We published an update on this Long Idea on August 11, 2021. A copy of the associated Earnings Update report is here.

Despite the micro-bubble in specific tech stocks, investors can still find value in the sector. This tech firm has a long history of profit growth, prudent capital stewardship, and an undervalued stock. It’s business model creates more value than peers. Add in its position in multiple fast-growing markets and its clear why Insight Enterprises (NSIT: $54/share) is this week’s Long Idea.

Reported Income Understates NSIT’s Fundamentals

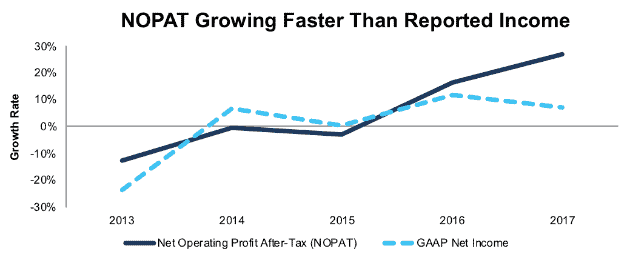

Investors who only analyze reported net income might think that NSIT’s profit growth stalled in 2017, when, in fact, NSIT’s profit growth is increasing.

In 2017, the company’s net income included multiple non-operating expenses (some hidden in the MD&A and some reported directly on the income statement) that lowered its reported earnings. As reported on page 24 of NSIT’s 2017 10-K, operating income includes $2.5 million in after-tax transaction costs, $7 million in after-tax severance costs, and $13 million in after-tax income tax expense related to U.S. tax reform.

Combined, we removed unusual charges of $44 million, or 49% of NSIT’s reported net income. By removing these non-recurring charges, we see that NSIT’s after-tax operating profit (NOPAT) increased 27% year-over-year (YoY) in 2017 while GAAP net income grew just 7% YoY. Per Figure 1, NSIT’s NOPAT (+16%) grew faster than GAAP net income (+12%) in 2016 as well.

Even better, economic earnings, which take into account cost of capital and changes to the balance sheet, grew 176% and 100% YoY in 2016 and 2017 respectively.

Figure 1: NSIT’s NOPAT & Net Income Growth Rate Since 2013

Sources: New Constructs, LLC and company filings

NSIT has improved its profitability through margin expansion and intelligent capital allocation. NOPAT margins have improved from 1.6% in 2015 to 2.1% over the trailing twelve months (TTM). At the same time, average invested capital turns, a measure of balance sheet efficiency, have averaged 4.4 over the past five years, and are currently 4.4 in the TTM period (well above the 1.9 average of competition under coverage).

Rising margins and efficient capital use have improved NSIT’s return on invested capital (ROIC) from 7% in 2015 to 9% TTM. The firm has also generated positive free cash flow in nine of the past 10 years, to the tune of $338 million (18% of market cap) in cumulative FCF over the past decade.

Acquisitions Have Grown Company While Not Destroying Shareholder Value

For a value-add retailer such as NSIT, which combines traditional hardware/software sales with consulting and IT expertise to create custom solutions, acquisitions can increase its service offerings and revenues. However, we know that in most cases acquisitions fail to create value for shareholders. We’ve emphasized in the past that big acquisitions can be accretive to GAAP earnings but actually destroy shareholder value (despite executives still getting bonuses). Not all acquisitions have to destroy shareholder value though, especially when executives’ incentives are properly aligned with shareholders’ interests.

Insight has shown a rare ability to create value through acquisitions. Insight has spent ~$318 million on acquisitions since 2015 (~19% of invested capital) while improving its ROIC from 7% to 9%. These acquisitions have expanded NSIT’s geographical scale, its expertise of existing services, and breadth of services offered to customers. Better yet, these acquisitions give the company greater scale and leverage versus suppliers, which we’ll discuss later.

Exec Comp Drives Value-Creating Acquisitions and Deployment of Capital

NSIT’s ability to improve its ROIC and create shareholder value through acquisitions is no coincidence. The company directly incentivizes executives to focus on intelligent capital allocation by including ROIC as one of the metrics used to determent executive pay. In 2017, 3-year average ROIC was the sole metric used to determine performance based restricted stock units, which make up 60% of long-term incentives.

This focus on improving ROIC aligns the interests of executives and shareholders and helps ensure prudent stewardship of capital[1]. There is also a strong correlation between improving ROIC and increasing shareholder value, a fact highlighted in our recent article “CEO’s That Focus on ROIC Outperform.”

