We closed this position on March 31, 2020. A copy of the associated Position Update report is here.

Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life.

When boards of directors allow managers to measure performance with the wrong metrics, they can ruin businesses and shareholder value. Meanwhile, managers tout record (non-GAAP) performance and earn significant bonuses. Without performing real diligence, unknowing investors are none the wiser.

When we strip out the noise, we find that this firm’s reported, non-GAAP results are not what they seem. Add in increased competition from more nimble start-ups, the risk of future write-downs, and management’s decision to ignore prudent stewardship of capital, and investors should be on alert. Mondelez International (MDLZ: $50/share) is in the Danger Zone.

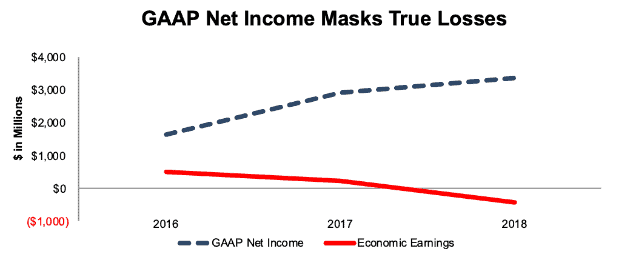

Don’t Believe Reported Results – True Cash Flows Are Declining

We first put MDLZ in the Danger Zone in March 2016. In our original report, we noted that profits were declining, and would continue to do so. Investors who only look at GAAP net income may think we were wrong. But, when we remove accounting distortions and calculate MDLZ’s economic earnings, which represent the true cash flows of the business, we find that MDLZ’s profitability declined.

From 2016 to 2018 MDLZ’s GAAP net income grew 43% compounded annually. Economic earnings fell from $508 million to -$413 million over the same time, per Figure 1.

Figure 1: MDLZ’s GAAP Net Income Rises as Economic Earnings Fall

Sources: New Constructs, LLC and company filings

The disconnect between GAAP net income and economic earnings in 2018 is primarily attributed to a $778 million (23% of GAAP net income) gain on equity method investment transactions. Only by removing this non-recurring income can we evaluate the true recurring profits of MDLZ’s operations.

We also made the following adjustments to the balance sheet:

- $3.9 billion (8% of reported net assets) in asset write-downs

- $666 million (1% of reported net assets) in off-balance sheet operating leases

By adding these items back to invested capital, we hold MDLZ accountable for all capital invested into the business, which management doesn’t want to do, as we’ll touch on below. These adjustments, combined with a rising weighted average cost of capital (WACC), which was at 6.0% in 2018, up from 5.5% in 2017), increase the capital charge and decrease MDLZ’s economic earnings.

Poor Capital Stewardship Hurts Investors

The deterioration of MDLZ’s fundamentals can be tied to the company’s poor corporate governance. Failure to incentivize executives with goals that align with creating shareholder value can be a serious detriment to investors.

In the past, Mondelez’s executive compensation, which includes annual bonuses and performance shares, has been tied to organic revenue growth, EPS, total shareholder return and adjusted return on invested capital (ROIC) goals. Normally, the inclusion of ROIC would be a positive, after all, improving ROIC is directly correlated with increasing shareholder value.

However, investors need to verify the integrity of any ROIC or performance measurement calculation. We’ve seen too many firms tout the use of “ROIC” while the ROIC calculation is compromised. Unfortunately, we find Mondelez’s ROIC calculation to be lacking. For example, MDLZ removed numerous expenses from its NOPAT, such as the costs of its multi-year restructuring efforts. In addition, MDLZ ignored off-balance sheet debt in the form of operating leases in its invested capital calculation. The low-quality of its ROIC calculation allows MDLZ to report a rising ROIC from 7.5% to 10% over the past three years.

Frankly, we don’t think corporate managers should be in the business of measuring their own performance any more than money managers. Independent, third-party analysis of performance should be standard for corporations just as the use of fund administrators to measure performance and report to investors is standard in the hedge fund business.

