

- Ranger Small Cap Fund (RFISX) – 4.3% allocation and Very Unattractive rating

- Transamerica Small Cap Growth (ASGTX) – 4.1% allocation and Very Unattractive rating

- Rice Hall James Small Cap Portfolio (RHJMX) – 2.6% allocation and Unattractive rating

- Carillon Scout Small Cap Fund (CSSQX) – 2.1% allocation and Unattractive rating

This article originally published on December 4, 2017.

Disclosure: David Trainer and Kyle Guske II receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] Ernst & Young’s recent white paper, “Getting ROIC Right”, proves the superiority of our research and analytics.

Click here to download a PDF of this report.

Photo Credit: Nejc Košir (Pexels)