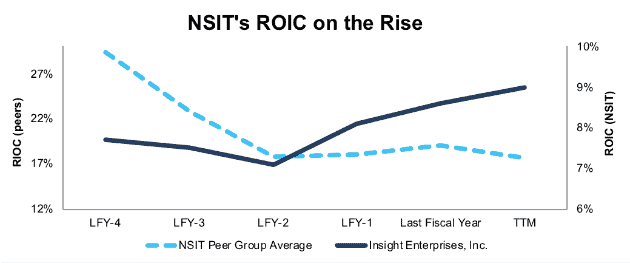

The improvement in ROIC appears to be specific to NSIT and not just the result of industry factors. Per Figure 2, NSIT’s ROIC has increased in each of the last three years, while its peers’ ROIC has fallen. Peers include (as noted in NSIT’s 2017 10-K filing) firms such as Amazon (AMZN), CDW Corporation (CDW), HP Inc. (HPQ), PCM Inc. (PCMI), and Systemax Inc. (SYX).

Figure 2: NSIT’s ROIC Rises While Peers’ Falls

Sources: New Constructs, LLC and company filings.

Growing High Margin Services Business Creates More Value (and Profits)

Buying IT hardware or software is as easy as walking into a store (or going to a website) and paying for the product. However, knowing which hardware works with particular software or which software will work best for your needs requires special expertise. NSIT leverages its unique expertise to provide a more hands-on approach to client service that creates value above and beyond traditional technology resellers.

This value-add creates barriers to entry and competitive advantages over the long-term. NSIT doesn’t depend solely on hardware/software sales, which are largely commoditized, but instead focuses on services and IT management. NSIT’s services business, which includes supply chain optimization, cloud data center transformation, digital innovation, and cloud, mobility, and big data consulting/management has grown from 6% of sales in 2014 to 10% TTM.

More importantly, the services business has much higher margins, and cannot be as easily replicated, due to the special expertise required and the quality of NSIT’s existing client relationships. In 2017, NSIT’s services business had gross margins of 59% (compared to 9% for products). In 2Q18, the services segment gross margin was 61%, compared to 8% for products. Such high margins mean services are key to NSIT’s future profit potential. In fact, in 2017 services derived 43% of gross profit, despite consisting of only 10% of sales. In 2Q18, services made up 51% of gross profit, but only 12% of total sales.

The quality of NSIT’s services business is recognized through industry accolades (shown below) and its roster of tech partners.

- In 2018, NSIT was recognized as Microsoft’s Artificial Intelligence Worldwide Partner of the Year

- In 2017, NSIT was named NetApp’s Flash Partner of the Year

- In 2017, NSIT was recognized as Microsoft’s Worldwide Mobile App Development Partner of the Year

- In 2017, NSIT was named the HPE North America Network Service Provider Partner of the Year

- In 2016, NSIT was recognized as Microsoft’s Worldwide Internet of Things Partner of the Year

Bear Case Ignores Growing IT Businesses

Insight Enterprises doesn’t need to develop the latest software or hardware. Rather, it benefits from its partner’s technological development efforts and focuses on procurement, delivery, installation, and service of these new products. Through this approach, Insight Enterprises benefits from many fast-growing technology markets, such as the Internet of Things, infrastructure-as-a-service (IaaS), and software-as-a-service (SaaS) without the costly research & development costs commonly associated with these industries.

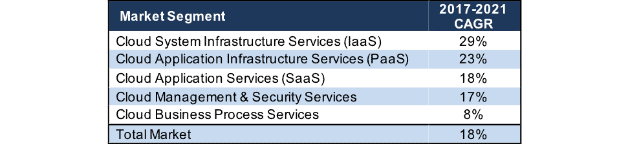

According to Gartner, the entire public cloud market (which includes IaaS and SaaS), is expected to grow 18% compounded annually from 2017-2021. Splitting into individual segments of the market, IaaS is expected to grow 29% compounded annually and SaaS 18% compounded annually. More details in Figure 3.

Figure 3: Worldwide Public Cloud Service Revenue Growth Forecast

Sources: Gartner and New Constructs, LLC

Additionally, McKinsey predicts the Internet of Things market will be worth $581 billion for Information and Communications technology spend and will grow anywhere from 7-15% compounded annually from 2015-2020. NSIT is focused on expanding further into both of these markets. As management notes in its 2017 10-K, “We have invested in, and will continue to invest in, technical tools and resources to provide clients with the services required to simplify the cloud adoption.”