Our calculation[1], which accounts for all recurring profits and capital invested into the business, shows MDLZ’s ROIC has actually declined from 6% to 5% over the same period.

Going forward, MDLZ plans to replace adjusted ROIC with adjusted EPS in its long-term incentive program. In announcing this change, management noted “the large amount of goodwill on the balance sheet restricts their ability to further impact ROIC.” This move suggests that management wants to divert attention away from the goodwill on its poorly-managed balance sheet. Though Mondelez’s ROIC is not perfect, it is still much better than adjusted EPS, which provide little-to-no accountability for capital stewardship, or balance sheet management.

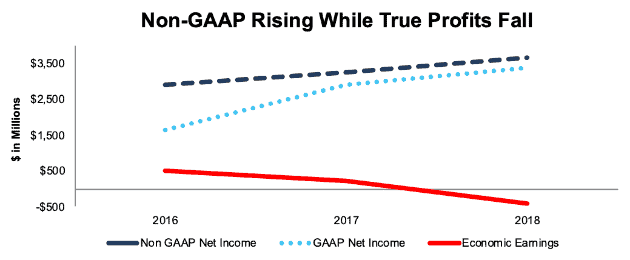

Non-GAAP Metrics Further Mislead Investors

While its true profits decline, MDLZ has investors focus on non-GAAP metrics. These metrics, such as adjusted gross profit, adjusted operating income, and adjusted EPS paint a wildly different picture of the firm’s profits. Some of the expenses MDLZ excludes from its non-GAAP metrics include:

- Simplify to Grow Program (restructuring program) costs

- Acquisition related costs

- Malware incident expenses

- Loss on debt extinguishment

After all adjustments, MDLZ reported non-GAAP net income of $3.7 billion in 2018 compared to $3.4 billion in GAAP net income and -$413 million in economic earnings.

Figure 2: MDLZ’s Non-GAAP Metrics Are Made To Look Good

Sources: New Constructs, LLC and company filings

MDLZ’s Profitability Lags in a Cutthroat Business

As Mondelez has grown, acquired stakes in other brands, and entered/exited new businesses, the company’s operations have become less efficient. Since 2016, MDLZ’s NOPAT margins have fallen from 15% to 14% in 2018. Over the same time, the market cap weighted average of the company’s listed competitors, which includes companies such as Campbell Soup Company (CPB), General Mills (GIS), Kellogg Company (K), PepsiCo Inc. (PEP) and The Hershey Company (HSY), has improved from 16% to 18%.

Figure 3: MDLZ’s NOPAT Margin Vs. Peers

Sources: New Constructs, LLC and company filings

Poor capital allocation has led to MDLZ’s average invested capital turns, a measure of balance sheet efficiency, remaining stagnant at 0.4 for each of the past three years, which is down from 0.7 back in 2008/2009. The combination of margin contraction and stagnant capital turns has led to MDLZ’s already low ROIC falling even further behind competitors. Per Figure 4, the gap between peers’ ROIC and MDLZ’s ROIC is now 30 basis points worse than it was in 2016.

Figure 4: MDLZ’s ROIC Vs. Peers

Sources: New Constructs, LLC and company filings

Additionally, when comparing MDLZ to its competitors, only two firms earn a lower ROIC. The two firms are notable. One is Campbell Soup (CPB), which is in the process of divesting international assets under pressure from activists. The other is Kraft Heinz (KHC), which recently fell almost 30% after announcing a $15 billion write-down of its brand names.

The news of MDLZ’s possible acquisition of Campbell Soup Company's international business does not inspire much confidence, given CPB’s lackluster ROIC of 5%. Could MDLZ, with its misleading accounting metrics, low ROIC, and high goodwill be the next large packaged food firm to fall?

Is Mondelez The Next Kraft Heinz?