Bears Ignore the Strong Economic Moat

As a reseller, bears will try and lump NSIT into a board category of technology retailer (or reseller). This categorization would imply that NSIT (and other retailers) stand no chance against “retail-killer” Amazon. Despite evidence to the contrary, this categorization is limited and ignores the advantage that Insight Enterprises’ business model has over a traditional hardware/software retailer.

Because NSIT combines product sales from a number of different IT vendors with consulting and management services, its business creates more value, for all involved stakeholders, the larger its user base grows. Its partners (which totaled 5,400 in 2017 and included firms such as Cisco (CSCO), Microsoft (MSFT), IBM (IBM), HP Inc. and more) don’t want to invest significant time and resources in setting up resale distribution or direct-ship programs with smaller businesses.

On the other hand, small and medium-sized business lack the time or expertise to go directly to each separate vendor to build a comprehensive IT solution. NSIT gives these businesses a one-stop shop to fulfill all their IT needs from the world’s leading hardware and software companies, and it shows them how to implement and use the technology or manages it for them.

NSIT’s economic moat also grows with each new user, as its client list becomes harder to replicate. Lastly, the business becomes more valuable to new and existing clients with each additional customer as the company can command greater pricing power with its partners.

Partners recognize the value of a reseller such as NSIT (which can help lower sales costs by handling customer interaction/sales talk for the partner), and provide incentives based upon volume of sales of their products. Additionally, manufacturers provide mailings lists, contacts, or leads to NSIT to further grow both the partner and NSIT’s businesses. As NSIT explains, “these incentives allow it to increase its marketing reach and strengthen relationships with leading manufacturers.”

Given the strength and breadth of its relationships on both the supplier and customer side, it’s hard to imagine another company supplanting NSIT in the foreseeable future. Amazon seems like the only company that could plausibly try, but it’s hard to imagine that other tech giants would cooperate with an effort by their rival to insert itself more directly into their value-chain.

Improving ROIC Correlated with Creating Shareholder Value

Numerous case studies show that getting ROIC right is an important part of making smart investments. Ernst & Young recently published a white paper that proves the material superiority of our forensic accounting research and measure of ROIC. The technology that enables this research is featured by Harvard Business School.

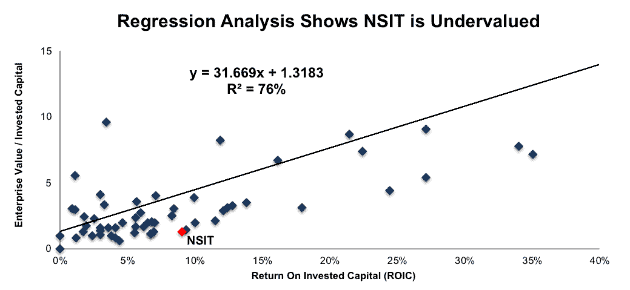

Per Figure 4, ROIC explains 76% of the difference in valuation for the 83 IT services & consulting firms under coverage. NSIT’s stock trades at a significant discount to peers as shown by its position below the trend line in Figure 4. NSIT’s enterprise value per invested capital (a cleaner version of price to book) of 1.3 implies that the market expects its ROIC to decline to below 1%.

Figure 4: ROIC Explains 76% Of Valuation for IT Services & Consulting Firms

Sources: New Constructs, LLC and company filings

If the stock were to trade at parity with its peer group, it would be worth $133/share – an impressive 246% upside to the current stock price. Given the firm’s improving margins, quality capital allocation, and value-add business model, one would think the stock would garner a premium valuation. Below we’ll use our DCF model to quantify just how high shares could rise assuming conservative profit growth.

NSIT Is Priced for Minimal Profit Growth

Despite the strong fundamentals, scalability of its business, and macro tailwinds, NSIT is cheap, whether analyzed through traditional valuation metrics or the expectations baked into the stock price. At its current price of $54/share, NSIT has a P/E ratio of 16.4, which is well below the Technology sector average of 35.4 and the S&P 500 average of 24.7.

When we analyze the cash flow expectations baked into the stock price, we get similar findings. At its current price of $54/share, NSIT has a price-to-economic book value (PEBV) ratio of 1.1. This ratio means the market expects NSIT’s NOPAT to grow no more than 10% from current levels.

This expectation seems rather pessimistic given that NSIT has grown NOPAT by 4% compounded annually over the past decade and 11% compounded annually since 1998.

Such pessimistic expectations create large upside potential. If we assume that NSIT’s can maintain TTM NOPAT margins (2%) and grow NOPAT by 6.5% compounded annually over the next decade, the stock is worth $68/share today – a 26% upside. See the math behind this dynamic DCF scenario.