When Kraft Heinz announced a $15.4 billion write-down on the value of its Kraft and Oscar Mayer brands, it put the rest of the consumer packaged goods industry on alert. What were once considered strong brands were having trouble adapting in an industry facing significant competition from upstart food/snack firms and changing consumer preferences. After the write-down, analysts noted that shrinking revenue, modest earnings growth, and a ballooning balance sheet could cause issues. Sound familiar?

MDLZ’s revenue has stagnated in recent years, its economic earnings have fallen, and its total debt, which includes off-balance sheet operating leases, has grown from $16.8 billion in 2015, to $19.3 billion currently. The company also holds significant goodwill on its balance sheet, to the tune of $20.7 billion (31% of invested capital) in 2018. For comparison, KHC’s goodwill equaled 38% of its invested capital prior to the recent write-down.

We’ve shown before that companies with significant goodwill on the books are more likely to take significant write-downs. Additionally, this goodwill artificially inflates accounting book value and lowers price-to-book ratios while economic book value ratios rise.

For years, markets gave KHC and its overblown goodwill and balance sheet a pass. It’s hard to predict when managers will finally take long overdue write-downs, but we’ve seen how much damage these write-downs can do to stock prices, e.g. KHC. We recommend investors avoid stocks like MDLZ where risk of significant write-downs is high.

Bulls Ignore Changing Consumer Preferences and Online Shift

Despite the warning signs above, bulls will argue that packaged food stocks still represent safe investments. After all, people always need food, and these companies have historically performed well in bear markets. However, this argument ignores key shifts in the packaged foods industry that impacts snack giants such as Mondelez.

Consumers are losing interest in traditional packaged snack foods. According to Mintel, a market research provider, freshness of food has become the top purchase driver for millennials and Gen Z consumers, at the expense of conventional snacking products. Additionally, Euromonitor finds that impulse snack purchases are on the decline due to a growing preference for fresh and prepared foods that are more widely available now.

Consumers used to focus their shopping on the interior aisles of grocery stores containing packaged snacks and foods sold by MDLZ and other snack giants. Now, they’re looking for fresher foods often found in the exterior aisles.

To make matters worse, when consumers do buy packaged snack foods, they’re increasingly doing so online. In the past, shelf-space and distribution networks gave large food companies, like Mondelez, a competitive advantage over smaller firms. With the rise in online sales, grocery delivery, and pickup orders, physical shelf space is becoming less important and lowering barriers to entry. When commenting on the success of smaller, more niche products, Peter Ter Kulve, Unilever’s “chief transformation officer” noted, “basically there are no entry barriers.”

An example of this industry change can be seen through Amazon’s “infinite shelf”, where 70% of the top-selling foods are start-ups that tend to be organic focused. Although online grocer’s like Amazon only make up around 6% of all industry sales, the e-retail segment of the market had 18% year-over-year revenue growth going into 2018. This rise of e-commerce, which makes it easy to compare prices between brands and retailers, is pressuring margins across the consumer packaged goods industry. Analysts at Bernstein say Mondelez is one of the most unprepared to compete with Amazon as it expands into grocery/food markets.

Bull Case is Entirely Priced In

We believe the 24% increase in MDLZ’s stock price (S&P up 15%) since the beginning of the year has been driven by investors willing to trust misleading non-GAAP and reported earnings. According to flawed traditional valuation metrics, MDLZ doesn’t appear overvalued. Its P/E ratio of 22 sits in line with the overall market. However, when we analyze the cash flow expectations baked into the stock price, we find that shares are significantly overvalued.

To justify its current price of $50/share, MDLZ must maintain 2018 NOPAT margins of 14% (after three consecutive years of decline) and grow NOPAT by 5% compounded annually for the next 13 years. See the math behind this dynamic DCF scenario.

For reference, according to Statista, the chocolate confectionery market is expected to grow by 3%, 1% and 5% compounded annually from 2019-2023 in America, Europe and Asia respectively. Additionally, the cookie & cracker market is expected to grow 2%, 2%, and 6% compounded annually over the same time in those regions. In other words, to justify its current price, MDLZ must grow faster than projected growth rates in nearly all its geographic areas and business segments.

Even if Mondelez can maintain current margins and grow NOPAT by 3% compounded annually (still faster than most of its markets/segments) for the next decade, the stock is worth only $35/share today – a 30% downside. See the math behind this dynamic DCF scenario.

Each of these scenarios also assumes MDLZ is able to grow revenue, NOPAT and FCF without increasing working capital or fixed assets. This assumption is unlikely but allows us to create best-case scenarios that demonstrate how high expectations embedded in the current valuation are. For reference, MDLZ’s invested capital has grown on average $379 million (1% of 2018 revenue) over the past five years.

Acquisition Is Unlikely Given MDLZ Size and Overvalued Stock

Often the largest risk to any bear thesis is what we call “stupid money risk”, which means an acquirer comes in and pays for MDLZ at the current, or higher, share price despite the stock being overvalued. Given MDLZ’s size ($71 billion market cap) and its ownership of many different brands ranging from cookies to chocolate, it would seem more likely that the company spins off some of these assets, rather than get acquired. KHC, which was once interested in acquiring larger consumer packaged goods firms, would seem unlikely to approach any deal with MDLZ given the recently recognized failure of its past acquisition strategy.

However, we think it helps to quantify what, if any, acquisition hopes are priced into the stock.

Walking Through the Acquisition Math

First, investors need to know that Mondelez has large (hidden) liabilities that make it more expensive than the accounting numbers would initially suggest.

- $3.3 billion in net deferred tax liabilities (5% of market cap)

- $1.6 billion in underfunded pensions (2% of market cap)

- $666 million in operating leases (1% of market cap)

- $581 million in outstanding employee stock options (1% of market cap)

After adjusting for these liabilities, we can model multiple purchase price scenarios.

Even in the most optimistic of scenarios, MDLZ is worth no more than its current share price. For this analysis, let’s assume PepsiCo (PEP), with its existing footprint in packaged foods, wishes to acquire MDLZ. Given PEP’s focus on ROIC, it’s unlikely it would be willing to overpay and lower the return it earns on any potential deal.

Figures 5 and 6 show what we think PEP should pay for MDLZ to ensure it does not destroy shareholder value. While hypothetical, acquiring MDLZ would strengthen PEP’s position in the consumer packaged goods market and expand its offerings. However, there are limits on how much PEP would pay for MDLZ to earn a proper return, given the NOPAT or free cash flows being acquired.

Each implied price is based on a ‘goal ROIC’ assuming different levels of revenue growth. In both scenarios, the estimated revenue growth rate is 0.4% in year one and 2.7% in year two, which are the consensus estimates for MDLZ’s revenue growth. For the subsequent years, we use 2.7% in scenario one because it represents a continuation of consensus estimates. We use 6% in scenario two because it assumes a merger with PEP could create additional revenue opportunities through new co-branded products.

We conservatively assume that PEP can grow MDLZ’s revenue and NOPAT without spending anything on working capital or fixed assets beyond the original purchase price. We also assume MDLZ immediately achieves a 15% NOPAT margin, which is the highest in company history. For reference, MDLZ’s 2018 NOPAT margin is 14%, so this assumption implies immediate improvement and allows the creation of truly best-case scenarios.

Figure 5: Implied Acquisition Prices for PEP to Achieve 5% ROIC

Sources: New Constructs, LLC and company filings

Figure 5 shows the ‘goal ROIC’ for PEP as its WACC or 5%. Even if MDLZ can grow revenue by 4% compounded annually, with a 15% NOPAT margin for the next five years, the firm is worth less than its current price of $50/share. It’s worth noting that any deal that only achieves a 5% ROIC would only be value neutral and not accretive, as the return on the deal would equal PEP’s WACC.