Tax Reform Wil Help Boost Margins

NSIT stands to continue to benefit from tax reform as it paid a cash tax rate of 35% in 2017, which is higher than the median S&P 500 company at 28%. If NSIT can reduce its cash tax rate to the new statutory rate of 21%, it can generate 22% more NOPAT and increase its NOPAT margin from 1.9% to 2.4%.

Earnings Beat Has Proven Fruitful in the Past

The growth in IoT and cloud markets provides NSIT an excellent runway for future profit growth. In the shorter-term, volatility around earnings could present a catalyst to send NSIT higher. Consensus 2018 EPS expectations have risen throughout the year and management expects adjusted EPS to rise anywhere from 39 to 42% year-over-year in 2018.

Despite rising expectations, NSIT has beat EPS expectations for eight consecutive quarters. Another beat could have a dramatic impact on the stock, as we’ve seen in the past.

- Stock jumped 9% in the two days following 2Q18 earnings

- Stock jumped 21% in the 2 days following 1Q18 earnings

- Stock jumped 9% in the day after 2Q17 earnings

The announcement of further acquisitions could also drive the stock higher since management has already demonstrated its ability to create value through acquisitions. After NSIT announced the $258 million acquisition of Datalink in November 2016, the stock rose 24% over the following month. In August 2018, NSIT announced the $79 million acquisition of Cardinal Solutions and the stock rose 9% over the next two days.

In the meantime, investors receive a decent yield via share repurchases, as we’ll show below.

Share Repurchases Could Offer 1.5% Yield

Insight Enterprises does not pay a dividend, but instead returns capital to shareholders through share repurchases. In February 2018, the Board of Directors authorized a repurchase of up to $50 million. Through the first six months of 2018, NSIT repurchased $22.1 million and has $27.9 million remaining under its current authorization. In 2017, no repurchase program was authorized. However, in 2016 and 2015, NSIT repurchased $50 million and $92 million respectively. Were the company to repurchase the remainder of its authorization, it would repurchase $27.9 million and return 1.5% of the current market cap to shareholders.

Insider Trading and Short Interest Are Minimal

Insider activity has been minimal over the past 12 months, with no shares purchased and 152 thousand shares sold for a net effect of 152 thousand shares sold. These sales represent less than 1% of shares outstanding.

There are currently 418 thousand shares sold short, which equates to 1% of shares outstanding and 2.4 days to cover. Short interest has fallen 16% from the prior month and is down 15% from its 52-week high. Continued improvement in Insight Enterprises’ fundamentals could bring about a minor short squeeze and send shares higher.

Critical Details Found in Financial Filings by Our Robo-Analyst Technology

As investors focus more on fundamental research, research automation technology is needed to analyze all the critical financial details in financial filings. Below are specifics on the adjustments we make based on Robo-Analyst[2] findings in Insight Enterprises 2017 10-K:

Income Statement: we made $48 million of adjustments, with a net effect of removing $40 million in non-operating expense (1% of revenue). We removed $4 million in non-operating income and $44 million in non-operating expenses. You can see all the adjustments made to NSIT’s income statement here.

Balance Sheet: we made $745 million of adjustments to calculate invested capital with a net increase of $333 million. The most notable adjustment was $429 million in asset write-downs. This adjustment represented 36% of reported net assets. You can see all the adjustments made to NSIT’s balance sheet here.

Valuation: we made $227 million of adjustments with a net effect of decreasing shareholder value by $227 million. There were no adjustments that increased shareholder value. The largest adjustment to shareholder value was $227 million in total debt, which includes $65 million in operating leases. This lease adjustment represents 3% of NSIT’s market cap.

Attractive Funds That Hold NSIT

The following funds receive our Attractive-or-better rating and allocate significantly to Insight Enterprises.

- ICON Information Technology Fund (ICTEX) – 2.6% allocation and Attractive rating.

- Royce Small-Cap Value Fund (RVVHX) – 2.5% allocation and Very Attractive rating.

- First Trust Value Line 100 Exchange Traded Fund (FVL) – 1.4% allocation and Attractive rating.

This article originally published on August 23, 2018.

Disclosure: David Trainer, Kyle Guske II, and Sam McBride receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] Ernst & Young’s recent white paper “Getting ROIC Right” proves the superiority of our holdings research and analytics.

[2] Harvard Business School features the powerful impact of our research automation technology in the case New Constructs: Disrupting Fundamental Analysis with Robo-Analysts.