Figure 6: Implied Acquisition Prices for PEP to Achieve 11% ROIC

Sources: New Constructs, LLC and company filings

Figure 6 shows the next ‘goal ROIC’ of 11%, which is PEP’s current ROIC. Acquisitions completed at these prices would be truly accretive to PEP shareholders. Even in the best-case growth scenario, the implied stock value is less than the current price. Any scenario assuming less than 4% compound annual growth in revenue would result in further capital destruction for PEP.

Catalysts Could Sink Shares

Missed Earnings: MDLZ has met or beaten EPS expectations in 11 of the past 12 quarters. The ability to meet quarterly expectations while economic earnings decline precipitously further illustrates the misleading nature of accounting earnings. Now, as uncertainty continues to rise in the consumer packaged goods industry, investors may grow more discerning. After years of restructuring has left MDLZ no better off, even the slightest miss on earnings could push investors to sell as they’re forced to face the continued destruction of shareholder value that is masked by accounting earnings.

Global Slowdown: It’s widely believed that global growth will slow in the coming years. The Organization for Economic Cooperation and Development (OECD) recently issued downward revisions to economic growth for nearly all G20 countries. The International Monetary Fund (IMF) has noted that “global financial conditions have started to tighten” and issued downward revisions to many major economies. A global slowdown, coming when growth in MDLZ’s end markets is already minimal, could put increasing pressure on margins and make it even harder for MDLZ to justify the expectations baked into its stock price.

Possible Write-Downs: While no certainty, it’s possible MDLZ could write-down some of the goodwill on its balance sheet, as did KHC. Such a write-down (even if not as large) would send further signals that the consumer packaged goods industry faces significant challenges moving forward and force investors to re-evaluate the premium valuation it has given to what was once considered a group of “safe” stocks.

Insider Sales and Short Interest are Minimal

Over the past 12 months, 309 thousand insider shares have been purchased and 371 thousand have been sold for a net effect of 62 thousand insider shares sold. These sales make up <1% of shares outstanding.

Short interest is currently 10.8 million shares, which equates to 1% of shares outstanding and just over 1 day to cover. Short interest is down 12% from the prior month despite the firm’s fundamentals deteriorating and the stock getting more overvalued.

Critical Details Found in Financial Filings by Our Robo-Analyst Technology

As investors focus more on fundamental research, research automation technology is needed to analyze all the critical financial details in financial filings. Below are specifics on the adjustments we make based on Robo-Analyst findings in Mondelez’s 2018 10-K:

Income Statement: we made $2.6 billion of adjustments with a net effect of removing $219 million in non-operating expense (1% of revenue). We removed $1.4 billion related to non-operating expenses and $1.2 billion related to non-operating income. You can see all the adjustments made to MDLZ’s income statement here.

Balance Sheet: we made $21.6 billion of adjustments to calculate invested capital with a net increase of $20.6 billion. The most notable adjustment was $10.6 billion (23% of net assets) in other comprehensive income. You can see all the adjustments made to MDLZ’s balance sheet here.

Valuation: we made $24.8 billion of adjustments with a net effect of decreasing shareholder value by $24.8 billion. There were no adjustments that increased shareholder value. Apart from $19.3 billion in total debt, the largest adjustment was $3.3 billion in deferred tax liabilities. This tax adjustment represents 5% of MDLZ’s market value. See all adjustments to MDLZ’s valuation here.

Unattractive Funds That Hold MDLZ

The following funds receive our Unattractive rating and allocate significantly to Mondelez International.

- Invesco Dynamic Food & Beverage ETF (PBJ) – 5.5% allocation and Unattractive rating

- ICON Consumer Staples Fund (ICRAX) – 4.6% allocation and Unattractive rating

- Gabelli Focus Five Fund (GWSAX) – 4.0% allocation and Very Unattractive rating

This article originally published on April 8, 2019.

Disclosure: David Trainer, Andrew Gallagher, Kyle Guske II, and Sam McBride receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] Ernst & Young’s recent white paper “Getting ROIC Right” demonstrates the superiority of our stock research and analytics.